Sulphur 419 Jul-Aug 2025

16 July 2025

Titanium dioxide and sulphuric acid

TITANIUM DIOXIDE

Titanium dioxide and sulphuric acid

Titanium dioxide is one of the major chemical uses for sulphuric acid outside of phosphate and metals processing, and sulphate route plants remain concentrated in China.

Titanium dioxide is a major industrial chemical and a significant use for sulphuric acid. It finds use mainly as a pigment; titanium dioxide is a brilliant white compound with a high refractive index. This means that when it is dispersed in a binding agent, typically a resin of some kind, it tends to have a greater difference from the refractive index of the binder, and hence tends to look whiter and more opaque than other comparable white pigments such as calcium carbonate or zinc sulphate. This gives e.g. paints greater opacity and ‘hiding power’; the ability to cover an underlying coat without the colour showing through, and as such makes titanium dioxide highly in demand for paint and ink formulations. It is also widely used in the paper industry and in plastics for much the same reason, and it is also used as a whitening agent in toothpaste and many other household items. It is also extremely stable with respect to direct sunlight, and so micro-fine grades are used in cosmetics and sunscreens. Overall the paints and coatings industry represents around 55% of the titanium dioxide market, plastics 25% and paper 9%.

In terms of tonnage, the global market for titanium dioxide was around 6.2 million t/a in 2024. Because it is used in so many finished consumer products, and because the paint industry is closely tied to the fortunes of the construction industry, titanium dioxide demand tends to fairly closely parallel GDP growth, and has averaged around 2.5% over the long term.

Anatase vs rutile

Titanium dioxide has two main crystal structures, anatase and rutile (there is also a third form, brookite, but this is not widely used). Anatase is a bipyramidal structure, while rutile is tetrahedral. This gives rutile titanium dioxide a higher refractive index than the anatase phase (about 2.7 – 2.8 as compared to 2.55) and hence it has slightly higher opacity and hiding power. It also has higher mechanical strength, and weathers better when exposed to sunlight and rain. However, it is also generally more expensive to produce. For this reason, anatase tends to be favoured for less demanding applications such as highway paints, interior paints and plastic filling. Untreated rutile is used in the paper industry, and treated rutile for demanding exterior paint applications.

TiO2 production

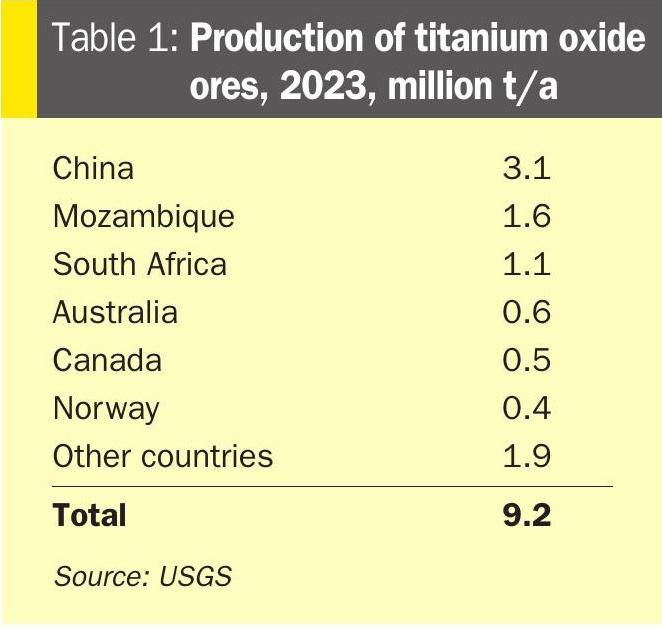

Titanium dioxide is produced from titanium-bearing rock, which tends to be mined in places such as China, Mozambique and South Africa. Table 1 shows mined production from the main producing nations in 2023. Anatase titanium dioxide comes from ilmenite, which is the main titanium ore, accounting for 90% of all production, while rutile ore is mined mainly in the US, Sierra Leone and South Africa.

There are two major competing routes for processing titanium ore; treatment with sulphuric acid, or via chlorination and subsequent oxidation. Production of finished titanium dioxide is split roughly 50-50 between the chloride and sulphate routes.

The chloride route mixes the ore with carbon and reacted in a fluidised bed with chlorine gas at 900C to produce titanium tetrachloride. The mixed chlorides are cooled. Iron, manganese and chromium chlorides can be removed by condensation. The remaining vapour is condensed to a liquid and fractionally distilled to produce a pure form of TiCl4 . This is then reacted with oxygen to form titanium dioxide and recover the chlorine to a recycle. The titanium dioxide produced is exclusively the rutile form. While chloride route TiO2 is widely regarded as a superior product, chlorine availability depends on the chloralkali industry, which electrolyses sodium or potassium chloride to yield chlorine gas and sodium or potassium hydroxide, and depends on electricity as the main ‘feedstock’, which affects cost. It also requires large volumes of chlorine gas, which presents potential safety issues.

In the sulphate process, the titanium-bearing ore is dried, ground and then agitated with concentrated sulphuric acid in a batch or continuous exothermic reaction. The titanyl sulphate is hydrolysed to produce a colloidal TiO2 hydrate, which needs to be washed and filtered prior to feeding into a calciner at 900-1,250°C to produce TiO2 It tends to be a lower cost process overall, depending on the cost of acid, but unless there is careful control of the reaction it generally produces a lower grade product. It also generates dilute sulphuric acid waste which requires treatment, though process improvements mean that acid recycling has reduced the volumes of waste acid produced. Enhancing the recoverability and saleability of by-products such as iron sulphates, iron oxides, gypsum and spent sulphuric acid can all help improve the efficiency and environmental credentials of sulphate-based plants.

The quantity of sulphuric acid consumed in the process mainly depends on the type of ore feedstock, and can vary between around 2.5 tonnes per tonne product and 4.2 tonnes per tonne product. This means that sulphuric acid costs can have a bearing on titanium dioxide production at the margins – anatase grade TiO2 typically retails for around $2,000-3,000/tonne, of which sulphuric acid cost represents perhaps a few hundred dollars. In general, every $10/t increase in the price of sulphur pushes up the price of manufacturing titanium dioxide by about $9/t. This can be problematic for titanium dioxide producers, as sulphuric acid costs are driven by phosphate and metals markets. On the other hand, TiO2 consumers such as paint manufacturers are generally relatively able to pass costs on to end users, and acid costs really only impinge on titanium dioxide markets when they reach very high levels.

China

During the 1990s, the chloride route seemed to be winning out in the US and Europe, as well as the Middle East, due to its higher quality product and lower levels of acid waste. However, the sulphate route returned with the rise of Chinese production. Chinese production of TiO2 has grown rapidly this century, from around 1.1 million t/a in 2010 to 4.8 million t/a by 2024, with total installed capacity reaching 6.05 million t/a in 2024 according to producer Titanos. Around 80% of Chinese production uses the sulphate route, and now accounts for most sulphate route production worldwide. Outside of China, there have been very few new greenfield TiO2 plants built in the past 30 years. There was a wave of new chloride-route plant construction during the early 1990s, and some sulphate plants built in India and Malaysia, but most new capacity has been in China. Chinese titanium ore mining has expanded rapidly this century, and as Table 1 shows China now mines 3.1 million t/a of ore, making it the largest miner worldwide, but the country’s finished TiO2 capacity has outstripped China’s ability to feed it with domestically produced ore, and so in order to feed TiO2 production it must also import large volumes of titanium ores from elsewhere in the world. Chinese imports of titanium ores reached 4.3 million t/a in 2023.

All of this explains why China has come to dominate the use of sulphuric acid in the TiO2 industry. In 2024 China used 13.0 million t/a of sulphuric acid for titanium dioxide production, representing 86% of all sulphuric acid use in TiO2 manufacture. Europe represented another 1.0 million t/a (7%), with small volumes also consumed in Japan, Brazil, India, Canada and Malaysia.

Chinese production of TiO2 continues to increase. Production increased by 606,000 t/a (16.5%) in 2024 compared to 2023. Production runs significantly ahead of domestic demand, particularly as the housing and real estate sectors in China – the main use for paints – are in a slump caused by overcapacity. As a result China exports large tonnages of TiO2 elsewhere, with total exports of 1.9 million t/a in 2024, an increase of 16% on 2023. India was the main destination (15% of exports), as well as Brazil (7%), Turkey (6%), South Korea (5%), Russia, Indonesia, Vietnam, and the UAE.

Anti-dumping

Large exports of titanium dioxide from China have in turn led to anti-dumping investigations in various countries to protect domestic production. In 2024 the EU, India, Brazil, and Saudi Arabia all launched anti-dumping investigations. In January this year the EU agreed anti-dumping duties on Chinese TiO2 for five years, with levels of euro 250/t for Anhui Jinhe Group, euro 740/t for Lomon Billions Group, and euro 640-740/t for other companies. Nevertheless, Chinese producers expect that exports will rise to 2.05 million t/a in 2025, an 8% increase on 2024, as domestic consumption remains relatively weak in spite of a recovery in industrial coatings, plastics and polymers.

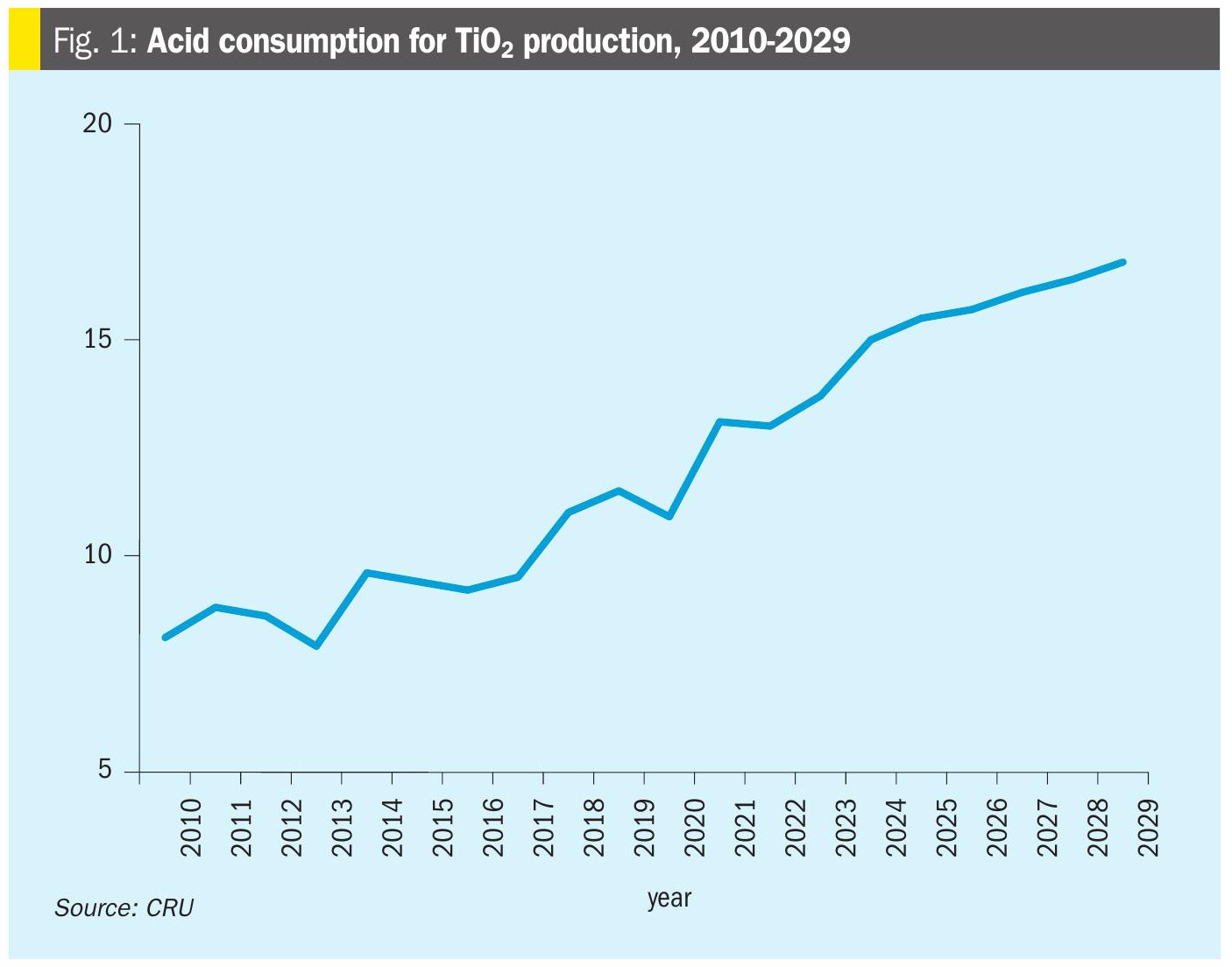

Increasing production

As Figure 1 shows, while global economic conditions can cause slowdowns or contractions in titanium dioxide production, such as the dip in 2020 caused by the covid-19 pandemic, in general it continues to grow at GDP-level rates. On the production side, China’s push for increased TiO2 output seems to be showing no signs of slowing down at the moment in spite of weak domestic demand. Essentially all new marginal production is expected to come from China over the next five years. While there is some chloride route production and new chloride route plants planned, much of this increase will come from sulphuric acid route production, and this will mean additional acid demand. As shown in Figure 1, acid demand for titanium dioxide production is expected to rise from 15.0 million t/a in 2024 to 16.8 million t/a in 2029, an increase of 1.8 million t/a, with 1.6 million t/a of that projected to come from China, and India representing most of the remainder.