Nitrogen+Syngas 396 Jul-Aug 2025

8 July 2025

Sustainable methanol: A multi-pathway fuel

DECARBONISATION

Sustainable methanol: A multi-pathway fuel

No longer viewed as only a chemical feedstock, methanol is increasingly being regarded as a low-carbon energy carrier. Zinovia Skoufa of Johnson Matthey discusses the role of sustainable methanol as a multi-pathway fuel for the energy transition.

Methanol has long been a foundational chemical in global industry, used to manufacture paints, adhesives, synthetic fabrics and thousands of other products. Increasingly, however, it is being viewed not only as a chemical feedstock, but as a low-carbon energy carrier. Its ability to be produced from a variety of sustainable sources, and to serve both as a fuel and a platform for further chemical synthesis, positions it as a highly flexible and scalable option in the energy transition.

What distinguishes sustainable methanol is the potential of carbon intensity reduction due to the origin of its feedstocks, of which there are various possible combinations. Unlike conventional methanol, which is typically derived from natural gas or coal, sustainable methanol is produced using low-carbon or renewable inputs. These include biomass and organic waste, non-recyclable municipal solid waste, and captured CO2 combined with green hydrogen. Each of these routes varies in technical complexity and regional suitability, but together they provide a compelling portfolio of solutions for reducing lifecycle emissions, improving resource efficiency and building energy resilience.

As governments, industries and financiers accelerate their decarbonisation strategies, sustainable methanol is gaining traction as a practical, deployable technology. It can be integrated into existing infrastructure, used in hard-to-electrify sectors, and scaled globally using well-understood processes. Its role is not limited to one use case or region. Instead, it offers a suite of pathways that can be applied across diverse geographies and supply chains.

Production pathways: Biomass, waste and CO2

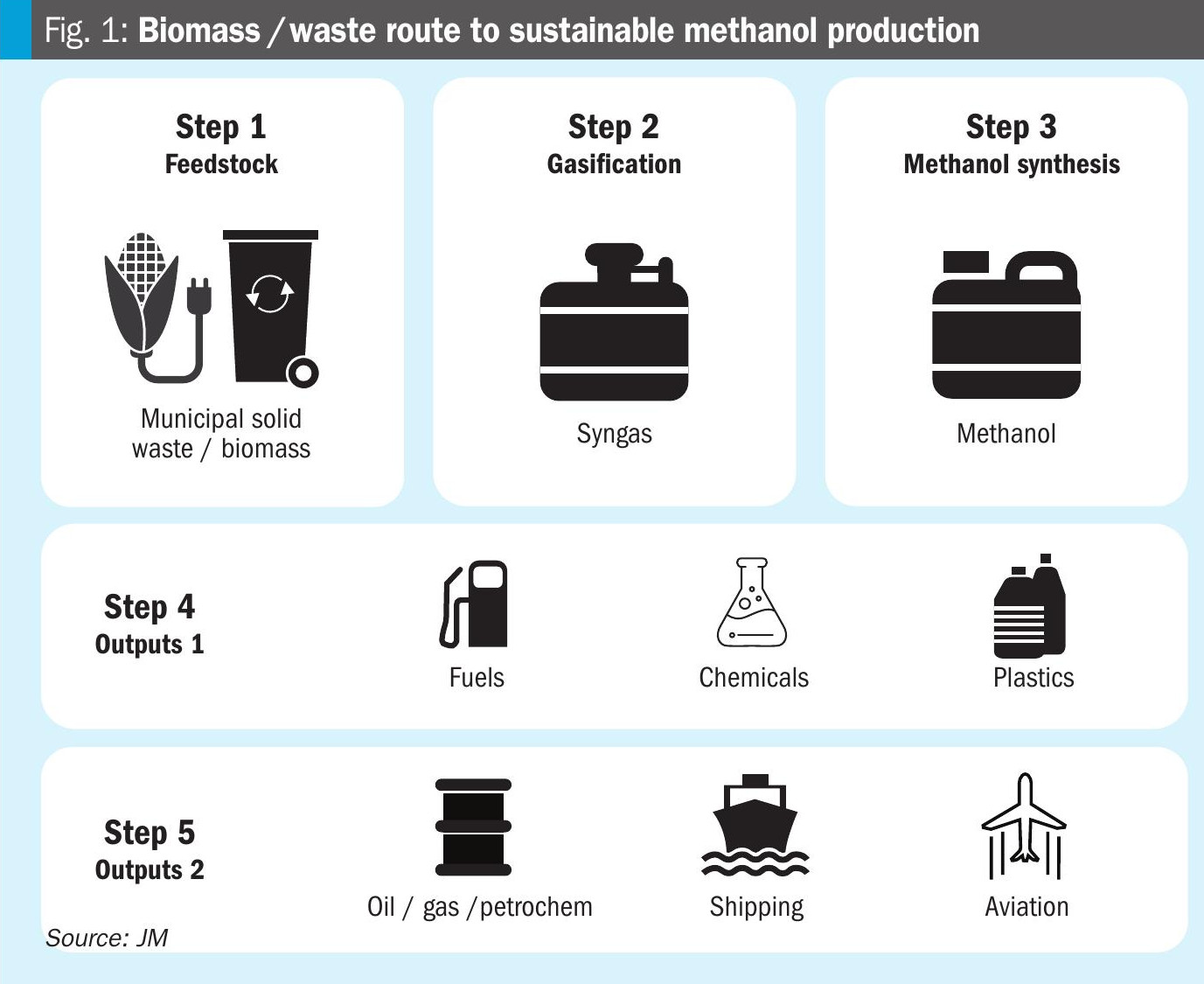

There are three primary routes to sustainable methanol production which are gaining traction today, each with its own feedstock base and process technologies (Fig. 1).

Biomass-to-methanol involves the conversion of lignocellulosic or organic residues into methanol through gasification. Feedstocks include agricultural by-products such as straw, husks and manure, forestry waste like bark and offcuts, and industrial residues such as black liquor from the pulp and paper sector. These materials absorb carbon during their growth and would otherwise decompose or be burned, releasing CO2 or methane into the atmosphere. Gasification transforms this biomass into synthesis gas, which is then catalytically converted into methanol. The process is already being commercialised in several pilot and industrial-scale facilities, particularly in regions with high biomass availability.

Waste-to-methanol makes use of the non-recyclable organic fraction of municipal solid waste, including packaging residues, textiles and contaminated materials. These wastes are typically incinerated or landfilled, both of which carry emissions and air quality consequences. Instead, they can be gasified into syngas and used as a feedstock for methanol synthesis. This approach diverts significant volumes of waste from landfill, lowers methane emissions and creates a value stream from otherwise discarded material. Waste-to-methanol technologies are now being piloted in several urban and industrial regions, where reliable waste supply chains exist and landfill diversion is a policy priority.

CO2-to-methanol, also referred to as e-methanol, involves synthesising methanol from captured carbon dioxide and green hydrogen produced via electrolysis using renewable electricity. The CO2 can come from industrial point sources such as cement or steel plants, from biogenic sources, or through direct air capture, once again using renewable feedstock sources E-methanol is particularly promising for countries with abundant renewable energy resources and strong ambitions to become hydrogen exporters or low-carbon fuel hubs.

All three routes feed into the same core methanol synthesis step, which enables technology providers and project developers to draw on decades of process engineering experience. Existing fossil methanol plants can in many cases be adapted or replicated for sustainable feedstocks, reducing time-to-market and capital investment risk.

Environmental performance and emissions impact

Methanol’s decarbonisation potential is significant, particularly when produced through sustainable pathways. According to the International Renewable Energy Agency, methanol production and usage account for approximately 0.3 gigatonnes of CO2 emissions annually, around 10% of the chemical sector’s total. Transitioning to renewable feedstocks could drastically cut this footprint.

The benefits extend beyond climate. Methanol is a clean-burning fuel that emits significantly lower levels of nitrogen oxides, sulphur oxides and particulate matter than heavy fuel oil or diesel. This makes it an attractive alternative for maritime and off-grid applications, especially in urban coastal zones with strict air quality standards.

Methanol is also biodegradable and water-soluble, making it safer to transport than many hydrocarbon fuels. Its use as a marine fuel is already in effect by a growing number of ship operators and engine manufacturers, with several commercial vessels now running on dual-fuel methanol engines.

Technology maturity and deployment outlook

The production of sustainable methanol builds on a well-established industrial process. Methanol synthesis via catalytic conversion of syngas has been deployed globally for decades. The challenge now lies in adapting this process to non-fossil feedstocks, many of which contain higher levels of impurities or present variable composition.

Technology developers with expertise in catalyst formulation and process engineering, such as Johnson Matthey, have made notable advancements in this area. Their systems are designed to process variable syngas from biomass and waste sources and deliver high-purity methanol at scale. Improvements in gas clean-up, loop efficiency and catalyst robustness are helping to close the cost gap between sustainable and conventional methanol.

In the case of e-methanol being able to accommodate hydrogen intermittency is key. Here, technology convergence is central to unlocking efficiency gains. Scalable, flexible designs that can accommodate fluctuating electricity inputs and high amounts of water in the methanol synthesis loop are being developed to ensure reliable, robust production in dynamic energy markets.

Critically, much of the infrastructure needed to transport, store and distribute methanol is already in place. Global trade routes for methanol exist, with tankers, terminals and bunkering systems adaptable for methanol produced via any route. This infrastructure readiness sets methanol apart from other alternative fuels like ammonia or hydrogen, which still face logistical hurdles.

Policy frameworks and market signals

Many jurisdictions still lack specific frameworks to differentiate between fossil-based and renewable methanol, or to reward the full lifecycle emissions savings of sustainable methanol production. Closing this policy gap will be essential for investment certainty.

However, policy support is growing, with the monumental IMO decision to enact a carbon penalty for noncompliance. However, there are several elements which will be reviewed after implementation including the cost of noncompliance, and the cost gap between eFuels and traditional marine fuels will remain in the immediate term. To enable wider adoption of sustainable fuels, industry will need clarity on the GHG default values for and a compliance framework to certify marine fuels, such as those developed by ISCC, along with clarity on the reward mechanism for using zero and near-zero (ZNZ) fuels.

Private sector demand is also rising. Several shipping companies have announced e-methanol fuel contracts for future-ready vessels. Industrial buyers are exploring methanol as a low-carbon feedstock for olefins and aromatics. In parallel, carbon offset markets and voluntary climate initiatives are beginning to factor in alternative fuels like methanol as part of broader emissions reduction strategies.

To attract investment and scale production, clearer offtake signals and stronger alignment between energy, waste and industrial policy will be required. Project bankability will hinge on stable feedstock access, long-term purchasing agreements and incentives that support infrastructure buildout.

A strategic molecule for a fragmented transition

No single fuel will solve the climate challenge. The energy transition will unfold unevenly, shaped by geography, resource access and political will. In this context, methanol’s flexibility is a major strength. It can be produced from agricultural surplus, urban waste, industrial carbon or renewable power. It can be shipped, blended, stored and used across multiple applications.

This adaptability makes methanol a strategic molecule, one that connects sectors and closes loops. It enables cross-sector synergies, such as turning pulp industry waste into marine fuel, or pairing excess renewable electricity with captured CO2 to make circular feedstocks.

Sustainable methanol will not displace every fuel, but it does not need to. Its value lies in its ability to integrate into diverse supply chains and act as a bridge between today’s infrastructure and tomorrow’s low-carbon economy.

As technology improves, policies align and costs fall, sustainable methanol is increasingly likely to become a central feature of the global energy system. It is not a concept or a pilot. It is a commercially viable, environmentally credible solution ready to be deployed, at scale, across sectors and around the world.