Measuring innovation

Vatren Jurin of DunhamTrimmer proposes a sophisticated methodology that accurately tracks the global value-added fertilizer market.

Vatren Jurin of DunhamTrimmer proposes a sophisticated methodology that accurately tracks the global value-added fertilizer market.

In this CRU Insight, Anthony Rizzo explains why market participants should expect an uneven global demand picture in 2026 and highlights regional variations.

Selected highlights of the International Fertilizer Association’s Annual Conference in Monaco in mid-May.

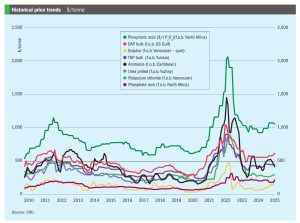

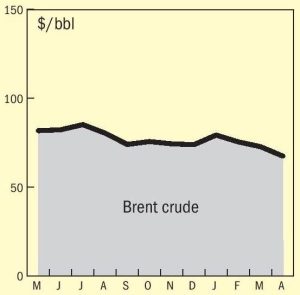

Price trends and the market outlook, 10th April 2025

Indonesia has become the epicentre of the world nickel industry, and is now seeking to raise royalty rates to capture more value from this. Will this impact upon the continuing expansion of HPAL capacity there?

While the US tariff situation remains subject to considerable uncertainty, there has already been an impact on short term trade flows, as well as investment decisions.

The Sulphur Institute (TSI) held its World Sulphur Symposium in Florence from April 8th-10th.

Sulphur markets have been on a tear over the past few months, driven by strong demand in Asia, with buyers primarily sourcing from the Middle East and Canada through late 2024 and into the early months of 2025. Steady buying from Indonesia and China, the two largest importers of sulphur, appears to have supported the market, in China’s case mainly for phosphate production as well as a variety of industrial processes, and in Indonesia’s case to feed the high pressure acid leach (HPAL) plants that are producing nickel for the battery and stainless steel industries. Prices saw a notable rally following the Chinese Lunar New Year celebrations. Nevertheless, this momentum finally began to shift as April began ago as the pace of price increases in Asia started to slow. As the spring fertilizer application season in China draws to a close, domestic prices began to drop, reaching the equivalent of a delivered price of around $272/t c.fr. As well as the narrowing window for spring application of phosphates, the decline was also driven by weakening demand amid uncertainty over tariffs and export restrictions. In southern China, phosphate producers continue to purchase import cargoes. A major phosphate producer in southwest China has been reported as having bought mainstream material at a price of $303/t c.fr, according to local market sources. Total sulphur port inventories in China had declined by 22,000 tonnes to 1.86 million tonnes by 16 April 2025. The volume at Yangtze River ports increased to 825,000 tonnes, while the port inventory at Dafeng decreased to 400,000 tonnes.

The Middle East remains the world’s largest regional exporter of sulphur, with additional capacity continuing to come from both refineries and particularly sour gas processing.

I am writing this freshly returned from the Sulphur Institute’s annual Sulphur World Symposium in Florence (for more on that see pages 24-25), where one of the topics causing some excitement was the anticipated commissioning of a demonstration plant for Travertine Technologies’ new Travertine Process. The plant is due to be commissioned at the Sabin Metals site near Rochester, New York in mid-2025 at a cost of $10.7 million. Capacity is put at “hundreds” of tonnes per year of gypsum processed, and removing “tens” of tonnes per year of CO 2 from the atmosphere.