Price Trends

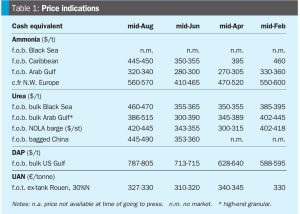

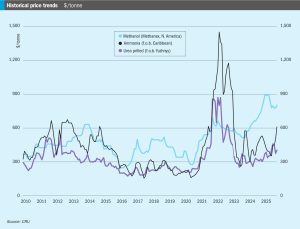

By the end of October the ammonia market was facing an acute shortage of spot tonnage, reflected in a $60/t jump in the Tampa price for November. The benchmark Tampa price increased for the sixth straight month to its highest since February 2023 as the global ammonia supply crunch deepened. The surge at Tampa was said to be driven by good demand in the US for direct application combined with a lack of supply. Contributing factors included Nutrien shutting down its nitrogen production in Trinidad, potentially removing around 85,000 tonnes/month from the market. So far, there is no suggestion that other producers in Trinidad will follow suit, and they may even benefit from a boost natural-gas supply given the Nutrien outage, although it is unclear whether the spare gas will be directed to ammonia as opposed to other demand sources.