Fertilizer International 531 Mar-Apr 2026

20 March 2026

Market Insight

Market Insight

PRICE TRENDS

Market snapshot, 26th February 2026

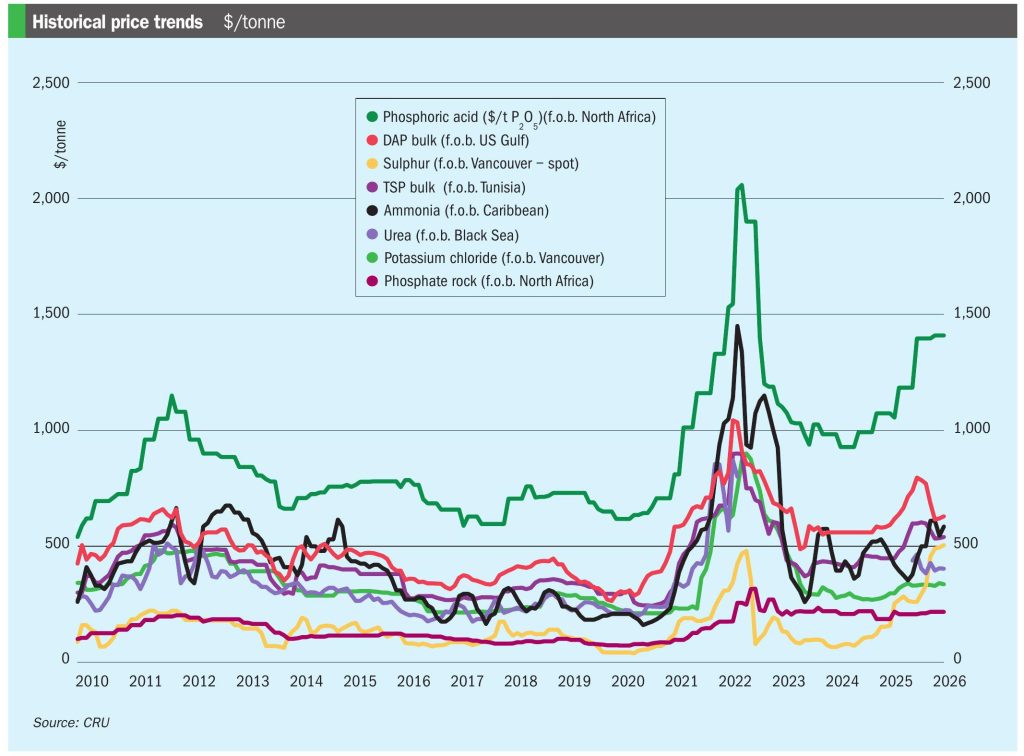

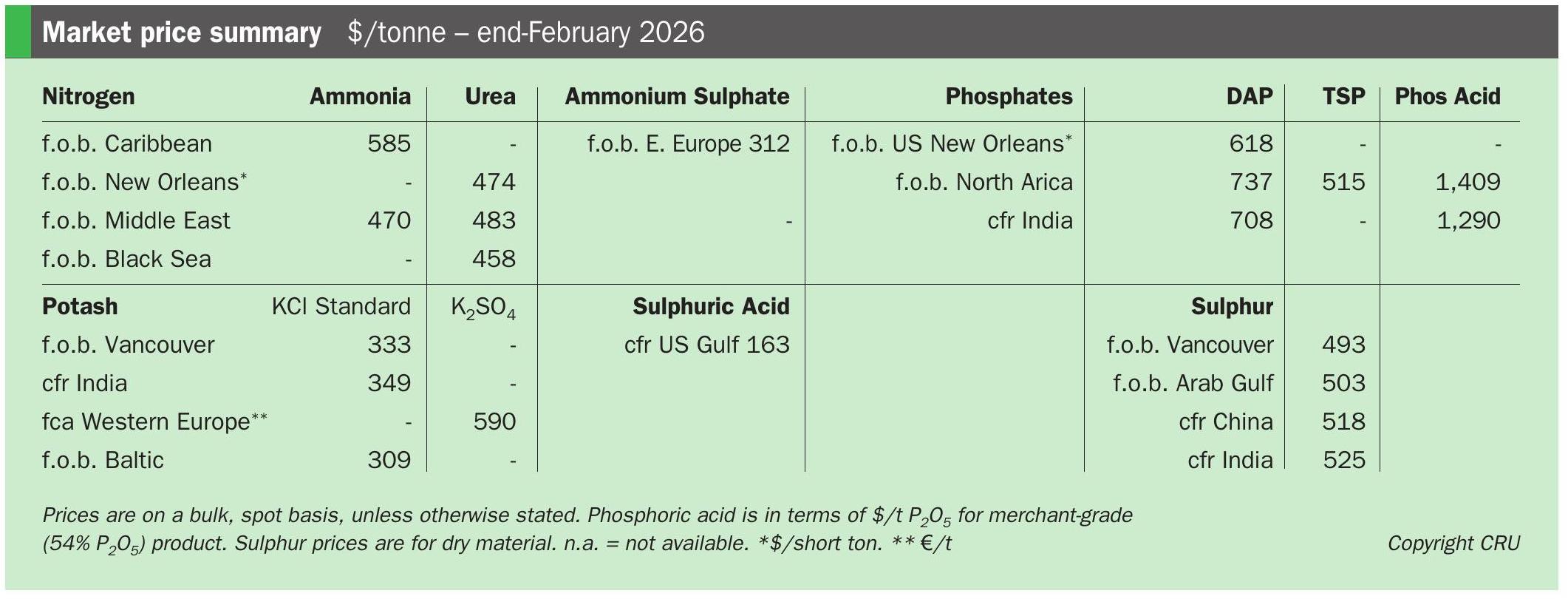

India’s purchase tender sets urea market tone. The urea market was dominated by the conclusion of Rashtriya Chemicals and Fertilizers Limited’s purchase tender on 18th February. RCF secured just over 1.3 million tonnes of urea at the lowest offer prices of $508/t cfr west coast and $512/t cfr east coast.

Middle East urea prices have firmed to $490-495/t f.o.b., aligning with netbacks from the RCF tender, with Fertiglobe set to ship around 180,000 tonnes from the UAE. In Iran, Pardis sold two 50,000 tonne granular cargoes to Turkey at $430/t f.o.b.

In Southeast Asia, Indonesian urea producer Kaltim sold 45,000 tonnes granular to Ameropa in the low-$490s/t f.o.b. for March shipment. In Brunei, BFI is understood to have sold 30,000 tonnes granular to Indagro in the high-$490s/t f.o.b., also for March.

West of Suez, two Egyptian producers sold a combined 30,000 tonne granular shipment to the US at $485/t f.o.b., with Mopco selling a further 10,000 tonnes at $490/t f.o.b. NCIC was said to have awarded its 19th February sales tender at $488/t f.o.b., amid speculation the 20,000 tonnes offered will be directed to India.

Ammonia divided between firmer west and softer east. The global ammonia trade continues to show a clear east-west divide. West of Suez, prices remain underpinned by constrained availability, while the market east of Suez is weighed down by ample availability and weak spot demand.

In the US and Caribbean, new guidance from Nutrien confirmed the removal of 1.6 million tonnes of sales volumes from its portfolio in 2026, on the assumption of no ammonia production from its Point Lisas, Trinidad, and New Madrid, Missouri, production plants. This helps explain the continuing ammonia supply tightness felt west of Suez.

East of Suez, the Middle East price spread for ammonia remains wide. Although supply continues to stay long, buying interest west of Suez has helped support westbound offers. India has reinforced the east of Suez softness, with buyers there increasingly eyeing up Indonesian tonnes, as Southeast Asia values continue to trend lower and availability remains comfortable.

Phosphate prices firm on supply scarcity. Global DAP and MAP prices have continued to increase. Bullish sentiment is being driven by an exceptionally tight supply outlook and high raw materials prices, with these offsetting seasonally slow demand and affordability concerns.

Prices in key MAP import market Brazil moved higher, continuing a trend of ascending prices seen over seven of the last eight weeks. MAP prices were assessed at $730-740/t cfr, their highest level since August 2025 and a rise of 16% ($100/t) over the year to date.

Prices in the key DAP market India were also up at $705-710/t cfr, despite a dearth of deals, with some sources pegging prices as high as the $720s/t cfr. Latest business to Pakistan, which is typically priced at a $10-15/t premium over India, was concluded in the mid-to-high $720s/t cfr for a Saudi cargo, with producer Maaden achieving even higher netbacks on a DAP cargo to Southeast Asia.

Morocco’s OCP, meanwhile, continues to reach higher f.o.b. sales on small-volume shipments to Europe. In the US market, on the other hand, DAP prices at NOLA softened to $615-620/st f.o.b., while MAP prices were steady.

Potash prices stable as seasonal demand builds. Global MOP markets remain firm, with seasonal demand building across key regions and tightening availability shaping sentiment ahead of the second quarter.

In India, the 180-day MOP contract remains unsettled, although market participants expect agreement by the end of March. Suppliers are pushing for an increase from the existing $349/t cfr level, possibly as high as $20/t above this. The outcome of this contract is widely expected to set MOP price direction over the next quarter.

In Brazil, MOP was assessed at $365-380/t cfr. Russian and Belarusian producers are sold out for March and are now taking orders for April, tightening availability.

In Southeast Asia, standard MOP was assessed at $360–390/t cfr and granular at $390-410/t cfr. In China, port wholesale MOP prices were assessed at RMB3,000-3,580/t fca, with modest increases at the upper end of this range due to tight availability. In Europe, meanwhile, MOP prices remain broadly stable, with limited spot deals reported.

Sulphur correction deepens on muted demand. The downward correction in global sulphur prices gathered pace, as hopes for a strong post-holiday rebound in Chinese demand failed to materialise. While one deal was heard at $515/t cfr, interest from Chinese buyers remains sluggish. This has sent a bearish signal through the market, directly impacting prices in Vancouver, which fell to $490-495/t f.o.b. in response.

Price weakness in China, a key destination market, rippled through to other major export hubs. The Middle East f.o.b. assessment fell sharply to $490-515/t. The US Gulf f.o.b. price also softened to $495-500/t, aligning with weaker sentiment in its key export market, Brazil. The CRU European sulphur index, meanwhile, captured this broad-based decline by falling to $498/t.

OUTLOOK

Urea supported in near term. Global demand is expected to support prices in the short term, primarily driven by purchasing from India and Australia. The anticipated return of Chinese exports in the second quarter is then expected to cause a price correction. The upside risk of a bullish natural-gas market on both sides of the Atlantic could, however, see urea costs soar, with the potential for domestic nitrogen production in the US being scaled back in favour of more lucrative LNG exports. Geopolitics could also provide unforeseen price support, particularly with the threat of US military action looming in Iran.

Ammonia on downwards trajectory. The current east-west split looks set to persist into March. Although ammonia prices have been revised higher for February, a general downwards trajectory is forecast through the first half of 2026 as steady supply growth alleviates the prevailing tightness. There is a downside risk that prices could sharply correct lower if Gulf Coast Ammonia and Woodside’s Beaumont project bring meaningful volumes to the market earlier than expected.

Phosphates bullish on tight supply outlook. Given severe export restrictions in China, granular phosphates prices are forecast to climb even higher this year than in 2025, with no respite likely for buyers until the third quarter at least. There is a downside risk that prices could move lower if China’s NP exports are greater than forecast.

Higher first quarter potash prices expected. MOP prices in most regions are forecast to rise in the coming quarter as potash remains the most affordable nutrient, and suppliers are in bullish mood. There is an upside risk that prices may firm more than expected on the back of supplier confidence and stronger demand in most regions.

Sulphur prices peak in February. Sulphur prices are now forecast to peak in February, later than previously anticipated, as ongoing supply disruptions in the Middle East and Kazakhstan continue to support the market. There is an upside risk that prices may not decline as quickly or as sharply as forecast, if ongoing supply disruptions continue to limit the recovery of global export availability.

Note As Fertilizer International went to press, the fertilizer market was reacting to news of hostilities between Iran versus the United States and Israel on 28th February. Stay on top of the latest market developments, plus full analysis, via CRU’s Fertilizer Week service, the industry’s most trusted source: crugroup.com/en/solutions/fertilizer-services/fertilizer-week/