Blue ammonia projects

Blue ammonia – ammonia produced from fossil hydrogen with carbon capture and storage (CCS) – offers a cheaper alternative than green ammonia for low carbon supply in the short term, and is more suited to retrofits.

Blue ammonia – ammonia produced from fossil hydrogen with carbon capture and storage (CCS) – offers a cheaper alternative than green ammonia for low carbon supply in the short term, and is more suited to retrofits.

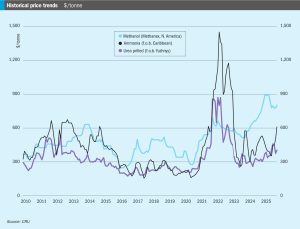

l The market looks very tight through the end of the year, though some expect supply to improve in Q4. Prices are unlikely to ease in the coming weeks. l Woodside’s Beaumont New Ammonia Project is now 97% complete, and the producer expects production from the first train in late 2025. There is no information from Gulf Coast Ammonia on when to expect commercial production. l There was an absence of fresh confirmed business into northwest Europe. Still, producers with ammonia capacity in the region are expected to be maximising output given the favourable economics at current spot natural-gas prices at the Dutch TTF.

By the end of October the ammonia market was facing an acute shortage of spot tonnage, reflected in a $60/t jump in the Tampa price for November. The benchmark Tampa price increased for the sixth straight month to its highest since February 2023 as the global ammonia supply crunch deepened. The surge at Tampa was said to be driven by good demand in the US for direct application combined with a lack of supply. Contributing factors included Nutrien shutting down its nitrogen production in Trinidad, potentially removing around 85,000 tonnes/month from the market. So far, there is no suggestion that other producers in Trinidad will follow suit, and they may even benefit from a boost natural-gas supply given the Nutrien outage, although it is unclear whether the spare gas will be directed to ammonia as opposed to other demand sources.

Ube Corporation has accelerated closure plans for its nitrogen products in Asia as part of its Vision 2030 plan. The company says that it aims to halt ammonia and related product production at its Ube City plant in Japan by March 2028, two years ahead of its previous schedule. Production of caprolactam and polyamide materials at the same plant will end by March 2027. Post-restructuring, the facility will prioritize specialty chemicals such as polyimides, separation membranes, ceramics, pharmaceuticals, and high-purity chemicals.

North Africa remains a major centre of global phosphate production, with significant production in Algeria, Tunisia and Egypt as well as Morocco, and sulphur and sulphuric acid consumption continuing to increase.

Jordan Phosphate Mines Company (JPMC) and Arab Potash Company (APC) have signed an agreement to develop an integrated industrial complex for the production of phosphoric acid, purified phosphoric acid, and specialised fertilisers. The facility will span sites in the Aqaba Special Economic Zone and Al Shediyeh, and represents a strategic collaboration between two of Jordan’s largest mining companies. The project aims to shift the country’s fertilizer sector from raw-material exports to value-added manufacturing, aligned with Jordan’s Economic Modernisation Vision. The complex will focus on high-purity phosphoric acid used in specialty fertilizers, as well as in food, pharmaceutical, and cosmetics applications. It is also expected to create both direct and indirect employment opportunities, with plans for training programmes for local engineers and technicians.

In late July, OCP Nutricrops announced that its triple superphosphate (TSP) production capacity now exceeds five million tonnes, thanks to the commissioning of the first two TSP production lines – each with a capacity of 500,000 t/a – as part of the strategic ‘TSP Hub’ programme at OCP’s massive Jorf Lasfar complex. This initiative is led by the OCP Group’s Manufacturing Special Business Unit (SBU) in coordination with OCP Nutricrops, OFAS and JESA. These flexible production lines can manufacture tailored fertilizers that integrate nutrients and additives to match specific soil and crop needs, OCP Nutricrops said.

India’s Coromandel International (CIL) is set to increase its stake in phosphate rock producer Baobab Mining and Chemicals Corporation (BMCC) in Senegal further to 71.51% from 53.8%, according to local press reports. CIL is reportedly paying $7.7 million for an additional 17.69% equity stake, after previously raising its stake from 45% in September 2024. CIL originally announced it would take a stake in BMCC in 2022, when it paid $19.6 million for a 45% stake, along with a loan of $9.7 million into BMCC for capital projects and expansion. CIL plans to use the stake to ensure long term supply security of phosphate rock.

Egypt’s Mineral Resources and Mining Industries Authority (MRMIA) has signed a memorandum of understanding with China’s Asia-Potash International Investment (Guangzhou) Co., Ltd. The MoU is designed to strengthen joint cooperation in exploring and assessing phosphate ore reserves. The objective is to maximise the added value of this crucial resource.

Upcycle Minerals Inc. has launched a brine to potassium sulphate fertilizer with carbon capture project in south-central Saskatchewan. The company says that it plans to use its mineral assets, including the Tuxford potash mineral permit and the Whiteshore and Lydden Lake Alkali Leases as feedstock for its patented process. Along with the production of potassium sulphate (SoP), the process also generates two co-products with established markets; ammonium sulphate fertilizer and precipitated calcium carbonate. Upcycle says that it intends to become an ecologically conscious, low-cost producer of SoP with low net CO2 emissions.