Sulphur 423 Mar-Apr 2026

23 March 2026

Price Trends

Price Trends

SULPHUR

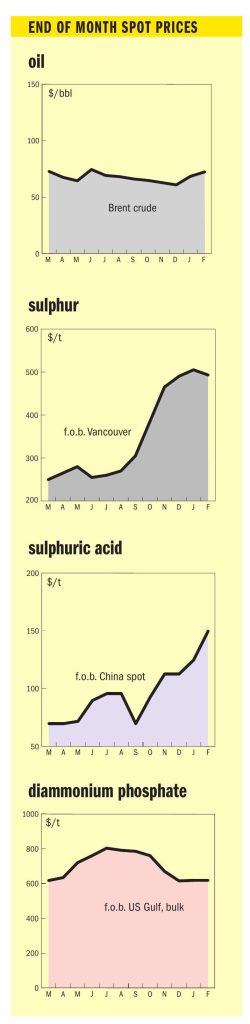

Conflict in the Middle East has halted all vessel traffic through the Strait of Hormuz, effectively paralysing a region that accounts for 48% of global seaborne sulphur trade. As a result, the sulphur spot market has ground to a halt, with prices notionally holding unchanged in the $490-515/t f.o.b. range simply due to a lack of activity. No spot offers were reported out of the Middle East.

Reflecting the paralysis, producers either delayed or did not post their March sulphur selling prices. After an initial delay, QatarEnergy eventually announced its March price as a rollover at $520/t f.o.b. Market sources have since confirmed that ADNOC (UAE) has also settled its March price at a rollover from February at $530/t f.o.b. on 5 March. This counters earlier market expectations, which had pointed towards a downward correction for March before the conflict escalated. Of the major producers, only KPC (Kuwait) had yet to announce its price at the time of publication. Amid the standstill, only one spot transaction has been reported since the conflict escalated: a 20,000 tonne Bahrain-origin cargo, which was sold to China at $555/t c.fr, reflecting the extreme premium required to secure any volume from the region. As the latest freight rates from the Middle East to China are unclear, the range was unchanged.

The reaction across major import markets has been varied. In China, the uncertainty prompted a sharp upward adjustment in domestic port pricing, reaching their highest levels since 2008; c.fr levels reached $550-560/t, up from $515-520/t. Domestically, the port spot price surged by $65/t from 27 February to a peak of $651/t on 4 March. Recent trades supporting these levels include 20,000 t of Bahrain-origin product sold at $555/t c.fr on the Changjiang river. The price surge is creating significant pressure on downstream phosphate producers. With sulphur now trading above domestic DAP and MAP prices, many are monitoring the situation closely rather than rushing to purchase. Large producers with existing inventories or access to cheaper domestic refinery sulphur are not under immediate pressure. In contrast, smaller MAP producers are facing potential production cutbacks due to poor affordability. Consequently, most port transactions are currently concentrated among traders. The geopolitical uncertainty has also weakened sentiment around China’s 2026 phosphate export outlook, further reducing producers’ buying interest. Total port inventories declined by 28,000 tonnes to 1.725 million tonnes by 5 March. The volume at Yangtze River ports saw the largest drop, decreasing by 24,000 tonnes to 702,000 tonnes, while Dafeng port’s inventory remained stable at 140,000 tonnes.

In contrast, other key importers have adopted a more cautious, “wait and see” approach in a market where demand was already softening due to persistently high prices. This is particularly true in India and Indonesia, two markets heavily reliant on Middle East supply, where buyers have retreated to the sidelines to await clarity. According to the latest trade data, Indonesia imported 378,096 tonnes of sulphur in January, with approximately 78% of that volume sourced from producers in the Middle East, now directly impacted by the halt in shipping.

The market in Brazil remains quiet, though this is more attributable to a preplanned period of maintenance at major fertilizer plants. Interest naturally turned to alternative sources, but buyers found limited options. Enquiries for North American cargoes increased, but suppliers in Canada and the US Gulf were already largely committed for the coming months. The global supply picture is further constrained by ongoing logistical issues, including heavy ice in the Baltic Sea and security risks in the Black Sea.

Mediterranean markets were quiet, with buyers in Turkey absent due to a lack of ammonia, and Tunisia out of the market, with the country’s phosphate sector still navigating the fallout from a general strike at Groupe Chimique Tunisien (GCT) sites in mid-February.

SULPHURIC ACID

In spite of the chaos in other markets, the global sulphuric acid market has largely continued ‘business as usual’, with the immediate impact of the Middle East conflict confined to isolated logistical disruptions. This stands in stark contrast to the sulphur market, where the conflict has effectively halted 48% of global seaborne supply, while the wider acid market watches for potential ripple effects.

The most direct logistical impact has been on Saudi Arabia’s Maaden, a major importer now unable to receive shipments. This blockage, particularly of cargoes from India, has become the catalyst for a rerouting of trade. In response, Indian buyers are reportedly pushing back on their own contracted March volumes from Asia. This has reportedly created unexpected prompt availability in the Far East, easing the narrative of acute tightness that had previously defined the Japan/South Korea market and prompting Chinese traders to actively seek new outlets for surplus tonnes.

Traders are now looking to place these newly available Asian cargoes into Chile, but this is being met with weak local demand due to ongoing mine maintenance, keeping the Chilean market stable for now. Spot prices for sulphuric acid to Chile were assessed as stable at $190-200/t c.fr, with the market balancing weak local demand against firm international replacement costs. The domestic market is currently well-supplied, with some buyers reportedly trying to delay incoming shipments. High stock levels have been compounded by recent operational issues at some major mines, which have temporarily reduced acid consumption over early Q1. As a result of the current slowdown, most buyers are reportedly covered until at least April and will not be looking for new spot cargoes for delivery earlier than June/July. Meanwhile, the Middle East conflict has altered some trade flows in the acid market. The disruption to the India-to-Saudi Arabia route has prompted traders to redirect spot cargoes from the Far East towards South America. A 30,000 tonne cargo was reportedly fixed to load in mid-April from Fangcheng, China, for delivery to Mejillones. However, with freight for that route estimated at $91-101/t, the landed cost from China is calculated in the $241-261/t c.fr range, based on a Chinese f.o.b. of $150-160/t, making it largely uncompetitive.

In Brazil, the market is also quiet due to local turnarounds, but forward sentiment has firmed considerably, with offers for May/June arrival rising on the perceived risk to future supply. In Northwest Europe, the market remains tight and sold out until April, which is the primary factor holding prices stable at $120-125/t f.o.b. The market remains underpinned by tight availability, with a consensus among sources that nearly all spot volumes are sold out through April. This scarcity is providing a firm floor to prices and has intensified talk around $130/t f.o.b. and above for any forward deliveries. While Europe has not been directly impacted by the trade flow disruptions stemming from the Middle East conflict, the global uncertainty is helping to support the firm sentiment in an already tight market.

In India, the market is under pressure. While subdued local demand has kept the weekly assessment stable at $170-180/t c.fr in early March, offer levels tightened due to rising feedstock costs and geopolitical risk. Heightened Middle East tensions have complicated feedstock flows. Traders report cargoes that had been bound for Maaden in Saudi Arabia are now stranded, prompting distressed sales into the market at roughly high $160s/t c.fr. Those forced disposals are available only in limited parcels, and many importers lack storage or the appetite to take on distressed material at present, given tight working capital and maintenance planning. Importers are entering their annual maintenance windows, reducing immediate procurement urgency. Several buyers say they are sufficiently covered with on-site stocks to bridge the shutdown period and will rely on those inventories rather than lift new spot cargoes. That dynamic limits immediate demand even as feedstock costs and geopolitical risk keep upward pressure on offers.

Sellers in Japan and Korea are reported to have only limited volumes available for new allocation, while China remains absent from spot exports. A handful of traders retain positions, but low acceptance rates among importers have left those parcels largely unsold. Physical flows through mid-February confirm the tighter backdrop. India imported around 67,000 tonnes of sulphuric acid to mid-February, with over 82% of that volume directed to CIL and the balance to FACT, according to vessel tracking data. With arrivals modest and bid acceptance weak, the market balance is fragile: limited spot liquidity and elevated offer levels leave importers reluctant to buy, yet any disruption to contracted flows could prompt rapid repricing.

Price Indications