Market Insight

Price trends and the market outlook, 19th June 2025

Price trends and the market outlook, 19th June 2025

President Donald Trump delayed his ‘liberation day” tariffs by three months on 9th April, while simultaneously ramping up levies on China.

Price trends and the market outlook, 10th April 2025

It is with great sadness that we report the death of Dr. Umberto Zardi, who passed away on March 17th 2025 at his home in Breganzona, Lugano, Switzerland. Dr Zardi was an innovator in the nitrogen industry and for many years the president and driving force behind Ammonia Casale, now simply Casale SA, becoming responsible for its revival and transformation into the global engineering and technology giant that it is today.

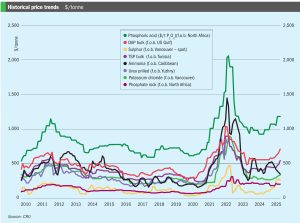

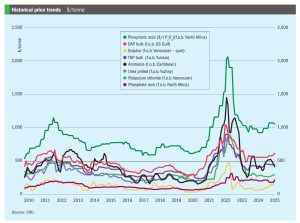

• Continuing oversupply means that ammonia prices should continue to come under pressure moving into 2H April, though it remains to be seen just how much further values in Asia can decline before producers begin to shutter output.

Spanish company Ignis has decided to pause work on the renewable energy generation projects it had planned in Chile’s Magallanes region. In a press statement, Ignis said that: “even though we firmly believe that this industry will develop and mature, the company is considering a longer time frame than initially planned and a reduction in the project to adapt it to this new reality.” The company was developing a wind farm to supply the green ammonia plant with hydrogen, but reportedly found the process of leasing the land area to build the turbines slower and more difficult than it had hoped.

Achema says that it plans to “temporarily” suspend ammonia production at its site at Jonava from May 15th, due to the volatility of natural gas prices and competition from cheaper foreign imports. It currently plans to resume production in 3Q 2025. The facility has been operating at reduced capacity since 2021, and Lithuanian lawmakers have discussed converting the site to explosive grade ammonium nitrate production as part of a European rearmament programme.

In mid-April, Ammonia prices both east and west of Suez remained firmly oriented to the downside, with supply still heavily outweighing demand and suppliers scrambling to place excess tonnage. Bearish market sentiment was exemplified by a Trammo sale to OCP at $415/t c.fr Morocco, $20/t short of Tampa’s c.fr settlement for April and around $44/t down on February.

Alfa Laval says that its ammonia fuel supply system, FCM Ammonia, will be installed in seven LPG/ammonia carriers for Tianjin Southwest Maritime (TSM). The installation will commence with three 25,000m3 vessels, followed by four 41,000m3 vessels. The first FCM Ammonia unit for TSM is scheduled for delivery at the end of 2025. The contract follows extensive testing and development conducted in close collaboration with Swiss engine designer WinGD at its Engine & Research Innovation Centre (ERIC) in Winterthur, Switzerland. Alfa Laval says that the research and development project with WinGD has laid a strong foundation for FCM Ammonia’s commercial adoption, as evidenced by K Shipbuilding receiving approval in principle in December 2024 dfrom the American Bureau of Shipping for the design of an ammonia dual-fuel MR1 tanker. Alfa Laval contributed to the design of the entire fuel system, including the ammonia fuel supply system, fuel valves train, and vent treatment system, as well as an Aalborg ammonia dual-fuel boiler system.

Japan’s New Energy and Industrial Technology Development Organization (NEDO) says that the world’s first commercial-use ammonia-fuelled vessel, Sakigake, has successfully completed a three-month demonstration voyage, during which the vessel engaged in tugboat operations in Tokyo Bay, while achieving greenhouse gas (GHG) emission reductions of up to 95%. The vessel was completed by Nippon Yusen Kabushiki Kaisha (NYK) and IHI Power Systems in August 2024, in cooperation with Nippon Kaiji Kyokai (ClassNK) as part of a Green Innovation Fund Project. NEDO says that the vessel will continue to be used for tugboat operations in Tokyo Bay, and the organisation will continue to promote research and development of next-generation fuel vessels, including developing an ammonia-fuelled ammonia gas carrier, in conjunction with NYK, Japan Engine Corporation, IPS, and Nippon Shipyard. This vessel is scheduled to be delivered in November 2026.