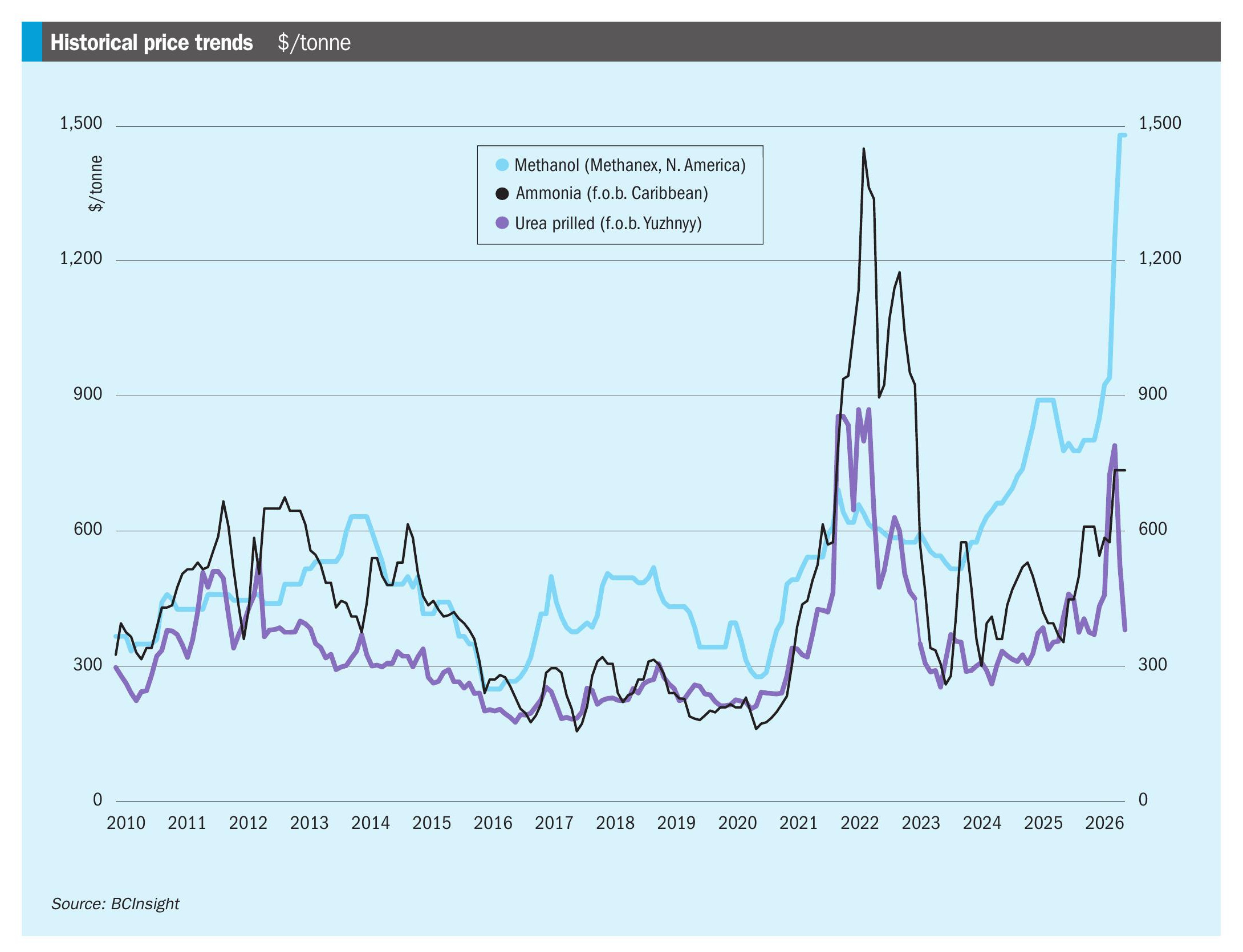

Sulphur 418 May-Jun 2025

3 May 2025

Investment to boost phosphate project

Investment to boost phosphate project

Avenira has secured an A$7.56 million strategic investment from majority shareholder Hebang Biotechnology to progress its Wonarah phosphate project in Northern Territory. The investment, in which Hebang will acquire 1.08 billion shares priced at A$0.007 each, will boost its equity holding in Avenira to 49%. Hebang has also agreed to provide Avenira with an unsecured drawdown loan facility to be repaid on completion of the placement or after the date of the first drawdown.

Avenira will use funds from the investment to advance its Wonarah phosphate project, located between Tennant Creek and Mount Isa. Wonarah is considered Australia’s largest high-grade phosphate project and Avenira plans to develop it as a direct shipping ore (DSO) operation based on a simple open-cut mining operation with processing facilities onsite. Avenira intends to supply premium-quality products from Wonarah, including lithium iron phosphate (LFP), thermal phosphoric acid (TPA) and yellow phosphorus, into the electric vehicle, agricultural and industrial chemical markets.