Market Outlook

• Ammonia prices look well insulated against any declines over the immediate term, though the upside may be more limited in some regions than others.

• Ammonia prices look well insulated against any declines over the immediate term, though the upside may be more limited in some regions than others.

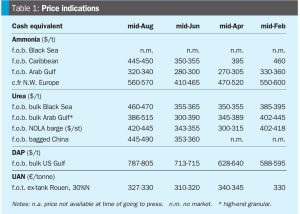

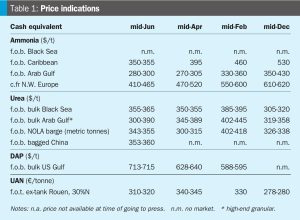

Ammonia prices in both hemispheres had levelled out by the end of August, with the exception of a few marginal upticks in some regions on the basis of the latest supply-demand dynamics. All eyes are now on September’s Tampa settlement, which should spell out the extent of the upside pressure set to emerge over the coming weeks.

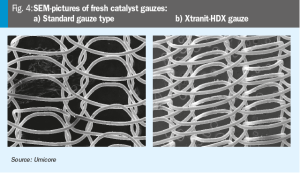

Umicore’s latest research and development has resulted in a novel catalyst for the Ostwald process, aiming to enhance efficiency and sustainability in high-pressure nitric acid production.

Stamicarbon has optimised urea granulation to meet rising global fertilizer demands by improving product robustness, reducing capital and operating costs through a simplified design.

Casale’s high-performance finishing technologies combine flexibility and innovation with seamless integration and sustainability across the nitrogen fertilizer value chain. Gabriele Marcon and Ken Monstrey of Casale present the latest developments in Casale’s comprehensive portfolio of fertilizer finishing technologies and highlight recent projects.

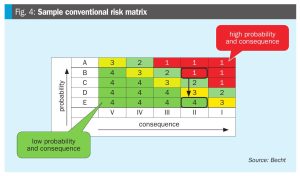

Becht’s Risk Based Work Selection (RBWS) process is a structured, data-driven method that uses risk and benefit-to-cost analysis to optimise turnaround and maintenance work in industrial facilities, resulting in significant cost savings and improved reliability.

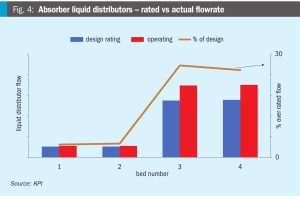

KPI describes the systematic revamp of a Benfield CO2 removal unit at a high-throughput ammonia plant, emphasising simulation-driven diagnostics and customised engineering solutions.

A round-up of current and proposed projects involving non-nitrogen synthesis gas derivatives, including methanol, synthetic/substitute natural gas (SNG) and gas- and coal to liquids (GTL/CTL) plants.

Ammonia benchmarks on both sides of the Suez were little changed in mid-June with a seemingly balanced supply-demand outlook, although those of a more bullish persuasion continue to support the notion that prices will soon – if they have not done so already – reach a floor. In Algeria, while activity was limited, producer Sorfert was believed to be seeking prices of $410415/t f.o.b. for July delivery, up $10-15/t and equivalent to >$450/t c.fr NW Europe. Imminent tariffs on imports of Russian fertilizers into the EU may trigger an uptick in downstream capacity utilisation across the continent.

• The short term outlook appears balanced for the most part, although more bullish participants seem to be holding sway over market sentiment.