Recent developments in sulphuric acid markets

Smelter outages and tight concentrate markets ease an oversupplied market.

Smelter outages and tight concentrate markets ease an oversupplied market.

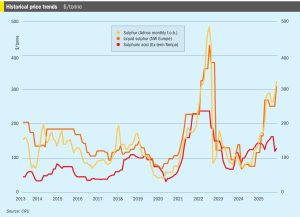

Prices in sulphur markets have been climbing rapidly for several weeks now due to short supply, reaching their highest levels for early two and a half years, since July 2022. A major cause has been widening Ukrainian drone and missile strikes against Russian oil and gas facilities. In particular, drone strikes in September on the Astrakhan and Orenburg natural gas plants led to Russian sulphur exports being cut drastically, first from around 400,000 tonnes per month to only 100,000 tonnes in October, and then to zero from the 1st of November, as Russia implemented a ban on exports of sulphur used in fertilizer production which was projected to last at least until December 31st. “This decision will stabilise shipments of raw materials to the domestic market to maintain current mineral fertilizer production volumes and ensure the country’s food security,” the government’s press service reported. The restriction applies to the export of liquid, granulated, and lump sulphur. It remains to be seen whether exports of Kazakh material from Ust Luga will be affected, but some Kazakh sulphur is now being sold via Iran.

While north Africa’s sulphur demand is dominated by its phosphate industry, south of the Sahara it is copper, cobalt and uranium mining, leaching and smelting that hold sway over acid production and demand.

Sulphur prices advanced further in October, more than expected, supported by the supply towards the end of summer becoming restricted, with a number of non-mainstream sources facing logistical constraints.

Singapore-based Indorama Group, through its Senegalese subsidiary Industries Chimiques du Sénégal (ICS), has signed a memorandum of understanding with Senegal’s Investment and Major Projects Promotion Agency (APIX) to launch a major $210 million investment, aiming to boost Senegal’s phosphate and fertilizer production capacity, reinforcing the country’s strategic role in the regional agricultural input market.

Queensland-based SMAC (Strategic:Mi nerals:Acid:Critical) Developments says that it plans to list on the Toronto Stock Exchange in December to raise $1.3 million to fund a final feasibility study. The company is attempting to develop sulphuric acid production in northern Queensland to supply local industries. The company plans to initially build a 180,000 t/a sulphur burning acid plant at a site at Cloncurry, followed by a second phase which would involve developing a pyrite roasting plant to generate 550-600,000 t/a of sulphuric acid.

Travertine Technologies, Inc., has began operations at its demonstration plant in New York state. The core Travertine process demonstrated at this plant combines three major unit operations: salt-splitting electrolysis, caustic direct air capture, and mineralisation. This process produces sulphuric acid, calcium carbonate, and green hydrogen from waste gypsum and carbon dioxide captured directly from the air. The demonstration plant will produce 125 t/a of sulfuric acid, 125 t/a of calcium carbonate, and 55 t/a of carbon dioxide sequestration. The plant will supply sustainable sulphuric acid for local partner Sabin Metal Corporation's precious metals recycling and refining business.

• Russia is set to impose a temporary ban on sulphur exports, covering liquid, granulated, and lump material, to ensure domestic supply. The measure will be in effect until 31 December 2025. CRU expects Russia to return to the export market in 2026 Q1. On the other hand, exports from Iranian ports are set to come back not only for Iranian production but also for Turkmenistan.

At least 43 people were injured after sulphuric acid fumes leaked from a chemical storage at the port of Aqaba in October, according to local press reports. Two of the injured were admitted to intensive care and another six were held in hospital. The remaining cases were described as mild and were treated either on-site or in nearby hospitals. Jordan’s Public Security Directorate (PSD) said emergency teams from the Aqaba Civil Defence Department, supported by the Aqaba Support Group, responded immediately to reports of a sulphuric acid vapour leak which created a fume cloud roughly 400 square metres in size. The operating company’s technical team managed to stop the leak before specialised hazardous materials units from the Civil Defence took over, implementing safety procedures in line with approved protocols. Investigations are under way to determine the cause of the leak, in coordination with the Public Security Directorate and other relevant agencies. Three years ago a sulphuric acid leak from a storage tank at Aqaba killed 13 and injured several hundred people.

Chile’s state-run mining company Enami says that it has received an environmental permit for a new $1.7 billion copper smelter, as part of the modernization of its Hernan Videla Lira smelting facility in the northern Atacama region. The new facility will process up to 850,000 t/a of copper concentrate, and its electrolytic refinery will produce up to 240,000 t/a of copper cathodes for use in electronics, construction and renewable vehicles. Enami says that the modernisation will “ensure profitable and sustainable operations, and practically triple the capacity of the old smelter.”