People

Leo Alders , the CEO of LAT Nitrogen, is the new president of Fertilizers Europe. He was elected with immediate effect at an extraordinary general assembly on 5th December last year.

Leo Alders , the CEO of LAT Nitrogen, is the new president of Fertilizers Europe. He was elected with immediate effect at an extraordinary general assembly on 5th December last year.

Prices will remain stable-to-soft across the board, though benchmarks could remain slightly more supported in the short-term than previously thought, with more significant declines likely in Q2-Q3.

Nitrogen magazine, as it originally began life in It has been a tough few years for the European nitrogen industry, and between covid, gas price spikes and Russian sanctions, not all companies have weathered the storm. Now that the initial shock of the sky-high ammonia prices that the closure of the Black Sea and the cutting off of almost 40% of Europe’s gas supplies has passed, and the world gas and ammonia markets have largely adjusted to the new reality, prices are coming back down. But it seems that in its wake it may leave quite a different European nitrogen industry from the one that existed in 2019.

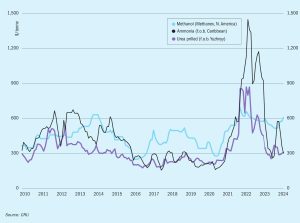

Ammonia pricing in the US Mid-West stood at $625/st f.o.b. in February, with applications to field continuing to ramp up. Prices in the US Gulf remain pegged in the low-to-mid$400s/t f.o.b. Recent production outages in the region have largely subsided, though an unexpectedly early uptick in seasonal demand from local buyers is likely to provide a degree of price support moving forward. The Tampa ammonia settlement for March has been settled by Yara and Mosaic at a $445/t c.fr rollover, largely in line with market expectations. The North American market remains detached from the considerably more oversupplied global ammonia scene.

Sulphur prices declined in Q4 following the increases seen during Q3, because of ample availability and limited spot demand. One contributing factor was that phosphate fertilizer producers in China, the largest importer of sulphur, have cut downstream production due to increased export restrictions. In addition, high sulphur stocks at Chinese ports and continuing high domestic sulphur production mean that domestic buyers have other options aside from international purchases.

Sulphur prices are expected to increase during H1 2024, reversing the trend of recent declines, though good availability will limit the upside to price gains in the short term. However, should fertilizer production prove weaker than expected, prices may remain below expected levels.

Ammonia prices are expected to remain soft moving through January with little in the way of price support from both a supply and demand perspective. Weakened global sentiment was characterised by news of January’s Tampa settlement $100/t down on December at $525/t CFR, with further declines anticipated in Q1 once the Gulf Coast Ammonia (GCA) project comes online. Traders returned to their desks in the New Year and ammonia prices extended losses amid a stable supply outlook and a distinct lack of downstream industrial and fertilizer demand.

Ammonia prices are expected to remain soft moving through January into February, with little in the way of price support from both a supply and demand perspective. January’s Tampa settlement was $100/t down on December at $525/t CFR.

We look ahead at fertilizer industry prospects for the next 12 months, including the key economic and agricultural drivers likely to shape the market during 2024.

With phosphate supply concerns persisting as 2023 draws to a close, CRU’s Senior Analyst Logan Collins looks back at what’s been a dynamic year for the global phosphate market.