Market Insight

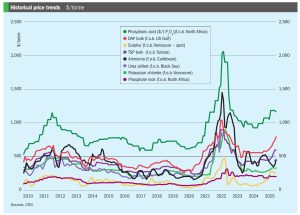

Price trends and market outlook, 23rd October 2025

Price trends and market outlook, 23rd October 2025

Nutrien said in its 3Q results that it has initiated a review of strategic alternatives for its phosphate business, which could include reconfiguring operations, strategic partnerships or a potential sale. A final decision on the future of the phosphate business will be taken in 2026, according to the company .

John Carr, Lei Zhang & Yu Zheng of Syensqo review currently available decadmiation techniques, including the company’s ACCO-PHOS® technology.

North Africa remains a major centre of global phosphate production, with significant production in Algeria, Tunisia and Egypt as well as Morocco, and sulphur and sulphuric acid consumption continuing to increase.

In late July, OCP Nutricrops announced that its triple superphosphate (TSP) production capacity now exceeds five million tonnes, thanks to the commissioning of the first two TSP production lines – each with a capacity of 500,000 t/a – as part of the strategic ‘TSP Hub’ programme at OCP’s massive Jorf Lasfar complex. This initiative is led by the OCP Group’s Manufacturing Special Business Unit (SBU) in coordination with OCP Nutricrops, OFAS and JESA. These flexible production lines can manufacture tailored fertilizers that integrate nutrients and additives to match specific soil and crop needs, OCP Nutricrops said.

In addition to the above deal with Morocco, the Bangladesh Agricultural Development Corporation (BADC), part of the Bangladesh Ministry of Agriculture, has signed a contract to import both triple superphosphate (TSP) and di-ammonium phosphate (DAP) fertilisers from Malaysia. The agreement was signed on 17 July 2025 in Kuala Lumpur by Mohammed Ruhul Amin Khan, chairman of BADC, and representatives of Selcra Niaga. Under the contract, BADC will import 280,000 tonnes of TSP and 280,000 tonnes of DAP from Malaysia. According to BADC officials, this landmark deal is expected to play a crucial role in ensuring the timely delivery of non-urea fertilisers to farmers. The move aims to strengthen Bangladesh's efforts toward building an efficient and sustainable agricultural system.

OCP can now produce more than five million tonnes of triple superphosphate (TSP) annually.

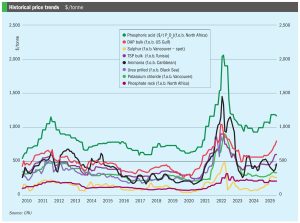

Price trends and market outlook, 21st August 2025

Danny Luu , Processing Engineer, Derrick Corporation, outlines the transformative role of fine screening in potash and phosphate processing.

Marc Sonveaux highlights Prayon’s innovative approach to fluorosilicic acid (FSA) valorisation.