Price Trends

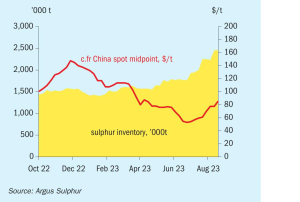

Maria Mosquera, Editor of the Argus Sulphur Report and Liliana Minton, Editor of the Argus Sulphuric Acid Report at Argus Media assess price trends and the market outlook for sulphur and sulphuric acid.

Maria Mosquera, Editor of the Argus Sulphur Report and Liliana Minton, Editor of the Argus Sulphuric Acid Report at Argus Media assess price trends and the market outlook for sulphur and sulphuric acid.

Lithium ion battery production is driving major expansions in nickel and cobalt extraction, but lithium iron phosphate (LFP) battery use is growing rapidly.

While phosphate fertilizer production represents the main slice of demand for elemental sulphur and sulphuric acid, sulphur fertilizers continue to be a growing sector of demand due to changes in the way that we use sulphur.

CRU’s Sulphur + Sulphuric Acid 2023 Conference and Exhibition takes place at the Sheraton New Orleans, Louisiana, USA, 6-8 November.

This year’s Argus Fertilizer Europe Conference is taking place at the EPIC SANA Lisboa Hotel, Lisbon, Portugal, 17-19 October 2023.

Some 1,400 delegates from 533 companies and 83 countries gathered in Prague, Czech Republic, for the 90th International Fertilizer Association (IFA) Annual Conference, 22 May – 24 June 2023. We report on the main highlights of this three-day flagship event.

Market Insight courtesy of Argus Media. Urea: While prices mostly fell in mid-August, the main development was the massive purchase of Chinese urea by Indian Potash Limited. IPL confirmed that, out of a total tender settlement of 1.759 million tonnes, one million tonnes will be met by Chinese exporters. This far exceeded expectations and added to the already bearish sentiment of most market players.

We profile leading European NPK fertilizer producers. Major ownership changes have taken place within the EU during the last three years. Europe’s NPK producers have also needed to adjust their raw material sourcing in response to the Russia-Ukraine conflict.

Crop residues are the plant materials that are left in the field after the harvested portion is removed. Many growers are increasingly valuing these materials due to their nutrient content and soil health benefits. Dr Karl Wyant, Nutrien’s Director of Agronomy, highlights the value of crop residues and discusses how to manage these more effectively without interfering with on-farm activities. Ag retailers, in particular, are well-placed to advise growers on how to unlock value from their residues.

Many crops are sensitive to chloride due to a genetic susceptibility. Similarly, crops can become stressed when soil salinity reaches high levels, a situation that typically occurs in water scarce regions. So, when is low-chloride crop nutrition needed? Dr Heike Thiel of K+S Minerals and Agriculture GmbH provides some answers.