Price Trends

Meena Chauhan, Head of Sulphur and Sulphuric Acid Research, Argus Media, assesses price trends and the market outlook for sulphur.

Meena Chauhan, Head of Sulphur and Sulphuric Acid Research, Argus Media, assesses price trends and the market outlook for sulphur.

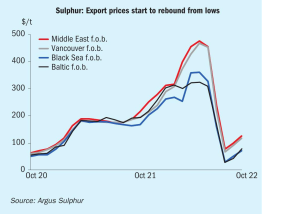

Sulphur markets suffered a correction in July-August that was more of a collapse; from $500/t to less than $100/t. Though it seems to have been something of an over-correction, and prices have moved back up since then, it is one of the most extreme price swings that sulphur has ever seen, comparable to the peak and precipitous fall in 2008. Indeed, at a time when commodity prices of all kinds have seen extremely high levels of volatility, sulphur has been more volatile still than just about all of them.

Market Insight courtesy of Argus Media

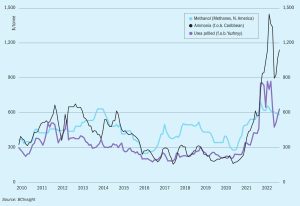

Fertilizers are always political to some extent, sitting as they do at the intersection of key commodities such as oil and gas on the one hand and food on the other. Markets for major nitrogen derivatives have often been distorted by political decisions to achieve self-sufficiency in fertilizer production, such as in, e.g. China or India. But over the past couple of months ammonia has found itself particularly in the political spotlight, in the context of the ongoing conflict in Ukraine, which continues to shape and indeed re-shape global commodity markets.

The ammonia market appears to be oversupplied as of the end of October 2022, with a ready availability of spot cargoes. Coupled with increased availability from European producers due to an easing of gas prices, this seemed to indicate bearish market sentiment for the immediate future.

The curtailment of ammonia production in Europe and reduction in export supply from Russia has led to an unprecedented year for the merchant ammonia market.

Market Insight courtesy of Argus Media

As we near the end of the third quarter of 2022, the attention of the nitrogen industry is focused on the coming northern hemisphere winter, and the prospects for higher natural gas prices as temperatures fall and power and heating demands rise. Vladimir Putin has been stoking these worries to try and force a climbdown from European countries over the sanctions that followed his invasion of Ukraine, with the flow of gas through the Nordstream 1 pipeline across the Baltic Sea gradually dwindling over the summer and finally stopping altogether at the end of August due to “technical issues” – an explanation somewhat undermined by the subsequent statement from spokesman Dmitry Peskov that gas would flow again once sanctions were eased. This is a familiar enough tactic; Russia has used gas stoppages to pressure Ukraine and Europe several times over the past two decades.

Overall the market finds itself in a period of illiquidity, and is exposed to further uncertainty in 4Q because of the European energy crisis. Spiralling natural gas costs in Europe, with Dutch TTF gas prices trading around e200/MWh, are forcing European fertilizer producers to close ammonia capacity and buy in from overseas.

The war in Ukraine has severely affected the supply of ammonium nitrate and CAN from Russia and Ukraine, with particular potential impact on Europe and Latin America. Can urea make up the difference?