Price Trends

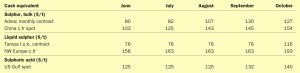

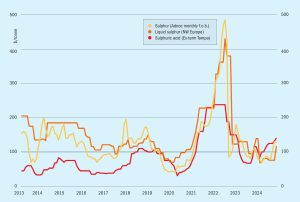

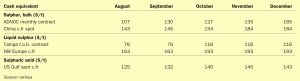

Global sulphur prices were mostly assessed flat in mid-January, with only slight changes for China, Indonesia and India, while the first quarter contracts for the Middle East, North Africa and Tampa increased from the previous quarter. Overall, the number of transactions taking place globally has declined as subdued demand has limited trading activity in most delivered markets. The current sulphur price environment has been shaped by the combination of rising Chinese demand and higher Middle East f.o.b. prices in the second half of last year. As a result, some consumer markets such as Indonesia and India have been subject to upward pressure in order to remain attractive destinations. But demand remained lacklustre across delivered markets, leaving prices relatively stable.