Sulphur 423 Mar-Apr 2026

23 March 2026

Sulphuric acid in South America

SULPHURIC ACID

Sulphuric acid in South America

While Brazil is the largest consumer, trade in acid in South America has been dominated by Peru and Chile.

South America is a relatively small part of the overall sulphuric acid market, consuming about 19 million t/a of acid, or 6% of all production, split roughly evenly between Brazil’s phosphate fertilizer industry and the copper industries of Chile and Peru. However, Chile’s considerable need for acid for copper leaching operations makes it one of the largest importers of acid worldwide, and makes the continent a significant factor in global acid trade.

South America is a relatively small part of the overall sulphuric acid market, consuming about 19 million t/a of acid, or 6% of all production, split roughly evenly between Brazil’s phosphate fertilizer industry and the copper industries of Chile and Peru. However, Chile’s considerable need for acid for copper leaching operations makes it one of the largest importers of acid worldwide, and makes the continent a significant factor in global acid trade.

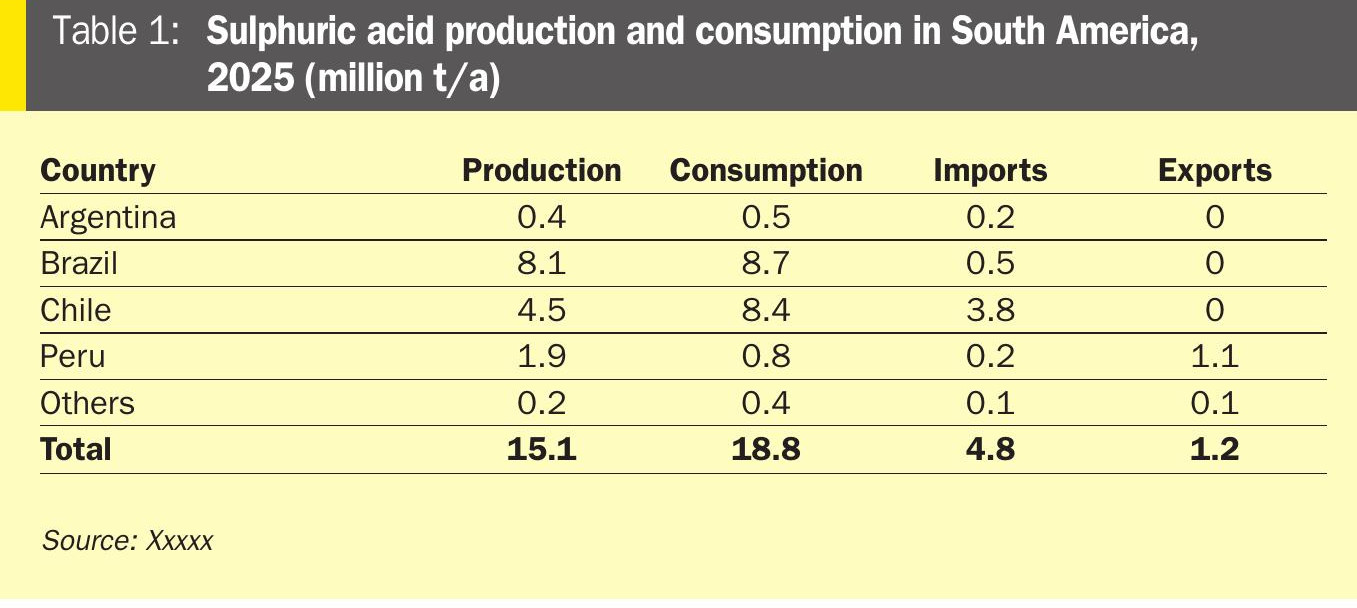

As Table 1 shows, the major producers are Brazil, Chile and Peru. However, there is considerable difference in how that acid is generated. Brazil only has around 300,000 t/a of smelter acid production, and relies upon sulphur burning acid plants to produce all of the acid for its phosphate plants. Chile and Peru, conversely, generate most of their acid from copper smelting. Chile imports large volumes of acid, mainly from neighbouring Peru, as well as Japan, South Korea, China and Mexico.

Brazil

Brazilian phosphate demand continues to climb, and with it phosphate production and demand for sulphuric acid. Most Brazilian acid production is fed from imported sulphur. Brazil imported 2.3 million t/a of sulphur in 2025, 95% of it to manufacture single superphosphate (SSP) and mono-and diammonium phosphate (MAP/DAP) fertilizer production. Sulphur consumption is set to increase as the phosphate sector continues recovering and a new phosphate plant continues its initial ramp-up. Euro-Chem’s Serra do Salitre phosphate plant was launched in mid-March 2024, and it was expected to reach full output by the end of 2025. The facility will add an additional 330,000 t/a of sulphur consumption to Brazil. Growing demand is expected to maintain import growth throughout the rest of the decade, with Brazilian sulphur imports reaching 2.9 million t/a in 2030, feeding total acid production of 9.6 million t/a in that year. Imports of sulphur are forecast to climb in 2026, despite an expected slower rate of demand in 2026 Q1.

Chile

Chile’s acid position is dominated by the copper market. Chile holds the world’s largest share of known copper reserves, at 21.3%, according to the United States Geological Survey (USGS). Chile also represents about 25% of global copper output, mainly in the north of the country. Copper markets, although volatile, have generally been buoyant over the past few years with prices high, assisted by supply disruptions among major producers (including Chile) and a weak US dollar. Copper prices of around $12,000/t have been seen at the end of 2025 and into 2026. Copper demand is expected to grow 2.6% annually out to 2030, outpacing supply growth of 2.4%, mainly due to Chinese demand, particularly for electric vehicles, leading to projected deficits forecast for remainder of the decade. However, part of the reason for this mismatch between supply and demand has been falling copper production from Chile. Copper cathode production in Chile has actually declined over the last decade, from 1.8 million t/a in 2015 to 1.2 million t/a in 2025 – a 3.8% annual fall. Much of this has come from ageing mines and falling ore grades. News that Codelco and Glencore will partner on a new smelter and cathode refinery in the Antofagasta region is a positive for Chilean refined copper production, although with construction not expected to start until 2030, it sits beyond the medium term forecast.

In spite of this fall in output, Chile’s sulphuric acid consumption has remained broadly stable at an average of 8.2 million t/a. This is due to an increase in the consumption ratio from acid leaching projects, which has risen from an average 4.5 tonnes of acid being required to generate each tonne of copper in 2015 to 6.9 tonnes of acid per tonne of copper in 2025, as ore grades fall. Continued growth in acid demand has thus become increasingly reliant on the start-up of new, high acid consuming projects, as well as the extension of existing assets with high acid demand rates.

Overall Chilean sulphuric acid demand in 2025 was down slightly on the 2024 figure, falling from 8.3 to 8.2 million t/a due to some maintenance shutdowns at existing operations. This is expected to recover in 2026 to 8.4 million t/a, driven by a rebound in demand at the Radomiro Tomic and Mantoverde projects, although the closure of the Mantos Blancos site will partially offset overall copper performance, and there will be a continued decline in demand from existing copper operations. The reduction of these will be recorded from the Centinela and Chuquicamata project, with a total 300,000 t/a of acid demand being lost, while acid consumption at Radomiro Tomic is expected to rebound by 200,000 t/a. Looking forward, the project landscape is composed of a mix of restarts or extensions of existing assets, and projects deploying alternative leaching technologies. Extensions are planned at Spence and El Abra, for example, although this will only serve to maintain acid demand at its current level.

Chilean acid consumption is set to continue increasing throughout 2030. The Marimaca project, expected to start operations by 2028, will add 400,000 t/a of acid consumption. Additionally, the sulphide leaching at Gaby (expected to start in 2029) and the Collahuasi bioleaching project (anticipated to come online in 2028) are forecast to add 100-200,000 t/a of new acid consumption by 2030. Region II (Antofagasta) is expected to increase acid consumption to 7.50 million t/a by 2030 from 6.77 million t/a in 2025. Supply in Region II is also expected to climb, but at a slower rate, with output up from 2.53 million t/a in 2025 to 3.13 million t/a in 2030.

Supply will also increase more generally. In part this will be due to the start of the proposed Marimaca sulphur burner but also an anticipated increase output at smelters. The unplanned outages at the Altonorte (2025 Q2) and Potrerillos (2025 Q3) smelters cut a total of around 300,000 tonnes of acid supply last year. The Altonorte issue triggered buyers to commit to new imports, which pushed 2025 Q2 arrivals to a 6-year high. Total imports for 2025 reached 3.8 million tonnes, representing a 10% increase year on year. Smelter availability is expected to recover in 2026 once the supply disruptions ease, which will reflected in lower import requirements. Supply is also expected to increase in central Chile with production recovery expected at Codelco’s Caletones smelter in Region 6. However, long-distance imports will still be required in the country, as supply is only anticipated to grown moderately. The result is that the requirement for imports is expected to increase, with a combination of European and Asian volumes necessary to meet demand needs. At the same time, Peruvian volumes available for the Chilean market are expected to decline with the start-up of the Tia Maria project, which will consume around 600-700,000 t/a of acid from 2028 (see below).

Peru

Like Chile, Peru’s acid industry is dominated by copper extraction. Peru is the world’s second-largest copper producer, with production approximately 2.8 million t/a in 2025, supported by major operations like Cerro Verde, Antamina, and Las Bambas. While output increased 1.6% across 2025, production faces a plateau due to a lack of new, large-scale projects and declining ore grades. However, there is positive news on the horizon, with the long-delayed Tia Maria mine expected to be commissioned in late 2027. The project is expected to add 800,000 t/a of acid demand, accounting for 60% of Peru’s total consumption. Other demand is expected to decline as existing mines reduce output and cut acid consumption by 2030.

Peruvian smelter acid production will remain broadly stable though the medium term, and will be sufficient to meet increasing domestic demand. The ramp-up of the PetroPeru facility will add around 100-200,000 t/a of supply by 2026, increasing exports in the short term. But once Tia Maria starts up, export volumes are expected to fall to around 700,000 t/a from 2028. This will reduce Peruvian supply into Chile. While the long-running relationship between Peruvian acid surplus and Chilean consumers will remain intact, the scale of demand that Peru can serve will fall. Peru is also expected to remain a minor acid import destination with the Mina Justa operation currently engaged in around 300,000 t/a of international trade.

Argentina

The sulphuric acid market structure in Argentina has been mainly focused on single superphosphate manufacture and some industrial-based consumption, with an annual demand of around 500,000 t/a. However, new copper-based consumption is expected to double Argentina’s acid demand by 2030. The start-up of McEwen’s Los Azules copper project will significantly boost acid demand in the country. Construction is expected to begin in 2026, with a target for initial production by 2030. Acid demand from the project is anticipated to reach 400,000 t/a, doubling the country’s total acid consumption in 2025. The project is expected to include a sulphuric acid plant at peak consumption, sourcing 800,000 t/a from the burner. Therefore, acid needs are expected to be largely met by local acid availability, with a minor impact on the traded market.