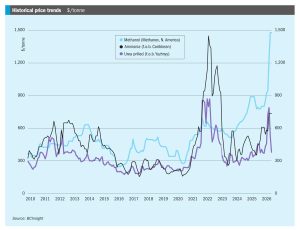

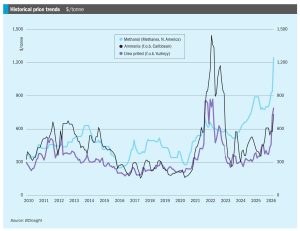

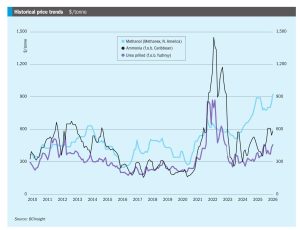

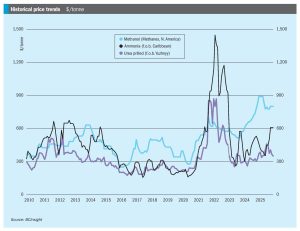

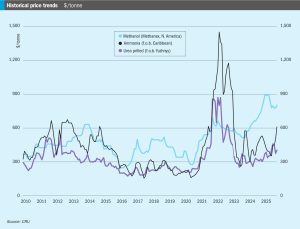

Price Trends

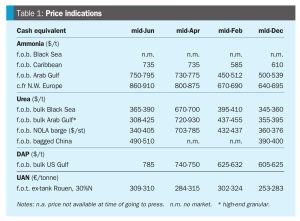

Ammonia values have continued to ease across most regions at the end of June, as the first ammonia vessels begin to exit the Gulf since the Iranian conflict began. Iranian ammonia had also begun to flow to India following the US Treasury’s issuance of a 60-day sanctions waiver on 22 June, allowing dollar-denominated trade in Iranian petrochemical products through 21 August. As a result, Indian bids have been heard as low as $750/t c.fr, as buyers benefit from a widening pool of available supply - Iranian, Chinese and renewed Southeast Asian material are all competing for the same business.