Africa

24 June 2026

CRU sharpens debate on CBAM and potash at AFA Cairo

Written by Natalie Noor-Drugan

CRU used its presence at the Arab Fertilizer Association’s 32nd Annual International Fertilizer Conference & Exhibition in Cairo to frame two of the meeting’s core debates: the “regulatory tsunami” around CBAM and the evolving economics of global potash supply.

CRU at AFA Cairo

The AFA conference ran from 16–18 June 2026 at the Nile Ritz Carlton in Cairo under the patronage of Egypt’s prime minister and key sector ministers, drawing regional and international fertilizer producers, technology providers and policy makers.

CRU contributed both on nitrogen regulation and potash markets, with analyst Alexander Chreky delivering a potash market briefing and analyst Ashmita Sen joining the opening regulatory panel titled “The Regulatory Tsunami – CBAM & Beyond.”

Potash markets: record demand, stable prices

In his “Potash Market Briefing – Stable pricing for potash, despite geopolitical upheaval and record demand,” Chreky told delegates that MOP prices remain elevated but are still close to their 2005–2026 average despite the war involving Iran and freight disruption risks around the Strait of Hormuz.

He highlighted that 2025 saw record imports into key potash demand centres such as Brazil and Southeast Asia, with high supply from Canada and the CIS balancing demand and keeping prices relatively stable.

Geopolitics, freights and farmer affordability

Chreky stressed that the Middle East accounts for less than 10% of global MOP supply, meaning direct physical disruption has so far been limited, but higher freight rates have pushed up delivered prices to key destinations.

He noted that any closure of Red Sea transit would mainly impact Jordanian and Israeli shipments to Asia, and warned that higher prices for other fertilizers risk squeezing farmer potash budgets even as crop prices for rice and palm oil rise on poor weather and tight supply.

Capacity wave and Arab Potash expansion

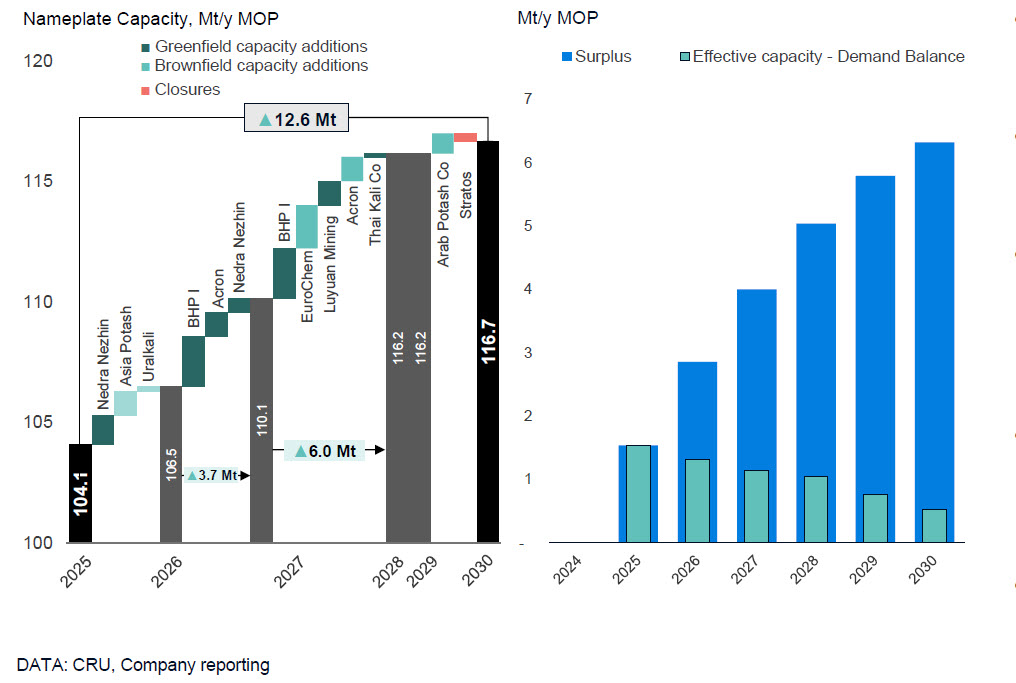

CRU’s presentation flagged a new wave of capacity additions, with 12.6 Mt of new nameplate MOP capacity expected to finish construction by 2030, outpacing demand growth and pushing the market into oversupply.

Chreky singled out Arab Potash Company’s Southern Expansion plans and related projects, which aim to lift effective capacity from just under 2.9 Mt/y today to 3.7 Mt/y by 2031, describing it as the company’s largest expansion programme in two decades.

CBAM: product by product exposure

On the “Regulatory Tsunami” panel, Sen walked the audience through CBAM exposure across urea, ammonia, ammonium nitrate/nitrates and NPKs, stressing that Europe is now a high cost marginal producer in urea after feedstock shocks since 2022.

She told delegates that Egypt and Algeria are “relatively well positioned under CBAM” on urea, with default emissions intensities of about 1.4–1.5 tCO2e per tonne versus around 2.7 tCO2e/t for many other origins, giving them a built in cost advantage as CBAM charges rise. She noted that, based on CRU’s estimates, their actual emissions are already close to the default values applied to them, which reduces the urgency to verify emissions compared with suppliers such as the US that face a larger gap between defaults and actuals.

New capacity additions will outpace demand

Hidden N₂O exposure and AN/nitrates

Sen warned that “this is really where CBAM bites hardest” for ammonium nitrate and nitrates because of the often overlooked N₂O emissions from nitric acid production, which has a global warming potential around 300 times that of CO₂.

She said EU producers have largely invested in abatement under the EU ETS, whereas exporters from regions such as the US, Trinidad and Russia face estimated 2026 CBAM costs of about $123/t, $88/t and $111/t respectively on AN/nitrates, before wider tariffs are taken into account.

US ammonia defaults versus actuals

For ammonia, Sen underlined that the key issue is the EU’s default emissions factor for the US at 3.444 tCO2e per tonne – the second highest after China – reflecting petroleum coke based plants rather than the gas based units that dominate export supply.

“If a US exporter relies on the default value, the CBAM charge can exceed $200/t,” she said, adding that exporters “will likely need to use the actual values route if they want to remain competitive in Europe,” while Egypt and Algeria face CBAM costs more in the $60–70/t range.

Trade flows: Russia loses, Arab product gains

Sen told the audience that CBAM, once netted against the wider tariff stack, “will redraw global fertilizer trade flows – but not evenly,” with Europe’s dependence on Russian nitrogen expected to fall further.

She contrasted Egypt’s indicative 2026 urea CBAM cost at around $56–57/t with Russia’s roughly $65/t plus the 6.5% ad valorem duty and an additional tariff, pushing Russia’s total burden towards $150/t and “clearly improv[ing] the relative competitiveness of Arab product.”

Limited exposure for phosphates and complex fertilizers

Sen noted that CBAM exposure for NPKs and DAP/MAP is much lower because complex fertilizers are treated largely on their embedded ammonia content, with limited burden from the phosphate side.

She cited Morocco, the largest phosphate supplier to Europe, where the 2026 CBAM cost on these complex products is around $24/t, making phosphates “relatively negligible[ly] exposed” compared with nitrogen fertilizers.

Five year outlook: Arab producers compete on carbon

Looking five years ahead, Sen said Arab producers will “increasingly compete on carbon intensity as a third advantage, alongside cost and proximity to Europe,” driving investment in low‑emissions nitrogen capacity.

She argued that CBAM is already creating a commercial market for low‑emissions fertilizer by turning carbon intensity into a direct cost advantage for suppliers able to verify emissions, especially efficient gas‑based plants in the Gulf and Egypt.

For readers wishing to follow up, CRU said enquiries on CBAM and related regulatory issues can be directed to analysts Ashmita Sen or Pranshi Goyal, who have been leading CRU’s work on this policy. For phosphate fertilizers, senior analyst Mariana Fortuna is the main contact, while potash market questions can be directed to CRU potash analyst Alexander Chreky.