Fertilizer International 526 May-Jun 2025

2 May 2025

Serra do Salitre ramps up

CRU INSIGHT

Serra do Salitre ramps up

Following the 2025 Fertilizer Latino Americano Conference in Rio de Janeiro, CRU’s Humphrey Knight visited EuroChem’s newly opened Serra do Salitre phosphate fertilizer complex in southern Brazil. Interest has centred on EuroChem’s ability to produce monoammonium phosphate (MAP) at the complex, given that Brazil is heavily reliant on global import supplies. However, domestic demand and pricing incentives ultimately mean that Serra do Salitre will principally focus on single superphosphate (SSP) production for now.

Producing after protracted development

Initially developed by Brazilian producer Galvani, Yara International acquired 100% of the shares in Serra do Salitre in October 2018 to take complete control of the project. Yara’s tenure as owner proved short-lived, however, despite the project having successfully commenced phosphate rock production that same year.

The Norwegian fertilizer major sold on Serra do Salitre less than three years later to Russian producer EuroChem in 2021 for $452 million (Fertilizer International 507, p58). EuroChem then finished construction and commenced fertilizer production at the complex in mid-2024, having invested a figure close to $452 million to complete the project.

Production continues to ramp-up with EuroChem expecting Serra do Salitre to reach the following planned capacities by the end of 2025:

- 1.2 million t/a phosphate rock concentrate – from around 10 million t/a of phosphate ore

- 1.0 million t/a granular phosphate fertilizers – split between single superphosphate (SSP), triple superphosphate (TSP), monoammonium phosphate (MAP) and NP/NPK

- 0.25 million t/a P2O5 wet phosphoric acid (WPA)

- 1.0 million t/a sulphuric acid.

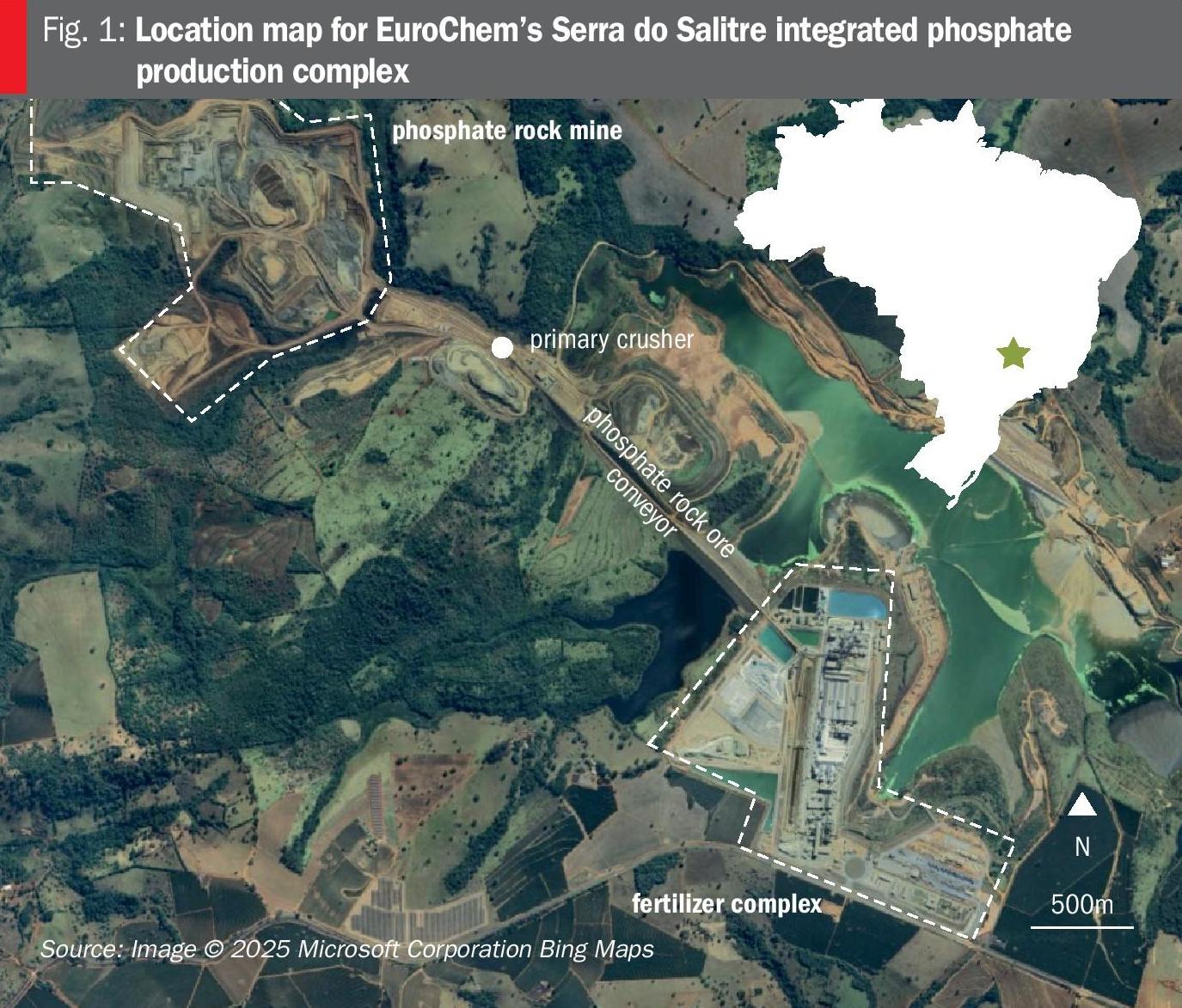

Serra do Salitre is located in Minas Gerais state (Figure 1). The phosphate rock mine – located adjacent to Mosaic Fertilizantes’ Patrocinio property – extracts highly weathered, friable igneous ‘bebedourite’ ore (3-5% P2O5) using excavators without the need for drill and blast techniques. Ore is moved by 30 tonne trucks to a primary crusher and then conveyed around two kilometres to the run-of-mine storage at the fertilizer complex in readiness for beneficiation. Froth flotation of a conditioned pulp yields a wet phosphate rock concentrate of 30–34% P2O5, split into coarse and fine fractions.

The fine concentrate is used to produce SSP, while the coarse fraction is largely used in wet phosphoric acid (WPA) production, although a portion of the coarse fraction is also separated and dried. Subsequently, the WPA obtained is either: l Reacted with ammonia and then granulated to yield MAP and NPs or l Reacted with the dry coarse phosphate rock concentrate to make TSP.

Although it has yet do so, Serra do Salitre also has the ability to make NPKs by incorporating standard-grade muriate of potash (MOP) with an on-site blending and bagging unit.

Imported sulphur feedstock is burned on site in the sulphuric acid plant – with co-generation at this plant supplying around 40% of power requirements at the complex. EuroChem also has the option to trade any excess sulphuric acid generated. The site’s ammonia requirements, meanwhile, are supplied by Yara from its Cubatao plant near Sao Paulo. All raw materials (other than phosphate rock) arrive and all finished products leave Serra do Salitre via trucks.

Brazil’s phosphate industry dominated by SSP

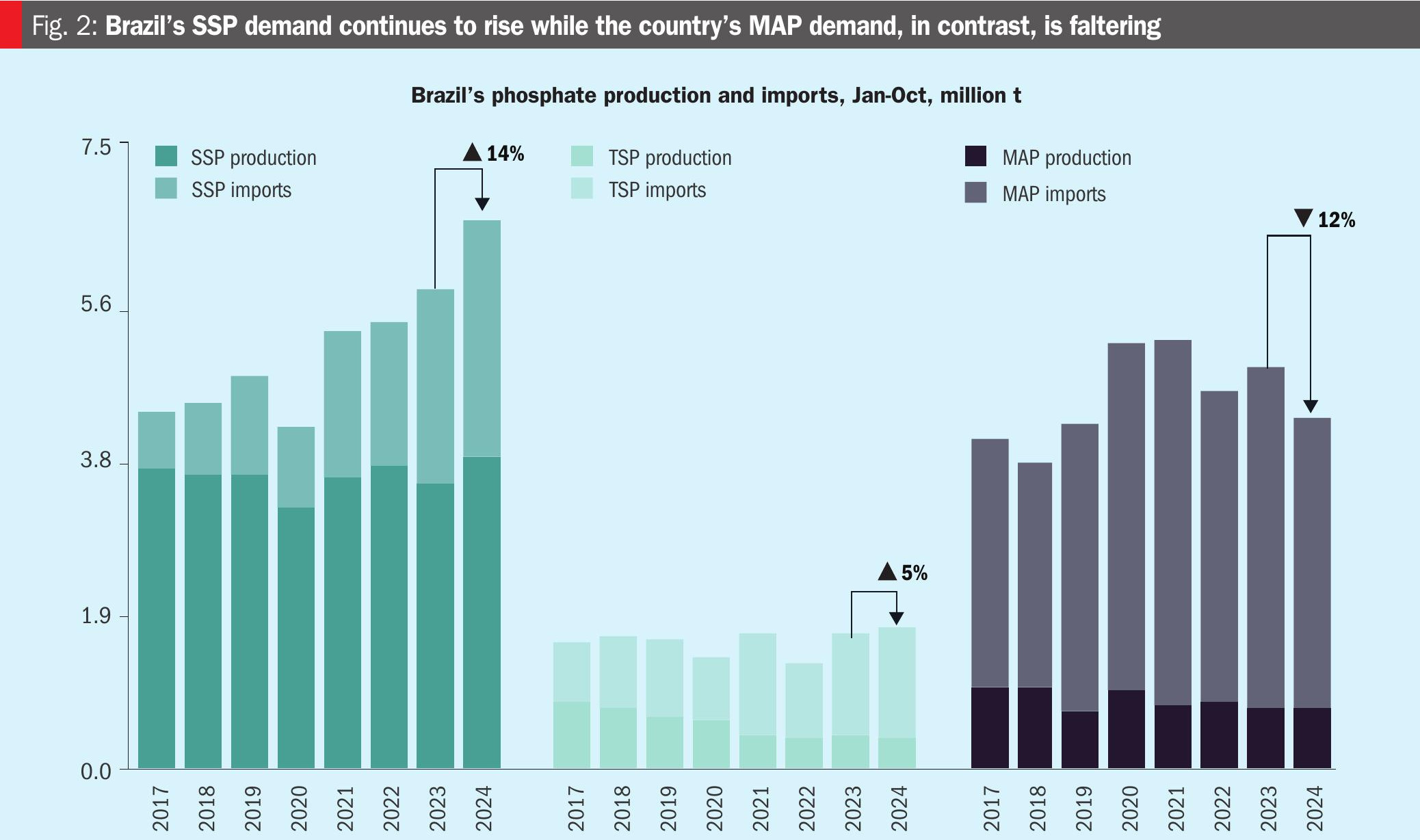

Towards the end of the 2010s, Brazil’s consumption of SSP and MAP stood at similar levels, around 4–6 million t/a each. The key difference was that agricultural consumers sourced the vast majority of their SSP requirements from domestic producers, whereas MAP consumption relied primarily on imported supply.

Since 2020, while the domestic supply of both MAP and SSP has remained reasonably steady – with supply of the former declining somewhat during the past decade – the supply and consumption of SPP from imported sources has risen sharply (Figure 2, left). A similar rise in TSP imports has also offset lower domestic production (Figure 2, middle).

Brazil has, however, struggled to maintain MAP import levels during the tighter trade and higher price conditions that are currently prevailing (Figure 2, right). This has made sourcing sufficient MAP to satisfy demand a challenge, as the country’s domestic MAP production is not large enough to make up any shortfalls.

While Serra do Salitre has the capability to produce MAP – with production already taking place – output is unlikely to exceed 0.2 million t/a, even when the site ramps up to full capacity.

This is partly due to production limits imposed by the modest WPA capacity (0.25 million t/a P2O5) at the complex – and EuroChem’s need to produce NPs and TSP from WPA as well as MAP. Consequently, while the top up in MAP output from this new production complex may stabilise Brazil’s total domestic production, it will do little to offset the country’s major import requirement for MAP or alleviate the current supply tightness, in our view.

Instead, phosphate fertilizer production at Serra do Salitre will focus on SSP, with output of around 0.5 million tonnes expected in 2025, as Brazil’s domestic producers still have a commercial incentive to make SSP, despite persistently high MAP prices.

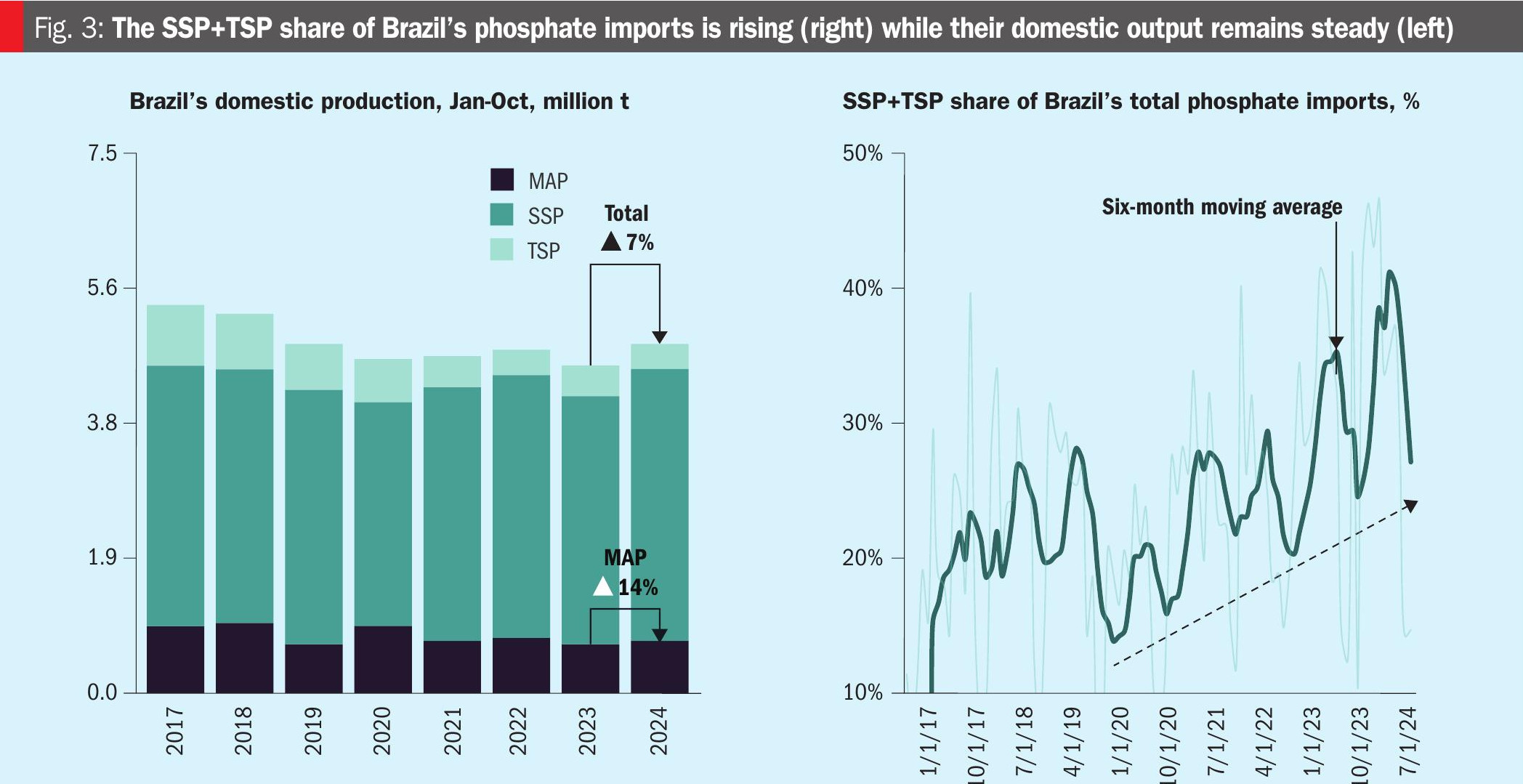

From a demand perspective, SSP is by far Brazil’s most popular phosphate fertilizer product. Bucking the general trend, the country’s agronomic requirements for sulphur have maintained buying interest in SSP, whereas in most other parts of the world this product has been largely displaced by ammoniated phosphates such as MAP and DAP.

Indeed, SSP imports have grown rapidly since the late 2010s (Figure 3). January-October import volumes, for example, have essentially trebled since 2017, surpassing 2.8 million tonnes in 2024. Brazil’s phosphate fertilizer imports have undoubtedly seen a swing towards superphosphates during the 2020s, as consumers have responded to persistently high MAP prices and faced continued difficulties securing product.

Note: Total phosphate imports include DAP, MAP, NPK, NP(S), SSP and TSP

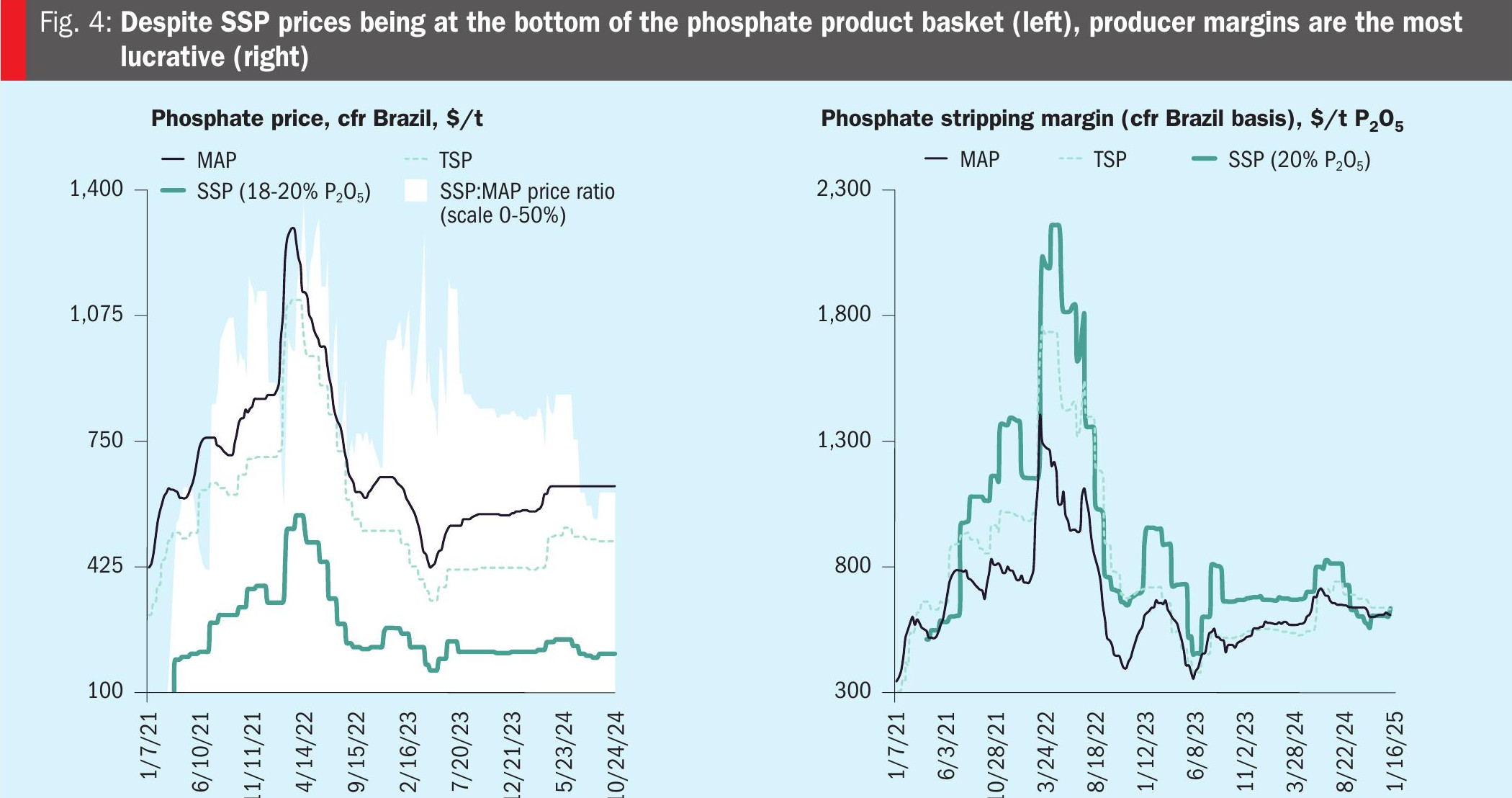

SSP production is also generally the most lucrative option for a domestic Brazilian phosphate manufacturer from a revenue perspective (Figure 4). Even though SSP prices have been hovering at around one third the level of MAP prices since 2021, the avoidance of phosphoric acid production and ammonia consumption significantly reduces production and raw material costs.

High global sulphur prices have brought MAP and SSP producer margins close to parity in recent months. But this is the exception rather than the norm. Since the start of 2023, CRU estimates that a Brazilian domestic phosphate producer on average would have secured an additional $130/t P2O5 on SSP sales compared to MAP (assuming ex-works rock production costs of around $90 /t).

Note: Stripping margins calculated as MAP/TSP/SSP price, less ammonia (f.o.b. Caribbean as a proxy) and sulphur (cfr Brazil) prices and phosphate rock costs (ex-works) at Serra do Salitre.

Clear incentives for SSP production

In conclusion, Brazilian distributors have found it increasingly difficult to secure MAP imports in the 2020s, while consumer demand for MAP has also faltered because of persistently poor affordability. SSP consumption, in contrast, has continued to rise in Brazil, supported in large part by rapid growth in import supplies.

Significantly lower production costs and raw materials exposure also favours domestic SSP production, as this typically generates higher sales margins for Brazilian producers. This is despite SSP prices in Brazil languishing at around one third those of MAP for much of the past four years.

When it comes to displacing Brazil’s now substantial SSP imports, new domestic producers such as EuroChem face significantly less competition from incumbent domestic suppliers than was the case a decade ago. The economic incentives also remain compelling, with SSP returning wider margins (per tonne of P2O5) for most of the time, versus MAP or TSP. Consequently, EuroChem’s rationale for focusing on SSP output as the preferred production pathway at Serra do Salitre is crystal clear – at least in the near term.

About the author

Humphrey Knight is Principal Analyst, Phosphate & Potash

Email: humphrey.knight@crugroup.com

Tel: +44 20 7903 2191