Nitrogen+Syngas 383 May-Jun 2023

31 May 2023

Market Outlook

Market Outlook

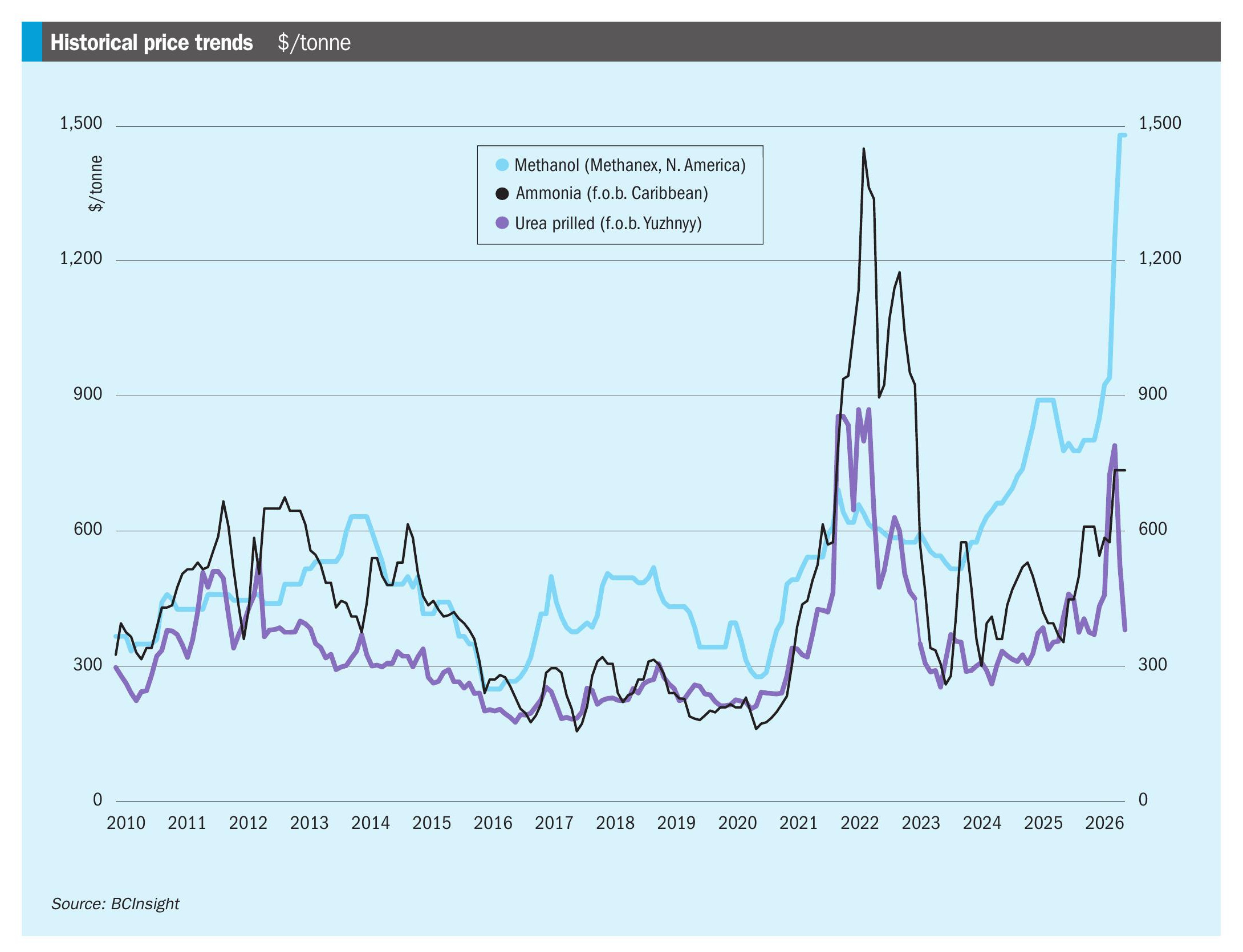

Historical price trends $/tonne

AMMONIA

- Further downward corrections are possible but the rate of demand is stabilising, suggesting the market floor is in sight, though some have suggested that May could bring another sharp reduction in the Tampa contract price towards the mid$300s c.fr. Demand remains sluggish in both eastern and western hemispheres.

- Exports from Trinidad remain lower, having fallen to around 300,000 t/month in March-April, down from 360,000 t/ month in January-February.

- Meanwhile, interest in imports in western Europe has picked up, in part due to production curtailments and increased demand from nitrate producers. TTF natural gas prices also suggest gas costs for production of $460/t in May in compared to import prices heading towards the $400/t c.fr level, likely driving increased import demand.

- Yara has idled more than half of its European ammonia capacity due to the steep drop in fertilizer prices.

UREA

- Increased supply from China and the anticipated return from turnaround of urea plants in southeast and central Asia should be exacerbated by slow import demand in the northern hemisphere.

- The US market appears relatively balanced for May-loading cargoes, even tight in some regions, but importers and traders seem reluctant to take significant long-positions and the market is nearly through the natural peak of demand for the second quarter.

- The Russian ministry of industry and trade has prepared a draft resolution to implement export quotas on certain finished fertilizers, totalling 17.94 million tonnes, applicable from 1 June to 30 November.

- Urea market focus will shift to the timing of the next Indian import tender, which does not appear likely to arrive until June. Urea prices are falling rapidly.

METHANOL

- Methanol prices have fallen due to high stocks and falling natural gas prices in both Europe and North America. Demand remains relatively limited with traded volumes thin, and there is no pickup expected in the near term.

- As a result prices have been bearish in most major markets. European spot prices fell to $485/t on local oversupply. In North America, prices fell to $550/t f.o.b. Gulf Coast.

- Chinese methanol prices also dropped sharply in March, and fell another 10% to below yuan 2,500 ($360/t) in April. Demand has been weaker than expected with MTO operating rates low, and overseas supply has been plentiful. In particular, several restarts of Iranian methanol plants have led to an increase in shipments into China of more than 200,000 tonnes in March.

- Elsewhere in Asia downstream markets have been weak and freight rates relatively high.