Market Outlook

• Continuing oversupply means that ammonia prices should continue to come under pressure moving into 2H April, though it remains to be seen just how much further values in Asia can decline before producers begin to shutter output.

• Continuing oversupply means that ammonia prices should continue to come under pressure moving into 2H April, though it remains to be seen just how much further values in Asia can decline before producers begin to shutter output.

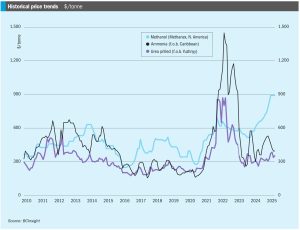

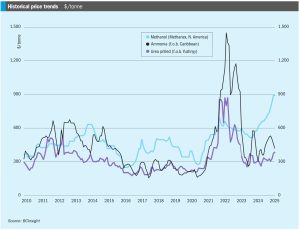

In mid-April, Ammonia prices both east and west of Suez remained firmly oriented to the downside, with supply still heavily outweighing demand and suppliers scrambling to place excess tonnage. Bearish market sentiment was exemplified by a Trammo sale to OCP at $415/t c.fr Morocco, $20/t short of Tampa’s c.fr settlement for April and around $44/t down on February.

Global gas demand has returned to growth after the supply shock of 2022-23, but geopolitical tensions and short supply in LNG markets.

P r esident Trump’s flurry of activity in his first month of office has not only upended the global political order that has existed, more or less, since the US rearranged it to its satisfaction in 1945, but has also had a seismic impact on world trade. How the various strands of US policy will play out remains highly uncertain, but some clear trends are beginning to emerge.

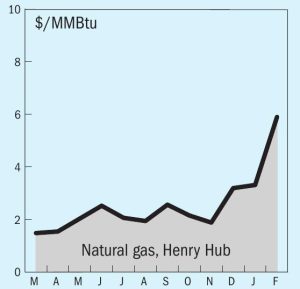

Support for ammonia prices in markets east of Suez eroded during February. The ongoing bubble of support seen in NW Europe remained just about intact, though news of further declines at Tampa for March and slumping natural-gas prices should begin to eat away at any remaining support in the West. After declining $70/t during the first two months of 2025, the Tampa settlement between Yara and Mosaic was revised down a further $40/t for March, imposing further downward pressure on f.o.b. values in Trinidad and the US Gulf.

• Prices look set to come under further pressure moving into March, particularly east of Suez. Prices in the West – specifically in northwest Europe – have enjoyed a partial degree of support through February, though this appears unlikely to hold for much longer.

• Sulphur prices have been revised higher in the latest forecast after supply from the Middle East was lower than expected in February, and buyers with uncovered demand were forced to chase prices upwards. UAE sulphur exports normally fall at the start of the year due to scheduled maintenance, but sales in February this year were 200,000 tonnes short of what is typical. Prices may climb more than expected as buyers scramble to cover their shorts. If supply is slower to return than currently anticipated, momentum may push prices even higher in the short term.

Aurubis AG has reported operating earnings before taxes of euro130 million ($134.8 million) for the first quarter of its fiscal year 2024/25, up around 17% on the figure for the equivalent period of last year (€111 million or $115.1 million). The company’s Custom Smelting & Products (CSP) segment posted €125 million ($129.7 million) in EBT compared with €107 million ($111 million) in the previous year. CSP comprises production facilities for processing copper concentrates as well as for manufacturing and marketing standard and specialty products, such as cathodes, wire rod, continuous cast shapes, strip products, sulphuric acid and iron silicate, via smelters in Hamburg and Pirdop, Bulgaria. The company attributes the higher EBT to higher metal prices, considerably increased sulphuric acid revenues, and robust earnings from copper product sales and lower costs, which more than compensated for a year-over-year decline in treatment and refining charges with lower concentrate throughput.

Global sulphur benchmarks rallied at the end of February, underpinned by strong demand in Indonesia and stock drawdowns in China as fresh European sanctions on Russia targeted the port of Ust-Luga. Chinese buyers paid up to $225t/t c.fr for a cargo, with unconfirmed rumours of business at even higher levels. However, delivered prices still lag domestic port spot prices in China, which are now assessed at a delivered-price equivalent of around $242/t c.fr. China’s delivered sulphur price jumped significantly as port inventories declined, and new arrivals were limited. Only two new cargoes were reported in the last week of February, one from a mainstream source into southern China at $205/t c.fr, and the second at $225/t c.fr by a phosphate producer for the Yangtze River. The sulphur port spot transaction price is reported at around 2,0402,050 yuan/t FCA ($281-283/t), with the low-end up $26/t and high-end up $25/t compared with previous settlements. That port price indicates delivered values at around $242/t c.fr, which is $17/t higher than the import price on the Yangtze. Phosphate producers need to purchase more sulphur to meet the increased buying activity in northeastern market and the improving spring application season demand in northern China. Still, market sales availability is limited, as most port tonnes are held by traders instead of end-users, while traders are selling limited quantities now to push prices higher. Chinese total port inventory dropped to 1.89 million tonnes by 26 February 2025. The quantity at Yangtze river ports declined 59,000 tonnes to 633,000 tonnes, while Dafeng port inventory decreased 20,000 tonnes to 450,000 tonnes.

The past few weeks have seen sulphur prices spiking after a steady rise since 3Q 2024. At time of writing, delivered prices to a variety of locations were around $280/t c.fr, their highest level since mid-2022 when the price of commodities of all kinds jumped in the wake of the Russian invasion of Ukraine and subsequent sanctions. Steady buying from Indonesia and China, the two largest importers of sulphur, appears to have supported the market, in China’s case mainly for phosphate production as well as a variety of industrial processes, and in Indonesia’s case to feed the high pressure acid leach (HPAL) plants that are producing nickel for the battery and stainless steel industries. Although Chinese buying has dropped off slightly since Lunar New Year, and demand has also slackened in India, Indonesia’s appetite continues unabated, having tripled its nickel production since the start of the decade to become the world’s largest producer, representing 60% of global supply in 2024.