Nitrogen+Syngas 400 Mar-Apr 2026

17 March 2026

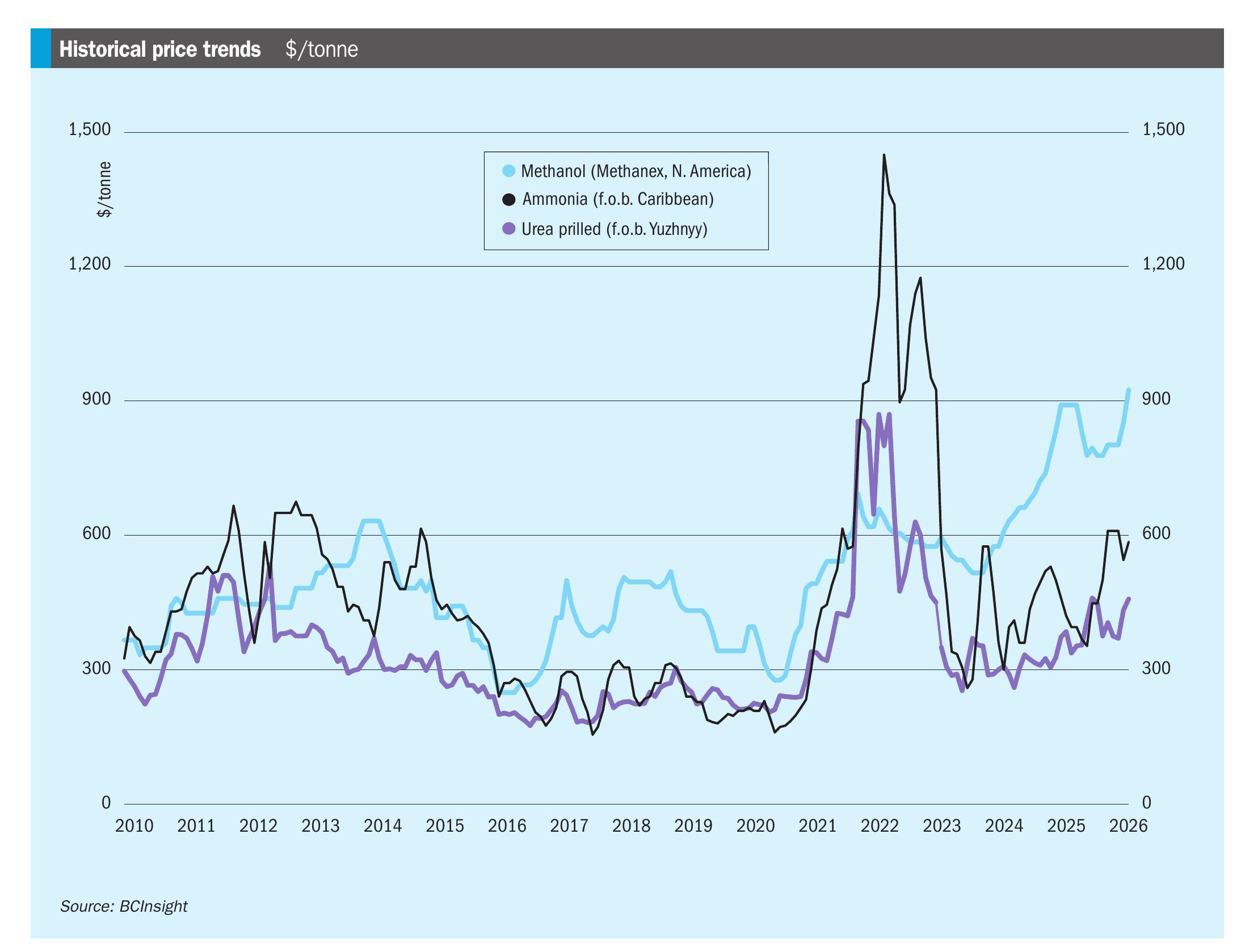

Another price shock

“Urea prices have jumped, in some cases by a reported $200/t…”

In just its first two months, 2026 had already managed to be a rollercoaster of a year, but at the start of March, the onset of hostilities against Iran by the US and Israel has managed to deliver another huge shock to markets, particularly commodities. Iran’s strategy of widening the conflict to neighbouring states, including by attacking Qatar’s massive LNG facility at Ras Laffan, effectively shutting it down, has sent the LNG market into chaos, and attacks on several tankers and other ships have paralysed maritime insurance markets and by default achieved the long-feared closure of the Straits of Hormuz.

At time of writing the conflict is less than two weeks old, but already oil prices have risen 35% to $90/bbl, after peaking at $120/bbl. All Gulf exports have halted, and Saudi Arabia is only able to export 5 million barrels per day via the Red Sea. Natural gas prices here in the UK have virtually doubled, as LNG cargoes are diverted away from Europe towards Asia by rising prices. Dutch TTF prices were last reported at $15/MMBtu, with some relief in Europe provided by warmer spring weather. Urea prices have jumped, in some cases by a reported $200/t, as the Straits carry almost one third of all traded product, and Iran has been a major exporter, particularly to India and China. India has invoked emergency measures to cut natural gas supplies to its fertilizer industry, forcing the sector to operate at approximately 70% of recent capacity, removing millions more tonnes from the market. Overall, around 47% of global sulphur, 43% of urea, 27% of ammonia and 24% of phosphate fertilizer trade is judged to be ‘at risk’.

For nitrogen markets, the shutdown of Qatar’s 5.6 million t/a urea complex at Mesaieed has been the first confirmed fertilizer production impact in the region. Most other sites are currently understood to be operating normally, but could mirror Qatar’s approach if the conflict persists. Duration is the key variable: CRU expects the two-week point to be pivotal for operational continuity. If disruption extends beyond two weeks, the main risk shifts to broader supply interruptions driven by constrained export routes, limited domestic offtake, and inadequate storage. With an additional two weeks potentially needed to restart idled capacity, this would imply a meaningful reduction in Middle East supply availability for March, alongside higher costs from repeated shutdown/restart cycling.

At present, CRU’s central assumption is that major shipping disruption will persist for at least three weeks, with significant ramifications for fertilizer importing markets heading into the spring planting season. By the end of week three of the conflict, the economic consequences may become crippling and may force a declaration of ‘victory’ or at least some form of agreement that allows some traffic through Hormuz to resume. Even so, while he has shown some signs of concern at rising oil prices feeding through to the gasoline pump in the US, president Trump has also said that the campaign may extend to five weeks or longer. For its part, the election of Mojtaba Khamenei as Ayatollah is a signal by Iran that it is in no mood for concessions, and the Islamic Revolutionary Guard Corps (IRGC) has said that it will determine when the war ends, not the US.