Market Insight

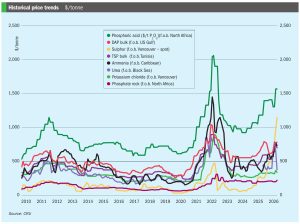

Price trends and market outlook, 17th June 2026.

Price trends and market outlook, 17th June 2026.

Cover story! Sergio Saenz, CEO of International Minerals Carlsbad (IMC), and Kelvin Feist, the company’s Commercial Consultant, talk to Fertilizer International ahead of Southwestern Fertilizer Conference.

Hunter Swisher, the CEO of Phospholutions, explains how the company’s RhizoSorb® technology can be integrated into phosphate fertilizer plants.

We speak to Justin Rackleff, CRU’s Americas Lead, Fertilizer Value Chain, about the US market state-of-play ahead of this year's Southwestern Fertilizer Conference.

Fertilizer International talks to ICL about improving nutrient use efficiency and some of its newest product innovations.

We interview Alison Coughlin, CME Group’s Director of Commodity Research and Product Development, about the valuable market role of fertilizer futures.

Sultech Global Innovation Corp’s patented micronisation technology is helping field-applied sulphur perform throughout the crop-year.

Methanex says that it has been unable to agree to a new natural gas contract for its 860,000 t/a Titan methanol plant in Trinidad and Tobago, and, as a result, will begin the process of indefinitely idling the facility. Titan’s existing natural gas contract expires in the third quarter of 2026. Methanex says that it will undertake a preservation process at the Titan plant to provide options for a future restart should conditions materially improve. The neighbouring 1/7 million t/a Atlas methanol plant, a joint venture in which Methanex holds a 63.1% economic interest, remains indefinitely idled in a preserved state.

JSW Steel says that it has signed a memorandum of understanding with Bharatia and Carbon Iceland International to develop a 300,000 t/a green methanol facility. The plant will capture carbon dioxide emissions from JSW Steel’s existing Raigad facility in Maharashtra state, and combine them with hydrogen produced from water electrolysis using renewable electricity. Under the […]

SunGas Renewables Inc. has said that it will cease further development of the Beaver Lake Biofuels project, a proposed wood fibre-to-low carbon methanol facility in Louisiana. The project was to have involved integrating three of SunGas S1000 syngas production systems with downstream technologies to produce approximately 553,000 t/a of low carbon methanol, and geological storage […]