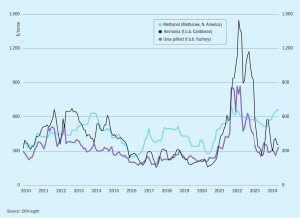

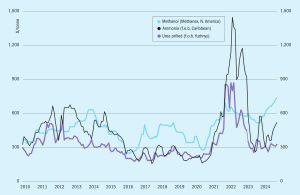

Market Outlook

Ammonia prices could remain stable for the duration of October, with any further increases likely to be capped by a lack of demand. The outlook for November is more positive for buyers, with prices set to ease off once turnarounds at key export hubs are concluded.