Market Outlook

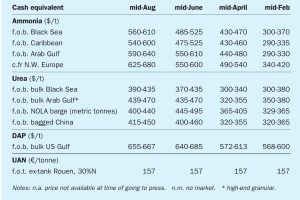

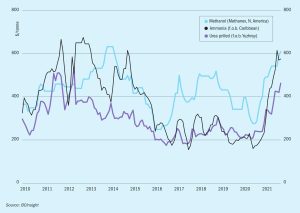

Soaring natural gas prices in Europe, up to five times higher than normal, have led to numerous economic shutdowns of ammonia capacity across the continent. This has coincided with shutdowns in the US due to hurricane season, reducing availability considerably and driving up prices in the western hemisphere.