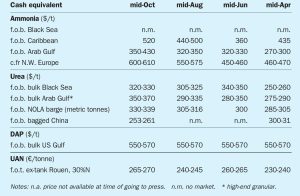

In October, ammonia benchmarks were more or less stable across the board. West of Suez, supply from Algeria was constrained by an ongoing turnaround at one of domestic player Sorfert’s production units. Still, demand from NW Europe remained quiet, although CF was set to receive a 15,000 tonne spot cargo from Hexagon some time in November, reportedly sourced somewhere in the region of $530/t f.o.b. Turkey. While regional supply appeared tight, steadily improving output from Trinidad and the US Gulf could alleviate recent pressures, with many players of the opinion that Yara and Mosaic could agree a $560/t c.fr rollover for November at Tampa as a result.