Nitrogen+Syngas 400 Mar-Apr 2026

17 March 2026

Where will new urea capacity be built?

UREA

Where will new urea capacity be built?

Changing markets for feedstock, shifts in demand, carbon pricing and geopolitics all help dictate the location of new urea capacity.

Urea remains the nitrogen fertilizer of choice for much of the world, and the global traded market for urea stood at 57 million t/a in 2025, almost 30% of all production. Total production capacity worldwide was an estimated 240 million t/a that year, with 85% of this operational. New plant construction continues to stand at several million tonnes per year, with 40 million t/a of net capacity due to be added between 2025-2030.

Urea demand

Urea demand falls broadly into two categories; agricultural demand as a fertilizer, and chemical or so-called ‘technical’ uses. Technical urea covers demand for urea-formaldehyde resins and melamine for construction, cyanuric acid, diesel exhaust fluid to break down nitrogen oxides in exhausts, an animal feed additive, and a variety of other smaller uses. These represent about 20% of demand, concentrated mainly in China and east Asia, with other notable demand centres in industrialised regions such as Europe and North America.

Agricultural uses dominate urea demand, with the major consuming countries being China, India, Brazil and the United States, in that order – these four countries collectively represent 62% of all agricultural demand. Other major consumers include Pakistan, Iran, Turkey, Indonesia, Argentina, Canada, Nigeria, Bangladesh, Thailand and Vietnam. Urea has become the major nitrogen fertilizer of choice for most of the world because of its high nitrogen content (46%), making it the most economical way to transport nitrogen. Its use is less prevalent in more northerly latitudes, where shorter growing seasons favour the use of ammonium nitrate or AN variants such as CAN or UAN, as the nitrogen in these fertilizers is more readily available to plants as they grow, not needing to be first hydrolysed to nitrate in the same way as urea.

As Table 1 shows, the combination of technical and agricultural demand makes China the largest overall consumer by some way, dominating the total demand figure for East Asia (China represents 98% of this total), while South Asia is the other demand hotspot, 80% of this accounted for by India. Brazil, the US and the combination of Indonesia, Vietnam and Thailand make South America, North America and Southeast Asia significant secondary markets.

Production

Urea production is via the conversion of two ammonia molecules into an ammonium carbamate molecule with the addition of carbon dioxide as a bridge, and its subsequent dehydration to urea. While there is some standalone urea capacity, most urea plants are therefore co-located with ammonia plants. It generally makes economic sense to site urea plants where ammonia production is cheapest and then transport urea to market, as solid urea is much more easily and safely and hence cheaply transported than liquid ammonia. This is why 30% of urea is traded across international boundaries but less than 10% of ammonia.

Early ammonia production tended to come from gasification of coal, and hence was clustered in major industrial regions, especially Europe and the United States. However, beginning around the 1960s, natural gas-based ammonia production came to predominate, as it did not need the solid handling and gasification section, greatly reducing capital costs. In the absence of a global natural gas market, natural gas was often ‘stranded’ in remote locations away from demand centres, and ammonia/ urea production became a viable way of monetising this gas. In this way, new clusters of urea production grew up in, e.g. the Middle East, Southeast Asia and central Asia/Russia, aimed at export to major consuming regions.

“For some years now, China has sought to manage domestic demand and production via the imposition of export controls…”

However, the switch towards natural gas as the major source of power generation in the late 20th century and the gradual evolution of first regional gas markets, via pipeline, and eventually global gas markets, via shipping of liquefied natural gas (LNG) altered the economics of gas-based ammonia/urea production. LNG plants were often more profitable than urea production, and gas prices began to rise as demand increased. Freight rates became important in the profitability of remote production, and this led to some switching away from gas-based production and back towards coal gasification. Meanwhile, some major consumers with little or no domestic gas reserves sought greater control over availability of urea, rather than depending on international markets, and developed almost exclusively coal-based ammonia-urea production, as was seen predominantly in China, but also Vietnam.

The production situation seen in Table 1 is the result of all of these streams of urea market development. Production in China/East Asia is roughly balanced, as it has been government policy to develop sufficient domestic capacity to feed domestic demand. The Middle East and Russia/Central Asia remain major exporting regions due to their large reserves of natural gas (the other is Central Asia), and Brazil and India, and to a lesser extent the US, remain major importing regions. Notable is the build up of export capacity in Africa, one of the few regions of the world that still has large, untapped and to a significant extent still ‘stranded’ gas reserves. Nigeria and Egypt, and to a lesser extent Algeria have become the dominant producers and exporters here. These three represent almost all African production.

Policy and regulatory drivers

While the availability of low cost feedstock has been a major factor in developing ammonia-urea capacity over the past few decades, government policy decisions have also loomed large and distorted the market to a greater or lesser degree. The most major impacts have come from China, India and Europe. In the wake of the terrible famines of 1959-61, China set itself on a policy course of total self-sufficiency in food production, and self-sufficiency in fertilizer production was seen as the best guarantor of this. The Chinese urea industry kept up with rapidly rising demand, and was even allowed to outpace domestic demand for the first two decades of the 21st century, turning the country into a major exporter, before policy changes to pollution control and a clampdown on over-use of nitrate and other fertilizers led to a rationalisation of the industry in the 2010s. For some years now, China has sought to manage domestic demand and production via the imposition of export controls which effectively shut down exports on a seasonal basis. China continues to build new urea capacity, and around 26 million t/a of new urea capacity has or is expected to be commissioned between 2025 and 2030.

India also sought self-sufficiency in urea production, but poor quality Indian coal meant that the coal-gasification based capacity that China developed did not flourish in India, where the only two coal-based plants suffered many technical issues and low operating rates, and were eventually converted to gas-based production. India’s relatively low domestic gas reserves however had to compete with power demand, and by the 1990s, there was effectively a moratorium on new urea plant construction, leading to a widening demand gap which was filled by imports. The Modi government has attempted to close this gap by importing large quantities of LNG to feed new domestic urea production, and, somewhat less successfully, to use coalbed methane and coal gasification to supplement this. But while India continues to build new urea capacity, it has not kept pace with rising demand, and the country remains a major importer.

Europe has set strict environmental standards for its domestic industries, which has placed a relatively heavy burden on fertilizer production. Gas and electricity prices have been high, and in the wake of the Russian invasion of Ukraine gas prices have made domestic ammonia production prohibitively expensive on occasion. The impact of the gas restrictions from Russia can be seen in the very low operating rate of urea production in eastern Europe (Table 2). The recent inception of the Carbon Border Adjustment Mechanism (CBAM), a tax on the carbon content of fertilizers imported from overseas, has helped redress the balance to an extent, but may open Europe up to a wave of imported ‘blue’ ammonia from the United States over the next few years, and Table 2 also shows that western European production remains disadvantaged.

The sanctions imposed on Russia, meanwhile, have crimped exports to Europe, though Russian urea has found other outlets. More devastating has been a recent wave of attacks by Ukraine on Russian production facilities which have reduced output.

Table 2 also shows very low operating rates in central and southern America. Most Brazilian capacity has closed for a variety of reasons. Some of this has been economic, or to do with lack of feedstock availability, but a series of scandals that forced a restructuring of state oil and gas giant Petrobras have also played their part. While Brazil remains a large urea importer, it has actually turned increasingly to cheap Chinese ammonium sulphate in the past couple of years to make up nitrogen deficits in a more affordable way.

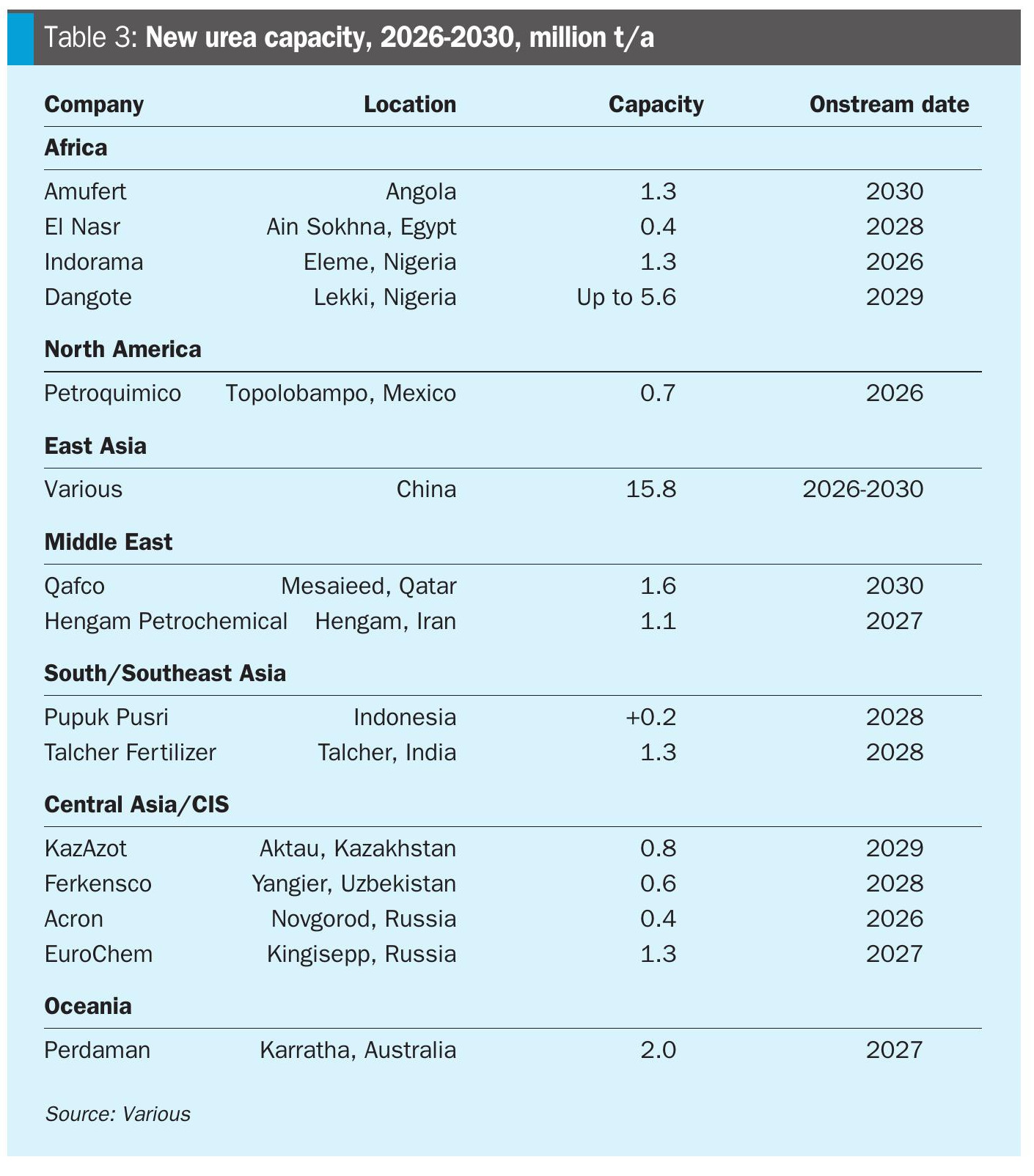

New capacity

Table 3 lists new urea capacity under construction or under development around the world. These are projects judged to be firm or probable over that time scale, but omit a number of more speculative projects or those which might not be completed by 2030. However, the conclusions appear to be clear – new urea capacity continues to centre in China, where rising domestic availability is likely to lead to increased exports over the period. Chinese coal costs remain relatively manageable for producers as power generation continues to switch towards renewables and away from coal-fired power, leaving more domestic coal available for chemical production. Outside of China, the main additions are likely to come from relatively ‘stranded’ gas in Africa, Central Asia and Australia, together with some additional coal-based capacity in India.