Fertilizer International 532 May-Jun 2026

27 May 2026

Water-soluble fertilizer growth dash

MARKET REPORT

Water-soluble fertilizer growth dash

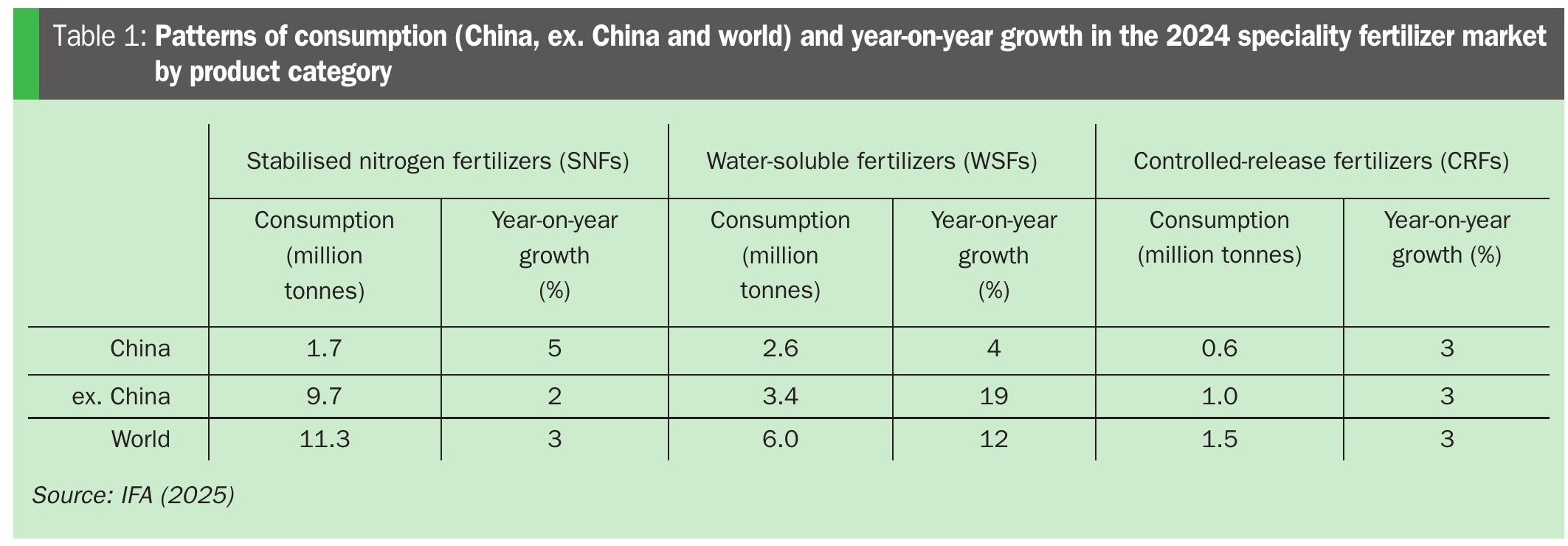

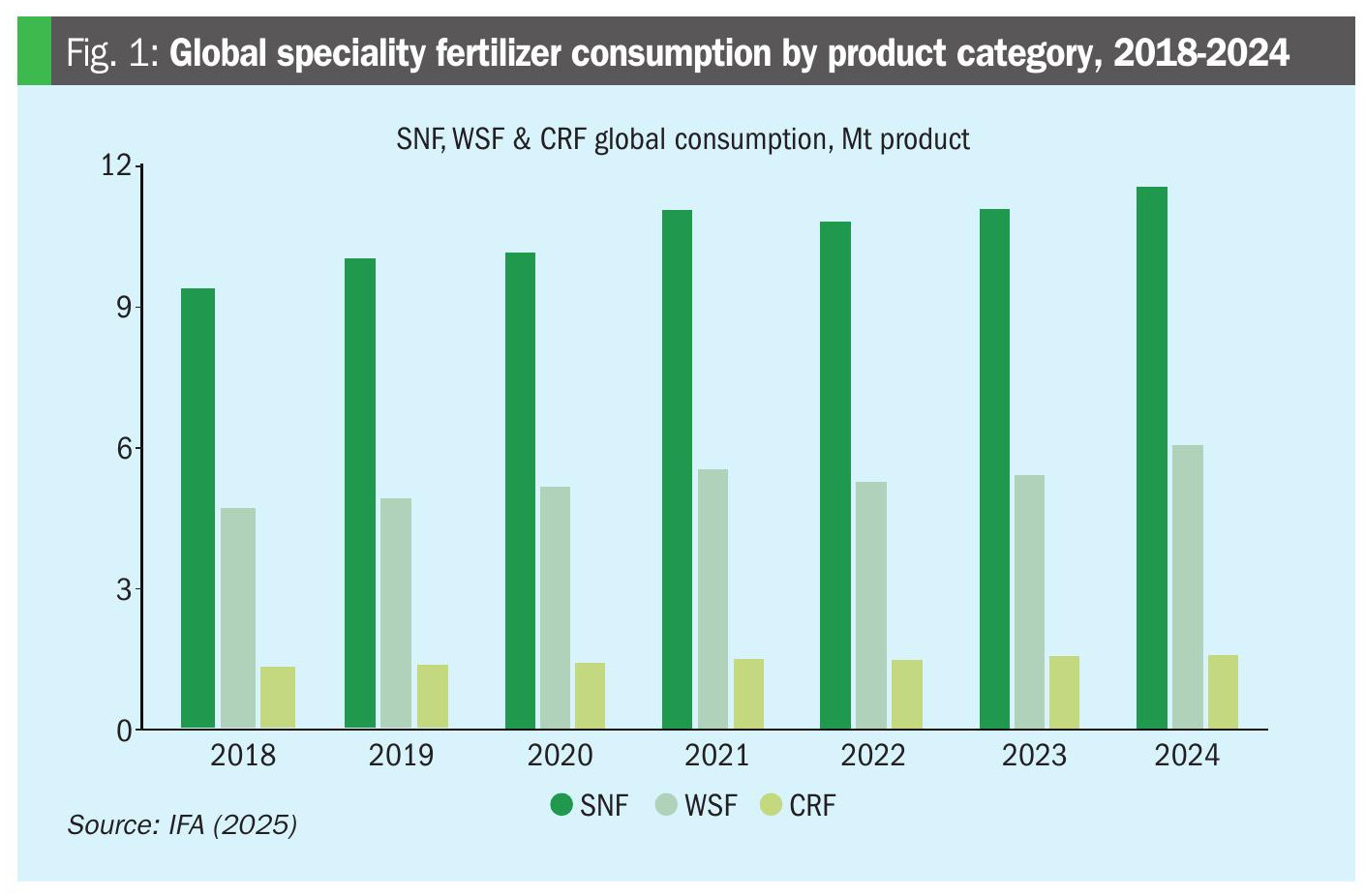

The International Fertilizer Association (IFA) has released its latest annual assessment of global specialty fertilizer demand for the year 2024. The assessment covers three product categories: stabilised nitrogen fertilizers (SNFs), water-soluble fertilizers (WSFs) and controlled-release fertilizers (CRFs). Total specialty fertilizer consumption across the three categories was close to 19 million tonnes in 2024, with WSFs emerging as the standout growth performer.

The global specialty fertilizer market grew by 5% year-on-year (y-o-y) to reach 18.8 million tonnes in 2024, according to the latest assessment by the International Fertilizer Association (IFA)1. This growth builds on a rebound in recovery in 2023 and follows the market disruptions of 2022. Previous IFA assessments have estimated that between 2016 and 2021 the specialty fertilizer market grew by around 45% from 10.9 million tonnes to 16.9 million tonnes2 (Fertilizer International 519, p12) before contracting by 7% in 2022 to 15.8 million tonnes3.

Specialty market growth in 2024 varied by product segment. The water-soluble fertilizer (WSF) category was the standout performer, surging ahead by 12% y-o-y. The controlled-release fertilizer (CRF) and stabilised nitrogen fertilizer (SNF) segments, meanwhile, were both characterised by more modest growth rates of 3% y-o-y.

IFA identified the following as the key growth drivers in the specialty fertilizer market during 2024:

• Favourable affordability – with a stable price environment supporting global demand.

• Good overall availability – this was maintained by a combination of firm global production and the drawdown of stocks accumulated in 2023, outweighing Chinese export restrictions on certain products.

• Growth in micro-irrigation – this helped to underpin production of high-value crops, a key market for specialty products.

• More efficient fertilizer use – this is being promoted by government policies/support in some regions and reflects the general global trend towards greater nutrient use efficiency (NUE).

Notably, the overall growth in global demand for specialty products in 2024 was led by markets outside of China, in comparison to more muted Chinese domestic demand growth.

“In 2024, all specialty product categories continued their upward growth, with water-soluble fertilizers emerging as a particularly strong performer, achieving an estimated 12% year-on-year growth,” Rajiv Ram, IFA’s Fertilizer Demand Analyst and the author of the assessment, told New AG International.

Specialty market overview

Specialty fertilizer consumption outside of China grew by 6% y-o-y in 2024 to reach 14.1 million tonnes, double the 3% growth rate of the previous year. A more detailed breakdown of consumption (world, ex. China and China) by product category is shown in Table 1 and Figures 1 and 2.

Stabilised nitrogen fertilizers (SNFs) are the highest volume, moderate growth segment:

• Global consumption increased 3% y-o-y in 2024 to 11.3 million tonnes, following 4% y-o-y growth in 2023.

• Consumption ex. China rose by 2% y-o-y in 2024 to reach 9.7 million tonnes, after 4% y-o-y growth in 2023.

• China’s consumption grew more strongly, by 5% y-o-y, to 1.7 million tonnes.

Water-soluble fertilizers (WSFs) are the lower volume, highest growth segment:

• Global consumption grew strongly by 12% y-o-y in 2024 to 6.0 million tonnes, after a 3% y-o-y rise in 2023.

• Consumption ex. China rebounded by 19% y-o-y to 3.4 million tonnes in 2024, after flat growth in 2023 and a 13% y-o-y drop in consumption in 2022.

• China’s consumption, meanwhile, grew by 4% y-o-y in 2024 to 2.6 million tonnes.

Controlled-release fertilizers (CRFs) are the lowest volume, moderate growth segment:

• Global consumption increased by 3% y-o-y to 1.5 million tonnes in 2024, following 7% y-o-y growth in 2023.

• Consumption ex. China grew by 3% y-o-y to 1.0 million tonnes, following a 5% y-o-y rise in 2023.

• China’s 3% y-o-y growth brought its total consumption to 0.6 million tonnes.

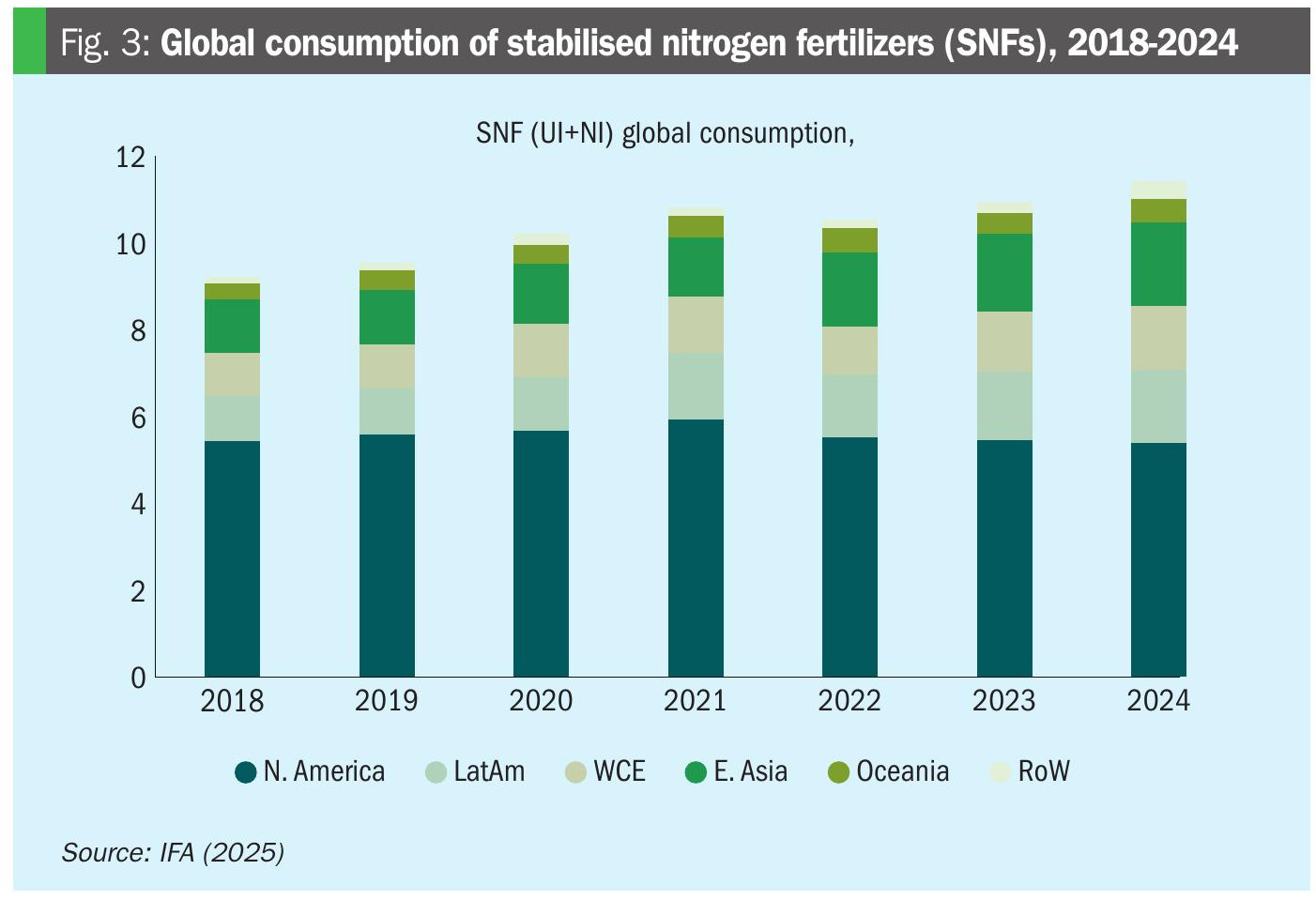

SNF consumption increasingly significant

Across the globe, consumption of stabilised nitrogen fertilizers (SNFs) reached 11.3 million tonnes in 2024 (Figure 3) – divided between 8.1 million tonnes for fertilizers stabilised with urease inhibitors (UIs, +3% y-o-y) and 3.2 million tonnes for fertilizers stabilised with nitrification inhibitors (NIs, +2% y-o-y). Two regions, North America and East Asia, account for 60% of global SNF consumption. Within East Asia, China’s SNF consumption has now risen to 1.7 million tonnes – due to a regulatory push by government and a general growth in nitrogen fertilizer consumption post-Covid – with usage split between 1.1 million tonnes of UIs (+5% y-o-y) and 0.6 million tonnes of NIs at (+6% y-o-y).

Market growth for SNFs is relatively concentrated globally, with three regions – East Asia, Western and Central Europe (WCE), and Latin America – accounting for 90% of the total global increase in 2024. Various market factors are at play. In Latin America, SNF adoption is largely being driven by farm economics and the desire for higher yields – rather than tighter environmental regulation – whereas growth in Western and Central Europe is conspicuously policy-driven. In the UK, for example, new government guidance and voluntary initiatives to reduce land-based emissions have pushed UI adoption rates to 36% of applied urea, versus 20% in previous years. While New Zealand’s adoption rate for UIs of 55% remains at the upper end globally, this is still below its 2022 peak of 60%.

The proportion of urea and urea ammonium nitrate (UAN) treated with urease inhibitors (UIs) – while only accounting for 6% of total urea plus UAN product consumption in 2024 – has grown steadily over the past six years, with UI usage increasing at a cumulative annual growth rate (CAGR) of 3% between 2018 and 2024. Penetration rates for UI usage (as a percentage of total urea plus UAN consumption) vary regionally as follows:

• North America, 16%

• Western & Central Europe, 14%

• Latin America, 11%

• Oceania, 11%

• East Asia, 4%

• Africa, 2%

• South Asia, 0%.

The regulatory environment governing the use of UIs is also a patchwork globally:

• Legally-binding regulations on inhibitor use with fines and compliance checks: Netherlands, Denmark, Germany and Ireland.

• Inhibitors strongly encouraged via incentives and subsidies: France, Austria, Finland, Belgium, UK and Spain.

• Voluntary/industry-led initiatives: Poland, Canada, New Zealand, Australia and South Korea.

• Either no regulations or regulations under development: US, China, Brazil, India and Japan.

Increased uptake of UIs faces the following challenges, according to market participants: unclear yield results in trials; upfront investment costs; affordability in price-sensitive markets; and regulatory hurdles.

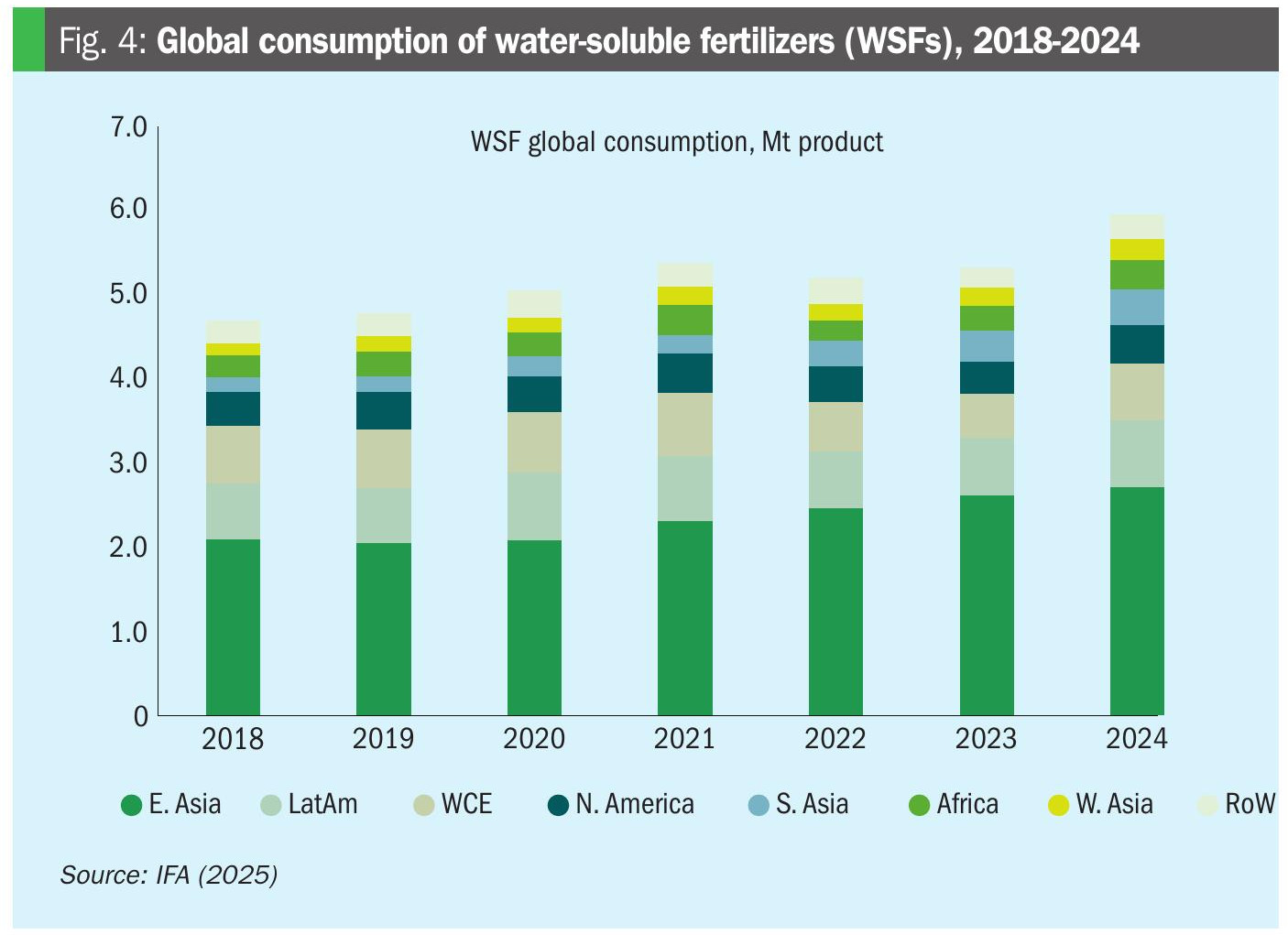

Robust water-soluble fertilizer (WSF) demand

Consumption of WSFs is linked to their delivery via micro-irrigation (drip irrigation) and greenhouse farming systems. China and India, the two countries with the largest crop areas under micro-irrigation, have both benefitted from government support for these systems. Other factors, such as the crop mix and market acceptance of enhanced efficiency products, also act as demand drivers for WSFs. Locally, soil conditions, water quality and fertilizer availability can also promote WSF uptake.

Global demand for water-soluble fertilizers (WSFs) grew sharply by 12% y-o-y to reach 6.0 million tonnes in 2024 (Figure 4), versus the much more modest y-o-y rise of 3% seen in 2023. Consumption in 2024 was boosted by stock drawdown and improved affordability – following two challenging years (2022 and 2023) of demand disruption, supply chain issues, poor affordability and stock carryover.

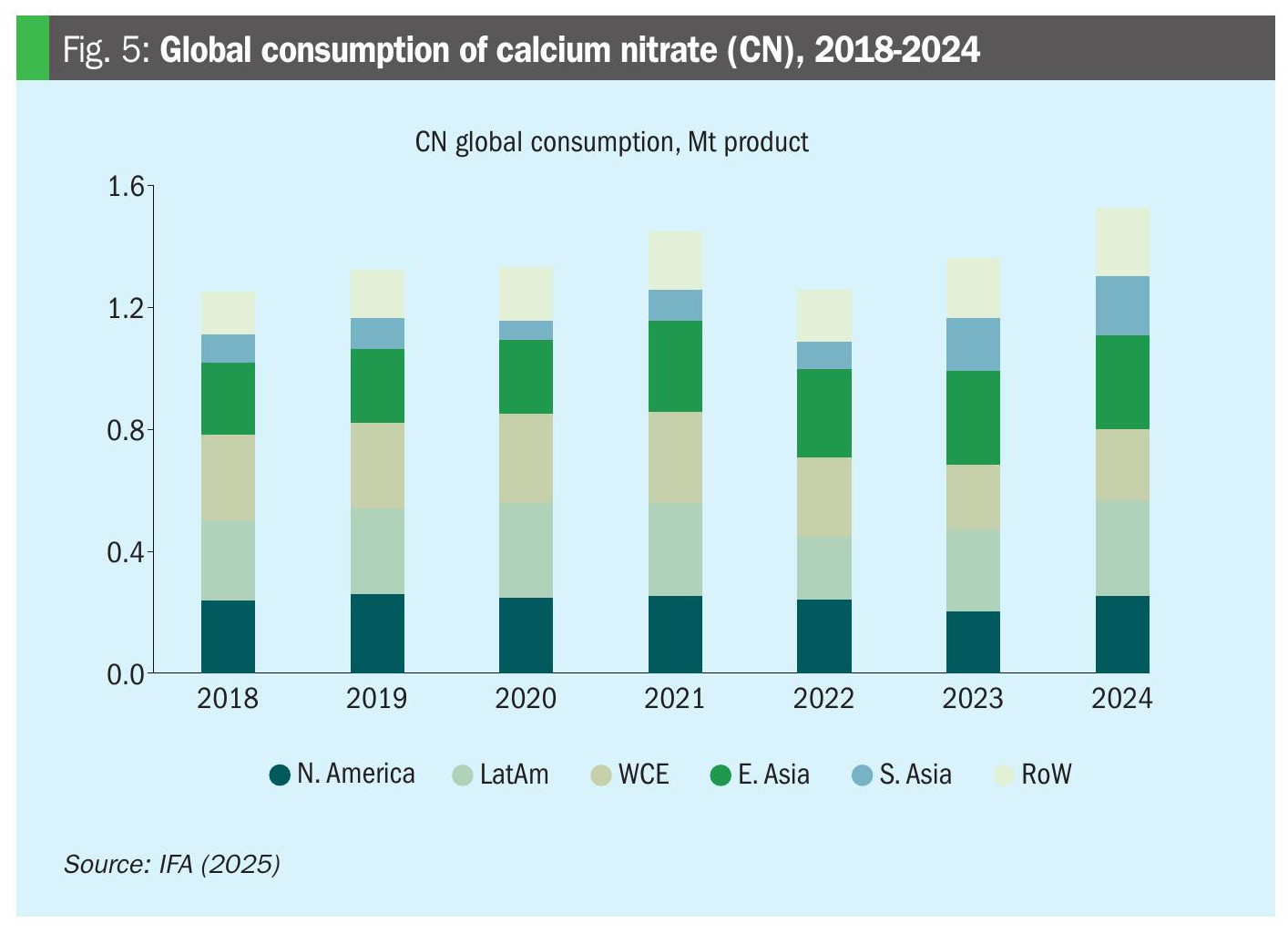

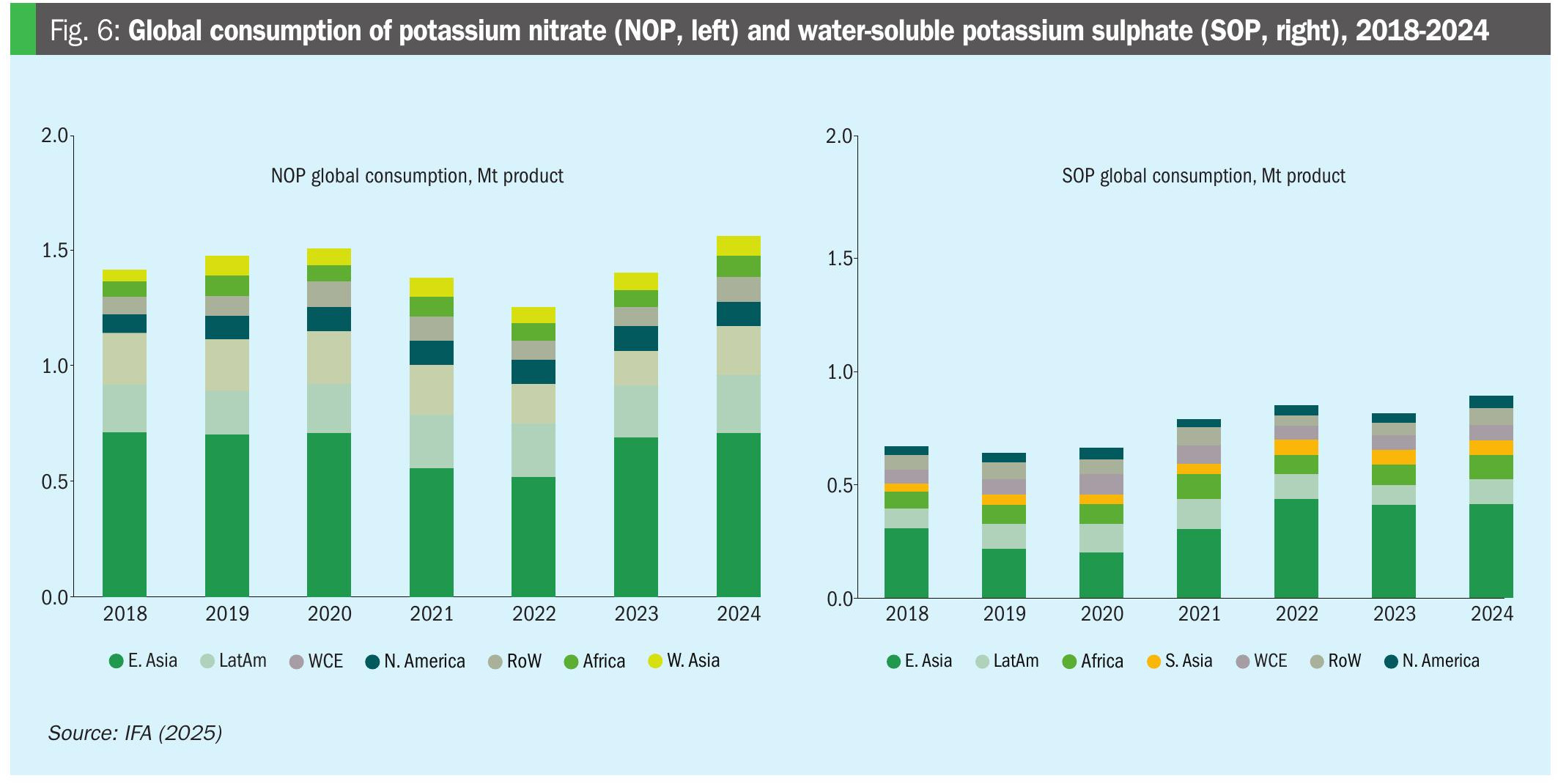

Globally, calcium nitrate (CN) consumption reached 1.5 million tonnes in 2024 (Figure 5), a 12% y-o-y increase, with WSFs accounting for 50% of global CN demand, according to IFA (excluding the liquid CN market in the US). Potassium nitrate (NOP) consumption, in comparison, is estimated at 1.6 million tonnes and water-soluble potassium sulphate (SOP) consumption at 0.9 million tonnes in 2024, with usage of these two products having risen by 11% and 8%, respectively, y-o-y (Figure 6).

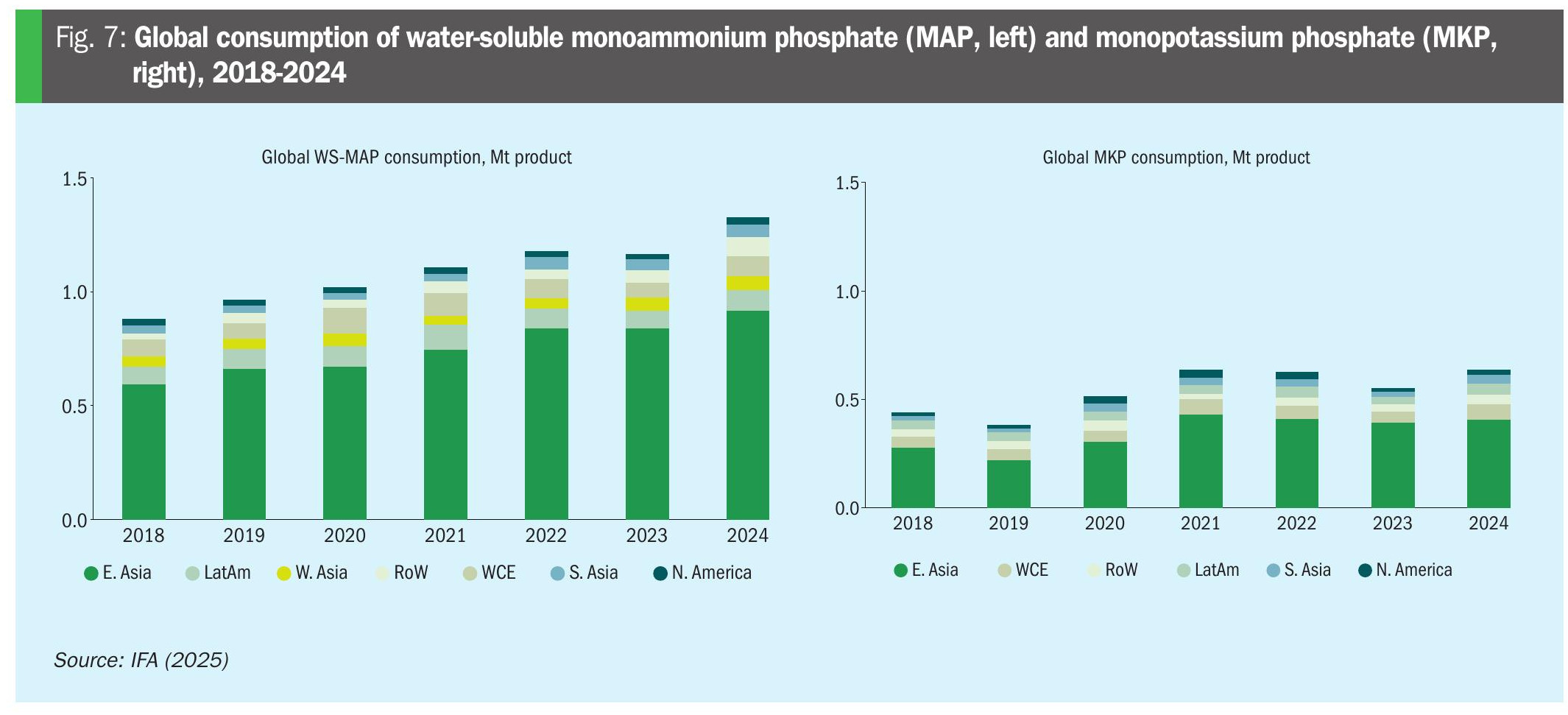

The usage of water-soluble phosphate products grew particularly strongly in 2024. The consumption of water-soluble mono-ammonium phosphate (MAP) – also known as technical monoammonium phosphate (tMAP) – increased by 13% y-o-y to 1.3 million tonnes, for example, while monopotassium phosphate (MKP) consumption grew by 15% y-o-y to reach 0.6 million tonnes (Figure 7). Water-soluble MAP and MKP prices normalised in 2024 – following a large downwards correction from the price levels seen in 2022 – with improved affordability contributing to demand growth for both products.

China has traditionally been the world’s largest exporter of tMAP. However, the introduction of formal export controls and growing demand from the country’s domestic battery market have restricted export availability in recent years. The resulting reduction in Chinese supply internationally has spurred investment in tMAP capacity in Russia, Europe and Morocco.

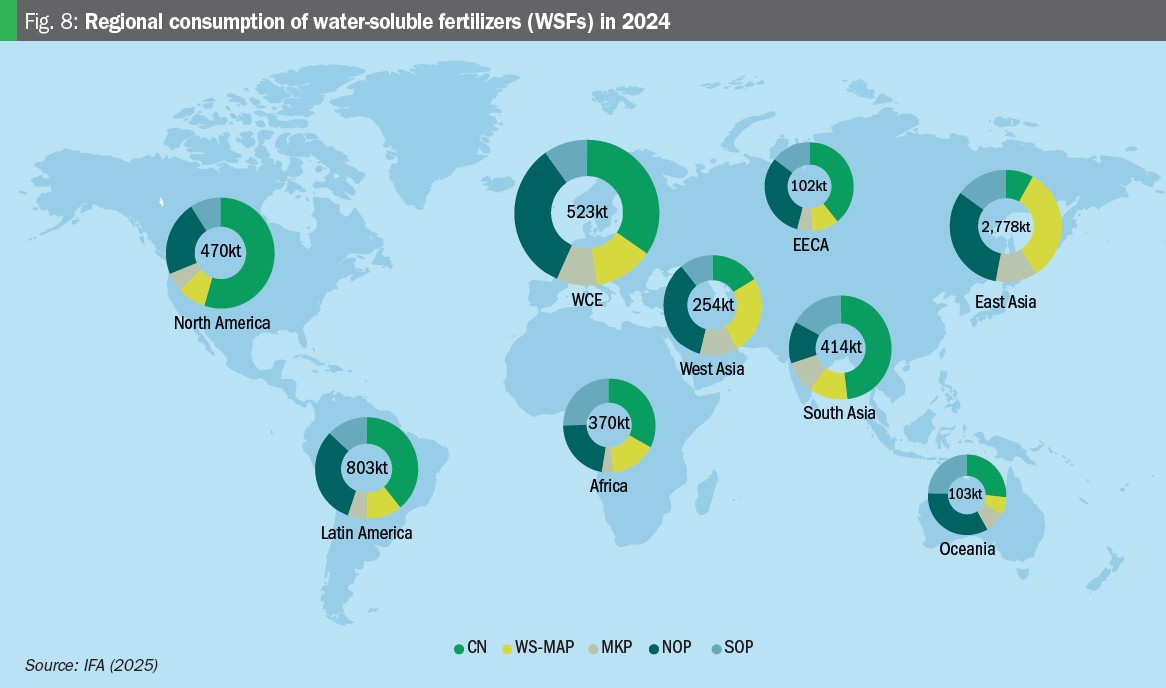

International demand growth outside China has underpinned what is being seen as a return to normal WSF market fundamentals in 2024, after two preceding years of either falling (2022) or flat (2023) growth. Regionally, East Asia is the leading market with consumption of 2.8 million tonnes accounting for more than two-fifths (43%) of total WSF consumption (Figure 8). In China, WSF consumption grew by 4% – a lower rate than in preceding years – to approximately 2.6 million tonnes in 2024. The long term growth of WSF usage in China has been linked to the adoption of more sophisticated fertigation equipment and technology. Alongside this, the promotion of high intensity cropping systems since the early 2020s has also supported demand, as these systems typically use drip irrigation/fertigation equipment which favours the use of WSFs.

“India’s rapid expansion of micro-irrigation in recent years has been a major catalyst for the growth of water-soluble fertilizers,” IFA’s Rajiv Ram commented. “Among these, calcium nitrate holds the largest share of the WSF market and has grown at an annual growth rate of around 15% over the past five years.”

DEFINITIONS, COVERAGE AND METHODOLOGY

IFA’s 2024 assessment of specialty fertilizer demand1 covers three product segments:

Controlled-release fertilizers (CRFs). As their name suggests, these release nutrients from granules into the soil solution at a controlled rate via a polymer or sulphur coating. Products include polymer-coated urea (PCU), polymer-sulphur-coated urea (PSCU), and other polymer-coated straight fertilizers and NPKs.

Water-soluble fertilizers (WSFs). These solid products are mainly crystalline, highly water-soluble and contain one or more nutrients. Very low insoluble content (less than 1%) allows their use in fertigation (the application of nutrients dissolved in water via a drip irrigation system) and foliar fertilization (the spraying of nutrient solutions onto plant leaves). IFA’s assessment focuses on calcium nitrate (CN), monoammonium phosphate (MAP, water-soluble grade 12-61-0), monopotassium phosphate (MKP), potassium nitrate (NOP) and water-soluble potassium sulphate (SOP).

Stabilised nitrogen fertilizers (SNFs). This market segment is divided between two product categories. Firstly, nitrogen fertilizers treated with a urease inhibitor (UI) to reduce ammonia volatilisation by slowing down hydrolysis by the urease enzyme. UI’s include NBPT, N-(2-nitrophenyl) and NPPT. Secondly, nitrogen fertilizers treated with a nitrification inhibitor (NI) that helps prevent the biological oxidation of the ammonium form of nitrogen to the nitrate form. NIs include DCD, DMPP, nitrapyrin and acetylene.

IFA’s specialty market assessment covers 40 countries which collectively account for the majority share of total global consumption, according to the association. Estimates of China’s specialty fertilizer demand are provided to IFA by the China National Chemical Information Centre (CNCIC).

China and the Americas drive controlled-release fertilizer (CRF) growth

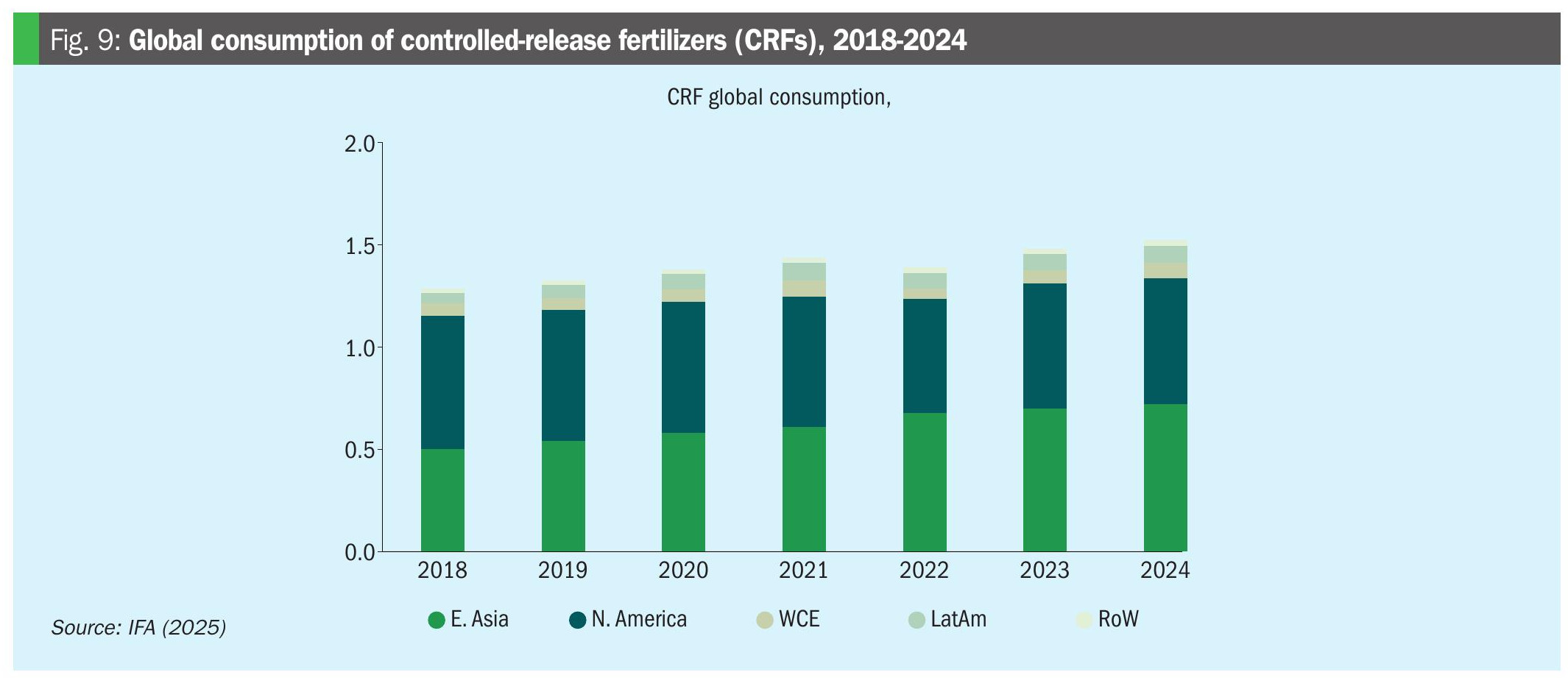

While growth slowed in 2024, global consumption of controlled-release fertilizers (CRF) still increased by 3% y-o-y in 2024 to reach 1.5 million tonnes (Figure 9), driven by a range of regional trends and market dynamics. The key drivers of CRFs demand include: yield improvement; cost efficiency (from reduced application frequency); and environmental compliance. CRFs are a price sensitive market, according to IFA, as shown by the decline in sales volumes that accompanied the price hikes of 2022.

Regional trends in CRF usage are as follows:

• China and North America are the first and second largest consumers of CRFs, respectively, each accounting for around 40% of total demand.

• North American demand grew by 2% y-o-y to 0.6 million tonnes in 2024. CRF consumption in the region is increasingly moving beyond the traditional turf and ornamental market and into agriculture, with usage rising in broadacre and specialty crops.

• CRF demand in China is estimated at 0.6 million tonnes in 2024, a 3% y-o-y increase, driven by rising usage on cash crops in the country’s more intensively farmed northern agricultural regions.

• West and Central Europe (WCE) experienced high consumption growth of 6% y-o-y in 2024, with environmental regulations and farming efficiency goals being the main drivers.

The expected impact of the EU’s introduction of a biodegradability requirement for CRF polymers from 2028 was cited as significant by market participants. They also commented that food producers may drive the adoption of biodegradable CRFs in future, as part of efforts to reduce their supply chains emissions.

“In 2024, all specialty product categories continued their upward growth, with water-soluble fertilizers emerging as a particularly strong performer, achieving an estimated 12% year-on-year growth.

Key report takeaways

• Stabilised nitrogen fertilizers (SNFs): This market segment is characterised by stable global growth, with overall adoption rising in response to tighter regulation and a wish to improve nutrient use efficiency. Strong demand in the two key volume markets – the Americas and East Asia – is, however, being driven by agronomic/economic reasons rather than by regulatory requirements.

• Controlled-release fertilizers (CRFs): China and North America remain the largest contributors to CRF demand with 2024 growth boosted by improved affordability. Implementation of the EU’s biodegradable CRF policy by 2028 could cause a shift in market demand.

• Water-soluble fertilizers (WSFs): Growth in calcium nitrate (CN) consumption in South Asia, especially India, is being driven by an expansion in the fertigation area. China’s redirection of water-soluble (technical) monoammonium phosphate (MAP) to industrial uses, together with export restrictions, is resulting in investments in production capacity elsewhere. Demand for water-soluble MAP and monopotassium phosphate (MKP) is growing strongly, particularly in regions outside of China. ■

References