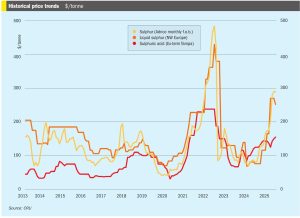

Smelter disruptions reshape 2025 traded acid market

CRU's analyst Viviana Alvarado discusses the effect of smelter outages and maintenance, a copper concentrate shortage, and Asian capacity ramp ups, on sulphuric acid supply and prices.

CRU's analyst Viviana Alvarado discusses the effect of smelter outages and maintenance, a copper concentrate shortage, and Asian capacity ramp ups, on sulphuric acid supply and prices.

Abu Dhabi-based nitrogen producer and distributor Fertiglobe says that it is acquiring the distribution assets of Wengfu Australia Pty Ltd. through an asset sale and purchase agreement, expanding its downstream reach and enhancing access to supplying Australian customers. Fertiglobe currently supplies around 600,000 t/a of urea to Australia, with the potential to grow supply volumes […]

India India has imposed five-year anti-dumping duties on six Chinese imports, including insoluble sulphur, mainly used in the vulcanisation of rubber. The move follows an investigation by India’s Directorate General of Trade Remedies (DGTR) last year, following a complaint by Oriental Carbon and Chemicals in March 2024. The period covered by the investigation was from 1st Jan 2023 to 31st Dec 2023, while the injury investigation period ran from April 2020 to 31st Dec 2023. DGTR made a determination that Chinese exporters had been selling the six products at unfairly low prices, adversely affecting the profitability of Indian producers. DGTR says that the duties it has imposed are “aligned with WTO norms” and aim to protect domestic industries from unfair trade practices and address the growing trade imbalance with China. According to the trade authority, the market share of the countries subject to duties “has been significantly increasing” while local Indian industry’s capacities are “lying idle” amid growing demand. n

New sulphur production from Chinese and Indian refineries and Middle Eastern sour gas and the ramp up of nickel leaching projects in Indonesia continue to change the direction of sulphur trade.

• Global sulphur prices are expected to experience decreases over the next few weeks. Buyers in Asia report that they are covered for contracted supply throughout July, and domestic prices in China are likely to decrease further, putting downward pressure on sulphur prices.

The end of June saw declines in sulphur prices in many regions amid subdued global demand across regions. Most import markets are sufficiently covered through July at least, resulting in limited activity while supply increases. These conditions have exerted downward pressure on prices as bearish sentiment spread across regions.

• The short term outlook appears balanced for the most part, although more bullish participants seem to be holding sway over market sentiment.

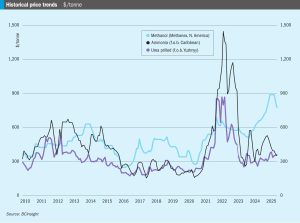

Increased merchant ammonia capacity over the next few years may lead to longer term price declines.

Ju ne saw fertilizer markets – urea markets in particular – thrown into chaos by the widening of hostilities in the Middle East. Israel’s and then the United States’ strikes on Iranian nuclear facilities and the retaliatory attacks on Israel and Qatar for a while held out the potential for the conflict to widen, perhaps even leading to attempts to close the straits of Hormuz at the entrance to the Gulf, something not seen since the ‘tanker war’ of the 1980s when Iraq tried to cripple Iran’s oil exports during the eight year Iran-Iraq War.

The Iran-Israel conflict in mid-June placed the urea market on edge prior to a ceasefire announcement.