PuraLoop – a circular solution that delivers for crops

PuraLoop is a new fertilizer created from recycled phosphorus. ICL’s Patricia Imas and Lucas van der Saag highlight its main benefits.

PuraLoop is a new fertilizer created from recycled phosphorus. ICL’s Patricia Imas and Lucas van der Saag highlight its main benefits.

CRU’s Humphrey Knight visits EuroChem’s newly opened Serra do Salitre phosphate fertilizer complex in southern Brazil.

Paradeep Phosphates Ltd (PPL) says that it has signed a memorandum of understanding with the government of Odisha state to invest $440 million over five years to increase its phosphate fertilizer production and export capacity, including port/ jetty and infrastructure development. PPL currently has capacity to produce 400,000 t/a of urea and 2.6 million t/a of finished phosphates, via DAP and NPK plants in Paradeep, Odisha, and Zuarinagar, Goa. Details of the expansion were not announced, but the company previously said in December 2024 that it had agreed to expand phosphoric acid capacity from 500,000 t/a to 700,000 t/a to increase backwards integration of production and reduce dependence on imports.

Sulphur’s key role as a plant nutrient means that its use as a fertilizer continues to be a major area of demand.

LKAB has begun construction of its new demonstration plant for processing phosphorus and rare earth elements at Luleå. The facility is the first in a planned industrial park and, says LKAB, marks an important step in the company's ambition to diversify its business with new minerals. The supply of phosphorus for mineral fertilizers is essential for food security in Sweden and the EU, while rare earth elements are critical for the electrification and digitalisation of society, such as the production of permanent magnets for electric vehicles and wind turbines. The $75 million demonstrator plant is planned to become operational in 2026. The aim is to further develop and verify the process for utilizing material flows from iron ore production in Gällivare, where apatite concentrate is produced for further refinement and production of critical minerals in Luleå. Through a stepwise expansion, the operations can then be scaled up with additional processing facilities over time, aiming for full operation during the 2030s. Once fully operational, the industrial park’s production will be approximately seven times Sweden’s needs and 6% of the EU’s demand for phosphorus in agriculture. Currently, there is no mining of rare earth elements in Europe.

Tight supply limits availability as China maintains export restrictions.

Yara says that it plans to wind down production of phosphate fertilizers and sulphuric acid at two sites in Brazil; Cubatão and Paulínia. The sites are expected to cease production by 3Q 2025, as part of what Yara describes as a strategy to concentrate on more sustainable operations focused on its main activity: the production of nitrogen fertilizers. At Cubatão, the suspension will affect unit 3 and the phosphate plants of unit 2, while units 1 and 2, responsible for the production of nitrogen, in addition to the mixer (unit 5), will continue to operate normally. Yara reported a net loss of $290 million in 4Q 2024, down $536 million from the $246 million profit it made in 4Q 2023. Revenues are down 11% for the year, leading Yara to announce a cost reduction and investment program of $150 million, with the aim of optimising its operations and focusing on strategic areas to ensure long-term sustainability. At the same time, the company has begun renewable ammonia production at Cubatão.

CRU will convene the 2025 Phosphates+Potash Expoconference in Orlando, Florida, 31 March – 2 April.

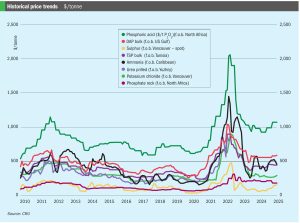

Price trends and market outlook, 20th February 2025

Fertilizer International interviews Graeme Cousland, Managing Director, and Martyn Dean, Sales Director, Begg Cousland Envirotec Limited.