Market Insight

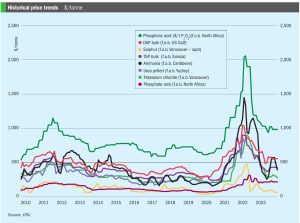

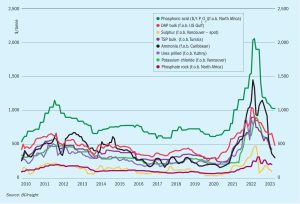

Urea: Prices continued their global decline in mid-April, including at New Orleans. The notable exception was Brazil where prices firmed due to buyer interest in the market for May and beyond.

Urea: Prices continued their global decline in mid-April, including at New Orleans. The notable exception was Brazil where prices firmed due to buyer interest in the market for May and beyond.

Urea. As February ended, urea prices found support in the US and Brazil while Europe remained subdued and Egypt struggled to find buyers. New Orleans was the one bright spot in the urea market – with NOLA prices benefitting from the meeting of suppliers and buyers at the TFI’s domestic conference. With positive sentiment all round, prices moved up $30/st, peaking at $390/st f.o.b. for March.

Urea: December began on a positive note with a flurry of Egyptian urea sales and firmer prices for delivery to Brazil. The increase in values was short lived, however, and piecemeal demand in Europe was insufficient to halt the downward trend. By mid-December, buying interest from Brazil had fizzled out, although sellers breathed a sigh of relief when India’s NFL floated a new import tender on 21st December.

Market Insight courtesy of Argus Media. Urea: Prices in general fell further in late October. Suppliers in most regions were forced to accept lower than expected net-backs due to low import demand and high producer inventories. India was the exception with IPL securing 1.7 million tonnes of urea at $400-404/t cfr under its 20th October tender.

Market Insight courtesy of Argus Media. Urea: While prices mostly fell in mid-August, the main development was the massive purchase of Chinese urea by Indian Potash Limited. IPL confirmed that, out of a total tender settlement of 1.759 million tonnes, one million tonnes will be met by Chinese exporters. This far exceeded expectations and added to the already bearish sentiment of most market players.

Market Insight courtesy of Argus Media. Urea: There was a general price upswing for both urea and ammonium nitrate in mid-June, while ammonium sulphate and urea ammonium nitrate (UAN) prices remained weak. Urea prices were pushed up in most regions as traders sought to secure cargoes across the globe – resulting in granular urea deals from the Baltic ($260-280/t f.o.b.), Egypt ($312-335/t f.o.b.), Middle East ($253-280/t f.o.b.) and China ($308-310/t f.o.b.).

Market Insight courtesy of Argus Media. Urea: Scarcity continued to drive urea prices higher in some markets at the end of April. The US market remains short on urea and prices spiked to reflect this. Nola barges for April were trading as high as $450/st f.o.b. ($490/t cfr), 55 percent up on this year’s low point. Southeast Asia remains short on urea too, amid planned and unplanned turnarounds, with one cargo trading at around $345/t f.o.b.

Market Insight courtesy of Argus Media. Urea: Prices fell in most global markets in early March as suppliers chased limited demand. Although India’s purchase tender has yet to formally conclude, IPL looks set to book 1.15 million tonnes of urea at $330-334.8/t cfr, with traders mainly sourcing from Russian and Middle Eastern producers.

Market Insight courtesy of Argus Media. Urea: The market remained weak at the start of the year with urea prices falling as producers fought for liquidity. Egyptian product fell by $40/t to $495/t f.o.b. in a matter of days, while f.o.b. prices in the Middle East and southeast Asia similarly fell to around $440/t. Urea prices in many end-user markets also slumped: US prices fell over the course of the first week of January by $30/t, Brazil by $15/t and many European markets by around $20/t.

Market Insight courtesy of Argus Media