Nitrogen+Syngas 400 Mar-Apr 2026

17 March 2026

Market Outlook

Market Outlook

AMMONIA

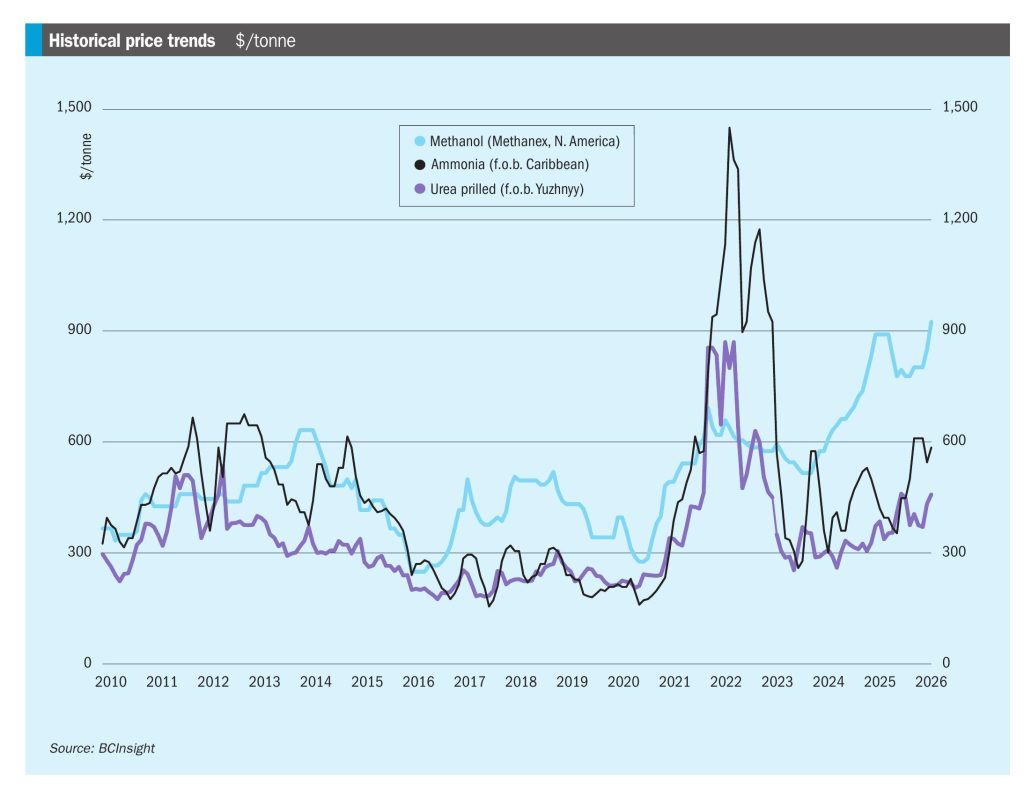

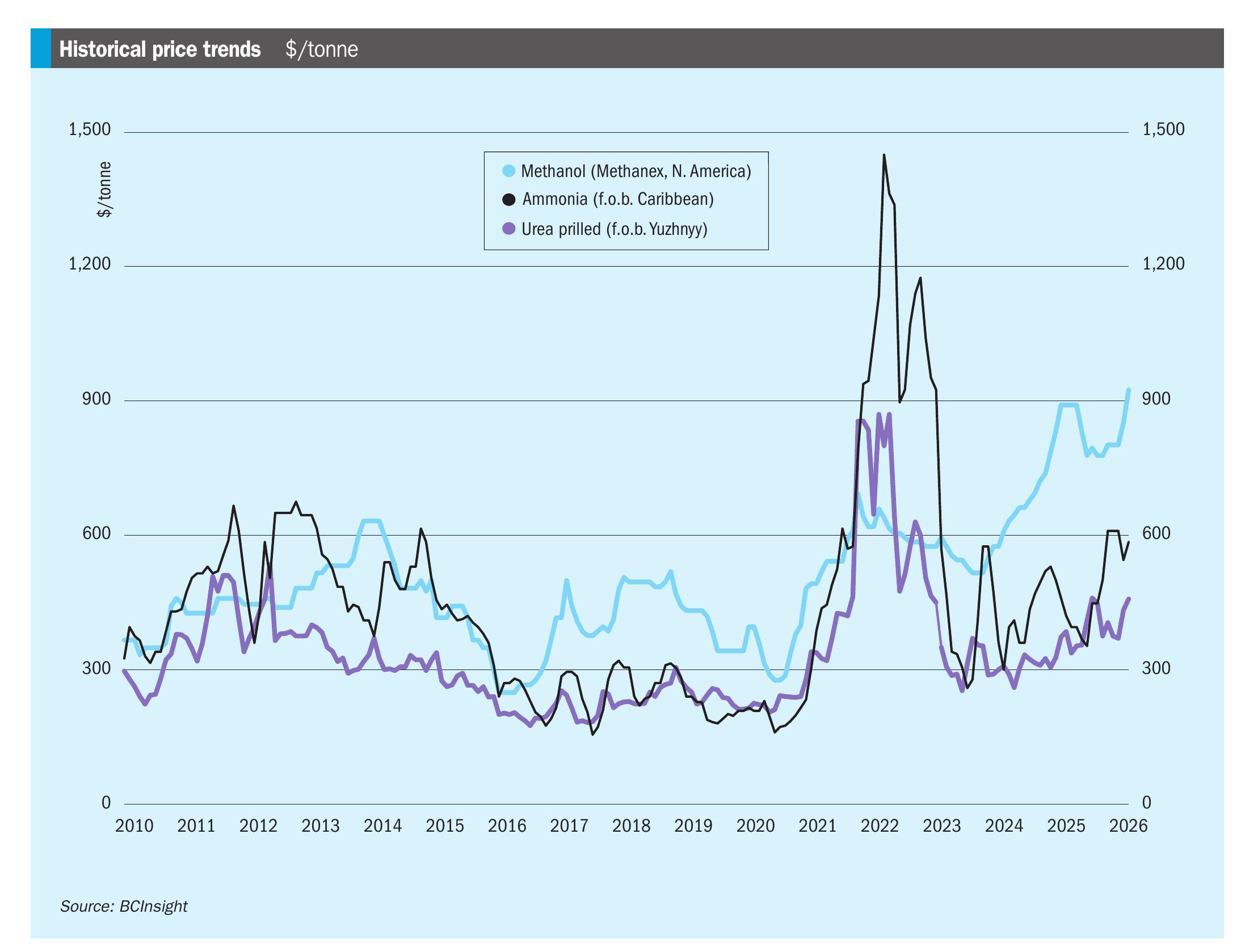

• Prices are likely to remain on an upward trajectory as long as the Strait of Hormuz remains effectively closed and Middle East export availability is constrained.

• The effect on the LNG market of a cessation of supply from Qatar and other Gulf nations is likely to increase feedstock prices in Europe and India.

• However, East Asia is relatively comfortably supplied by long-term contracts in the near term, with a steady run of scheduled arrivals continuing despite the ongoing conflict in the Middle East.

• Should the conflict in the Middle East persist, Southeast Asian producers may see further surges in demand from India. The Indian market is typically reliant on Iranian and Middle East supply, while this constrained Southeast Asia material remains the next best alternative.

UREA

• Urea prices look set to remain supported for as long as the Strait of Hormuz remains effectively closed, with significant further increases likely over the coming weeks if no resolution to the ongoing conflict in the Middle East is found.

• The supply disruption has created a precarious situation for India. Following RCF’s 18 February tender, a substantial portion of the 1.3 million tonnes of urea secured was set to be sourced from the Middle East. With several vessels now stranded, traders are scrambling to cover their positions.

• There remains significant uncertainty as to whether RCF will grant laycan extensions beyond the 31 March shipment deadline, and the potential for delayed arrivals is likely to impose further strain on India’s dwindling stock levels just as many domestic plants enter seasonal maintenance.

METHANOL

• The outbreak of hostilities in the Middle East has sent a shock through oil and gas markets, and there is likely to be a significant knock-on effect on olefins and polyolefins markets.

• Prior to this, production curtailments outside of China had tightened the market slightly. Iranian plants were already mostly down due to winter gas supply restrictions, but Trinidad and Venezuela also have gas supply restrictions, and a cold snap in the US also led to a temporary shutdown of several methanol plants. While demand remains subdued in Europe, rapidly oil prices point to rising methanol prices.

• Meanwhile, China’s January methanol output was the second-highest monthly level in recent years. Plant utilisation rates are above 90% while demand remains relatively weak, leaving the market oversupplied. Port inventories were up at 1.77 million tonnes