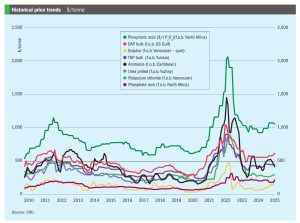

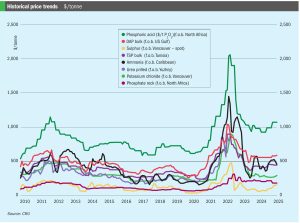

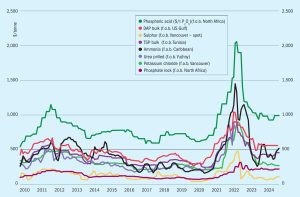

Market Insight

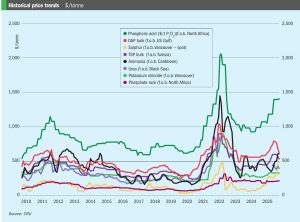

Price trends and market outlook, 18th December 2025.

Price trends and market outlook, 18th December 2025.

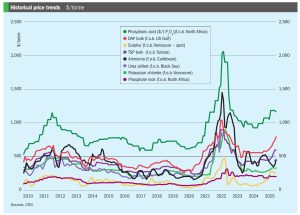

Price trends and market outlook, 23rd October 2025

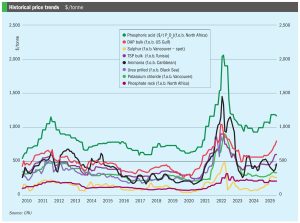

Price trends and market outlook, 21st August 2025

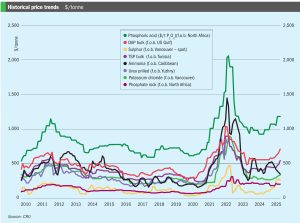

Price trends and the market outlook, 19th June 2025

Price trends and the market outlook, 10th April 2025

Price trends and market outlook, 20th February 2025

Market snapshot, 2nd January 2025

Market snapshot, 17th October 2024 Urea : Prices firmed in a thin market in mid-October. Middle East values shot up $20/t on expectations that Indian Potash Limited (IPL) would announce another tender to secure tonnes for India in December. If correct, this will follow hot on the heels of the latest Rashtriya Chemicals and Fertilizers (RCF) purchase tender for 0.56 million tonnes of urea. Sohar International Urea & Chemical Industries (SIUCI) sold a November cargo at $390/t f.o.b. with further trader interest reported at $385/t f.o.b. This demand was probably generated by traders positioning themselves for IPL’s expected tender, given that other markets generally remained quiet.

Market snapshot, 15th August 2024 Urea: A stand-off between buyers and sellers has left prices fairly flat in recent weeks with little liquidity. India's latest import tender was, however, finally confirmed for 29th August closing. The tender’s long shipment window allows NFL to secure tonnages through to end-October and took the market by surprise. This is a bearish signal that should increase dramatically the volume offered to NFL. The tender could exclude volumes from China with supply instead focused on the Middle East and Russia.

Market as of 20th June 2024. Urea: Prices remain stable while the market awaits clear price direction on whether to hold current f.o.b. levels or to push higher.