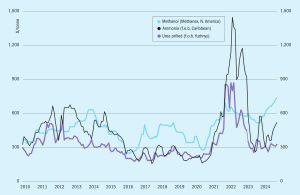

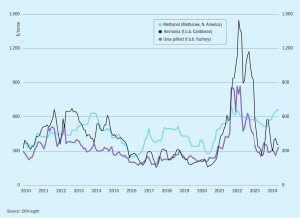

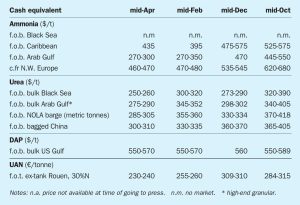

Price Trends

Ammonia markets saw a slow start to 2025, with further transparency needed on both sides of the Suez to determine the extent to which prices are expected to fall through January amid healthy supply and only limited pockets of demand.

Ammonia markets saw a slow start to 2025, with further transparency needed on both sides of the Suez to determine the extent to which prices are expected to fall through January amid healthy supply and only limited pockets of demand.

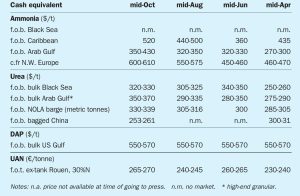

Ammonia prices could remain stable for the duration of October, with any further increases likely to be capped by a lack of demand. The outlook for November is more positive for buyers, with prices set to ease off once turnarounds at key export hubs are concluded.

In October, ammonia benchmarks were more or less stable across the board. West of Suez, supply from Algeria was constrained by an ongoing turnaround at one of domestic player Sorfert’s production units. Still, demand from NW Europe remained quiet, although CF was set to receive a 15,000 tonne spot cargo from Hexagon some time in November, reportedly sourced somewhere in the region of $530/t f.o.b. Turkey. While regional supply appeared tight, steadily improving output from Trinidad and the US Gulf could alleviate recent pressures, with many players of the opinion that Yara and Mosaic could agree a $560/t c.fr rollover for November at Tampa as a result.

In China, domestic prices are expected to come under significant downward pressure, with seaborne indications already following suit, with buyers said to have rejected offers around the $375/t c.fr mark.

Ammonia benchmarks west of Suez remain supported by limited availability at key regional export hubs amid increased potential for cargoes to arrive from the East, where availability is far healthier, and prices appear under pressure. The disparity in prices was illustrated towards the end of August, when Nutrien sold 25,000 tonnes to multiple buyers in NW Europe for 1H September delivery at $550-555/t c.fr. When netted back to Trinidad, the price marks a sizeable premium on the $375/t f.o.b. last achieved by Nutrien back in late June, although given that last business in Algeria was fixed at $520/t f.o.b., it appears there is room for delivered sales into Europe to move up further. Regional availability is still limited, with extreme weather conditions in the US Gulf and North Africa potentially impacting supply further over the coming weeks.

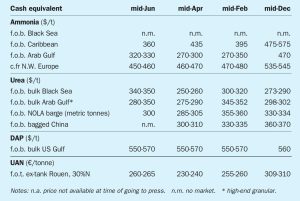

Ammonia markets were quiet in June, though both CF Industries and Grupa Azoty were reported to be looking for July tonnes and the enquiry will test how tight the market is going forward. Algeria has traded in the $400-405/t f.o.b. range, suggesting c.fr values in Europe might be slightly higher at $450-460/t c.fr. Supply from Algeria has been and continues to be somewhat restricted because of constraints caused by the hot weather. Gas supply however is easing in Egypt and further ammonia exports should emerge shortly.

Prices in the Eastern Hemisphere, whilst still flat-to-firm, do not appear as supported as they have been over the past month, whilst indexes. There are still no signs of softening in the Far East although demand remains underwhelming and supply improving. While production in Indonesia is said to be back up and running, traders do not expect any spot cargo to emerge in July other than possibly some small part cargoes. August could see spot offers.

The ammonia market reverted to recent norms at the end of April, with prices more or less unchanged in the east, and several benchmarks west of Suez moving downward in line with May’s Tampa settlement. Following a trio of high-priced c.fr spot deals many wondered whether such business would be replicated in Asia, but the hype did not live up to the expectation, with the majority of tonnes continuing to move on a contract basis into the likes of South Korea and Taiwan, China. The $430/t c.fr concluded into China has been attributed to both supply uncertainty and an uptick in domestic demand, though several inland prices declined this week, rendering price direction difficult.

Prices in the West are unlikely to garner much support moving into the latter stages of Q2. The May Tampa ammonia settlement was settled by Yara and Mosaic at $450/t c.fr, down $25/t on the $475/t c.fr agreed for April. With seasonal domestic demand in the US drawing to a close 2H April, many had anticipated that either a rollover or a slight decline would be agreed.

Ammonia pricing in the US Mid-West stood at $625/st f.o.b. in February, with applications to field continuing to ramp up. Prices in the US Gulf remain pegged in the low-to-mid$400s/t f.o.b. Recent production outages in the region have largely subsided, though an unexpectedly early uptick in seasonal demand from local buyers is likely to provide a degree of price support moving forward. The Tampa ammonia settlement for March has been settled by Yara and Mosaic at a $445/t c.fr rollover, largely in line with market expectations. The North American market remains detached from the considerably more oversupplied global ammonia scene.