Nitrogen+Syngas 374 Nov-Dec 2021

30 November 2021

Barriers to trade

MARKETS

Barriers to trade

With globalisation seemingly in retreat, the protectionist impulse is seeing a rise in barriers to trade, from quotas and tariffs to anti-dumping actions and domestic subsidies.

Since the Second World War, and especially over the past three decades, the global trade of goods rapidly increased. Over the past century and a half, periods of expansion of international trade have alternated with periods of retrenchment and protectionism. The first great boom in global trade came during the late 19th century with the rapid industrialisation of Europe and North America and the growth of rail and steamship transport, as well as the expansion of colonial control over regions such as Africa and Asia, but ended with the terrible carnage of the First World War. Depression, protectionism and the Second World War saw global trade as a proportion of GDP fall to just 5%. However, economic integration rebounded after the Second World War and continued to increase for the latter half of the 20th century. An embrace of economic liberalisation saw the removal of trade barriers in large emerging markets and led to unprecedented levels of international economic cooperation, with the global trade: GDP ratio peaking in 2008 at 61%.

Since this era of peak globalisation, however, the fallout from the world financial crisis has accompanied increasing tensions over trade, particularly between China and the US, and an increase in global trade barriers, exacerbated over the past two years by the Covid pandemic. Global trade: GDP ratios have fallen to 53.5% in 2017, though rebounding to 58% in 2019, according to World Bank figures (Figure 1).

Barriers to trade

Barriers to international trade can be summed up as falling into one of three categories. The first is what might be termed ‘natural’ barriers – long distances, poor infrastructure such as roads, rail or bottlenecks at ports, linguistic or cultural barriers, or comparative advantage that makes domestic products cheaper to produce than imported products.

The second broad category are financial barriers, specifically tariffs or subsidies. The purpose of tariffs or subsidies is usually to try and advantage less competitive domestic producers against competition from overseas producers by adding to the price of imports. Industries can be protected for a variety of reasons, from attempting to increase competition by letting domestic champions emerge, maintaining employment, especially in vulnerable communities such as rural areas, and other attempts to maintain domestic self-sufficiency for strategic reasons, and increasingly these days for reasons of health, welfare or the environment.

Finally, there are non-tariff barriers which seek to restrict trade, such as import quotas or embargoes – the latter again usually for geopolitical and/or strategic reasons. Other non-tariff barriers can e.g., mandate purchasing rules for domestic consumers, or setting standards which can only be met easily by domestic producers.

The WTO

The rapid expansion of international trade in the post-war period has been driven by the development of a rules-based international trading system, beginning with the General Agreement on Tariffs and Trade (GATT) just after the war, which eventually became the World Trade Organisation (WTO) in 1995. Agriculture was actually a relative latecomer to the WTO system, as domestic food security and the fate of rural communities is often a highly politically-charged area in many countries, and markets were therefore protected through tariffs, quotas, or outright bans on imports. Domestic support to agriculture, particularly among rich developed countries such as the US, Japan, and the EU, was large and growing.

“Agricultural subsidies… continue to distort global trade.”

However, the success of the 1986-1993 Uruguay Round discussions eventually produced the global Agreement on Agriculture (AoA), which brought clarity to areas such as market access, domestic support, and export competition. Under the agreement, members agreed to abolish non-tariff barriers and instead convert them to tariff equivalents, a process call ‘tariffication’ and, where necessary, guarantee minimum access to domestic markets via tariff-rate quotas (TRQs). Developed countries were required to cut tariffs by an average of 36% over six years, and developing countries 24% over 10 years. Several developing countries also used the option of offering tariff ceilings. Export subsidies were capped and reduced, and at Nairobi in 2015, WTO members further agreed that developed countries would immediately remove export subsidies except for on a handful of products, and that developing countries would do so by 2018. Domestic support levels were also subject to reduction commitments and countries were encouraged to adopt support policies that had minimal production- and trade-distorting effects and that were exempt from reduction commitments (so-called ‘green box’ policies).

The result has been a tripling in global agricultural exports by value (doubling by volume) from 1995-2018, reaching $1.8 trillion that year. However, progress since the Uruguay Round has been limited. The Doha Development Agenda (DDA) was launched in 2001, but members failed to reach agreement in 2008 and the trade agenda in Geneva has since advanced slowly. Just this year, in July, the WTO’s director-general Ngozi Okonjo-Iweala used a speech at a meeting with World Bank president David Malpass to argue that agricultural subsidies, especially those in rich countries, continue to distort global trade and create unfair competition for farmers in poor countries. The UN estimates that global support to farm producers totals $540 million per year, and could triple to $1.8 trillion by 2030. Malpass used the same occasion to reference fertilizer subsidies in particular, saying that they can distort which crops are grown as well as encouraging overapplication, leading to eutrophication. The remarks were seen as a steer ahead of the 12th ministerial meeting of the WTO members in Geneva, which will be held from November 30th to December 4th this year, postponed from last year because of the covid pandemic.

The ‘appellate crisis’

One of the key issues for the WTO at the moment is its dispute settlement mechanism, which has also covered agriculture since the completion of the Uruguay Round. When two WTO members have a dispute over the legality of any trade measure, they can refer the case to the WTO’s Dispute Settlement Body, comprising all member states, which then establishes a dispute panel which can arbitrate on the case. However, if one party is unsatisfied with the resolution, it can refer the case to the WTO Appellate Body, which functions as a final court of appeal. However, two of the members of the 7-person Appellate Body completed their terms in 2019, and the US has been blocking new appointments to it over a series of grievances with the WTO, including questions of delay, judicial over-reach, precedence, and transition rules. While the move was instigated by the Trump administration, this is an area where the Biden administration has continued the same policy, and it stems in no small part from ongoing rivalries with China. In the interim, the Appellate Body is unable to hear new appeals.

To find a temporary solution to the impasse, the EU and China and a number of other member states have set up a multiparty interim appeal arbitration arrangement (MPIA). The parties continue to seek resolution of the Appellate Body crisis, and agree to use the MPIA as a second instance as long as the situation continues. However, unless the matter can be resolved, the WTO may actually face an existential crisis.

China

Though it is some way down the list compared to disputes over e.g. steel and aluminium, fertilizer has also actually been one of the sticking points between the US and China. China acceded to the WTO in 2002, and in its accession agreement China agreed to implement a system of tariff rate quotas (TRQs) designed to provide significant market access for key industrial products, including phosphate fertilizer, a major US export. Under the TRQ system, a set quantity of imports is allowed at a low tariff rate, while imports above that level are subject to a higher tariff rate. The quantity of imports allowed at the low tariff rate increases annually by an agreed amount. However, the US has expressed concerns about Chinese government policies promoting domestic fertilizer production, including export duties and the exemption of diammonium phosphate from 13% VAT.

India

India acceded to the WTO in 1995 and was a member of GATT from 1948 onwards. However, it has faced criticism for its subsidy policy on domestic fertilizer production. India gave $22.5 billion as agricultural input subsidies in the 2017-18 financial year, including support for irrigation, fertilizers and electricity. However, in response, India points out that its agriculstural census of 2016 showed that 99.4% of all farm holdings in the country were low-income or resource poor farmers, and that in consequence the country will not accept any limits on subsidies on farm inputs such as seeds and fertilizers.

There is also a sense of injustice in that – unlike some of the richer countries such as the EU, US and Canada – countries such as India and China do not have access to permitted Aggregate Measurement of Support (AMS) measures, which are supposed to be slowly capped, reduced and eliminated. India and China say that AMS measures, such as the EU’s Common Agricultural Policy, currently provide $160 billion in subsidies to developed world farmers every year. India says that were it allowed to draw down subsidy in the same way as AMS measures, its subsidies are well below permitted levels.

Russia

Russia did not accede to the WTO until 2012. Prior to that, the European Union and United States had long argued that Russian fertilizer producers benefitted from artificially low natural gas prices, leading to so-called “dumping” of cheap product on western markets at below what should be a ‘natural’ cost price, and in return imposed a series of anti-dumping tariffs against Russian ammonium nitrate and other products during the 1990s and 2000s, amounting to around $32/tonne as per its last revision. However, the Russian gas industry has changed considerably since the collapse of the Soviet Union in 1989, and there is much more competition and market-related pricing in the industry now. Indeed, Russia has actually found itself benefitting from WTO adjudications recently, with a case brought last year in the WTO which ruled that existing EU anti-dumping duties on Russian AN were illegal and should be removed, as they used an outdated methodology for deciding what a “fair” price for gas inputs should be. However, the EU and UK both reaffirmed their anti-dumping duties in December 2020 following a review. India also maintains anti-dumping duties on Russian AN, although it is a much smaller consumer of it than the EU.

European Union

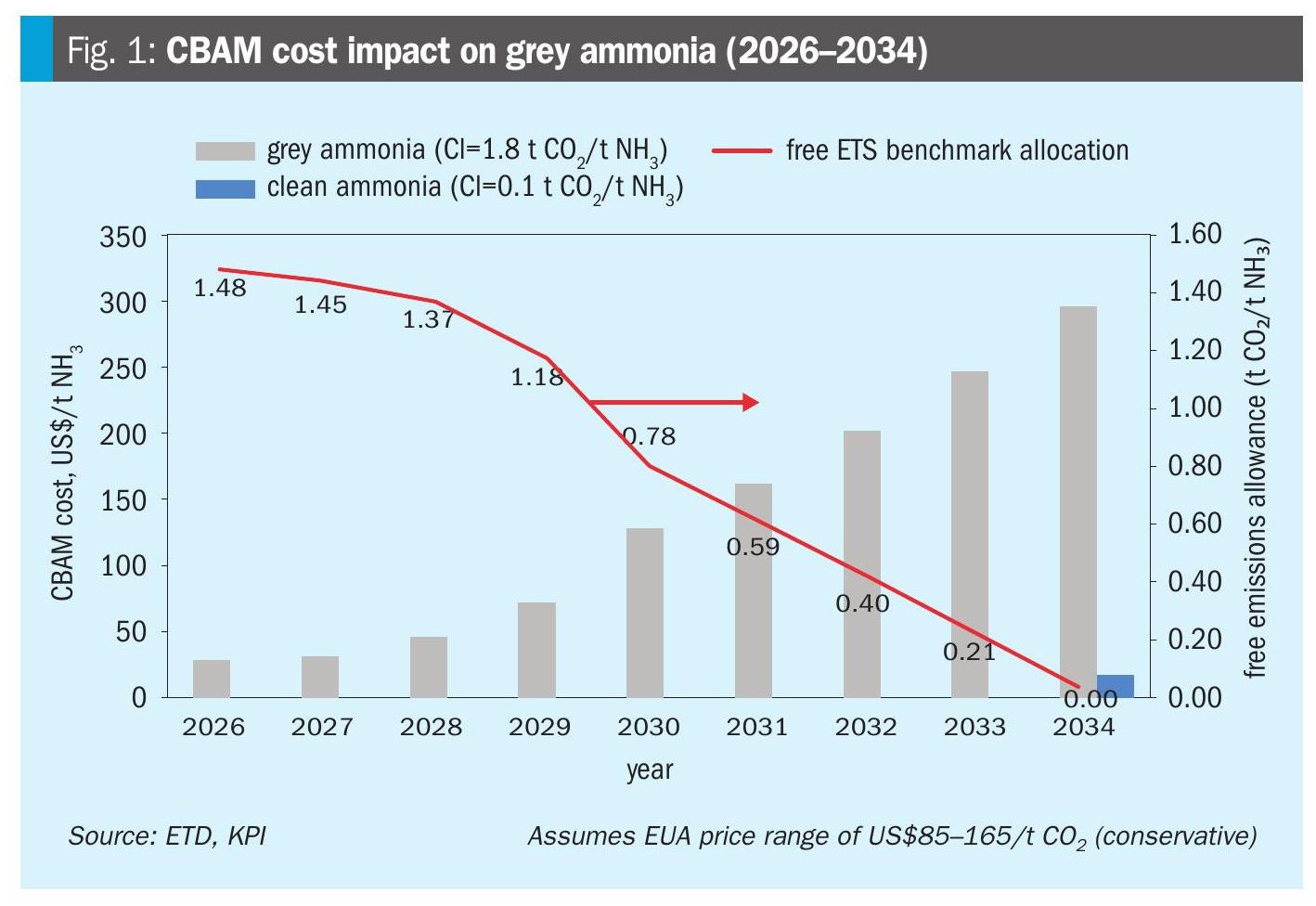

In addition to criticisms over its Common Agricultural Policy, there is a suspicion in some quarters that the EU is also beginning to use environmental measures to privilege its domestic industry. In December 2019, the EU proposed to introduce a carbon border adjustment mechanism (CBAM), a form of carbon pricing on imports into the EU, as part of the European Green Deal. The rationale behind the initiative is an attempt to address the risk that the EU’s efforts to curb greenhouse gas (GHG) emissions will be undermined by a lack of climate ambition in non-EU countries due to so-called “carbon leakage” – a situation when stronger climate policies in one jurisdiction lead to increased GHG emissions in other jurisdictions. It will target listed products from six carbon-intensive sectors, and nitrogen fertilizer production is one of those. The EU has talked of implementing the CBAM by 2026.

The CBAM was the subject of discussion at the WTO Committee on Trade and Environment (CTE), in March this year, and a number of members stressed that it needs to be designed in a transparent way, and different levels of development should be considered to address trade distortions. However, the EU says that under the proposal, countries with their own emissions trading systems such as Norway and Iceland could gain levels of exemption from CBAM, and the UK and China may also qualify if they link their national trading schemes to the EU ETS. The measure could spark greater interest in emissions trading schemes more generally. Canada and Japan, and possibly even the US are also said to be considering similar carbon border taxes. Much may depend upon what emerges from the COP-26 talks in Glasgow this autumn.

Africa

Africa remains the only continent not to have profited from a ‘green revolution’ in fertilizer use and food production in the same way that South America and Asia did from the 1970s onwards. In 2006 a meeting of the African Union made the Abuja Declaration, which called for 6% annual growth in agricultural production as a framework for the restoration of agricultural growth, food security and rural development in Africa. One of the concrete measures to be adopted was harmonisation of policies and regulations to ensure duty- and tax-free movement across regions, and the elimination of taxes and tariffs on fertilizer and on fertilizer raw materials.

Fifteen years on, progress remains very slow on achieving these goals. Standards and regulations, and non-tariff barriers (NTBs) continue to be a major bottleneck to trade and consumption of fertilizers, though these barriers can include poor infrastructure for transport and distribution. Urea production in Nigeria increased from less than 1 million t/a in 2015 to over 4 million t/a in 2018; sufficient to satisfy most of the demand for fertilizer in the rest of sub-Saharan Africa. However, as a result of prevailing local tariff and non-tariff barriers, over 80% of Nigeria’s urea is exported to Brazil and Argentina.

However, the African Continental Free Trade Area (AfCFTA), which came into operation in January 2021 under the auspices of the African Union, and currently ratified by 38 countries, may be a step to tackle this at last. It requires members to remove tariffs between member states on 90% of goods, and could boost inter-African trade by more than 50% within a couple of years.

Feeding the world

The growth in global trade has impacted many areas, and agricultural trade has been no exception, with the value of world trade in agricultural products having now increased to around $1.8 trillion per year. However, the UN Food and Agricultural Organisation (FAO) projects that global food demand will increase by as much as 50% from 2012-2013 levels by 2050, as trends in population growth, urbanisation, and income growth continue, particularly in developing countries. Population projections by the United Nations suggest that 98% of the population growth expected between 2015 and 2050 will come from developing countries, with sub-Saharan Africa accounting for more than 55% of that growth. Income growth rates and urbanisation rates are also projected to be higher in developing countries, so that much of the global demand growth for meats, dairy, fruits and vegetables, and processed food products will continue to come from these economies. This could also be true for fertilizer demand growth, perhaps balancing losses from more efficient use elsewhere, but it will require the continued lowering of tariff and non-tariff barriers to trade. However, as this article has discussed, in order to achieve this there are a number of issues outstanding, from the Appellate Crisis to Aggregate Measurement of Support calculations and the impact of cross-border carbon taxes which need to be urgently addressed.