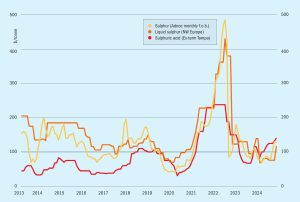

The market for ammonium sulphate

Continuing growth in Chinese ammonium sulphate production is leading to a continuing flood of exports, as greater awareness of the utility of sulphur as a fertilizer leads to increasing global demand.

Continuing growth in Chinese ammonium sulphate production is leading to a continuing flood of exports, as greater awareness of the utility of sulphur as a fertilizer leads to increasing global demand.

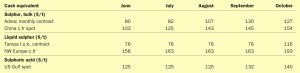

Global sulphur prices underwent increases in some key benchmark markets during October, but spot activity nevertheless remained muted, with demand subdued and availability tight. Market participants continue to closely track geopolitical developments.

While underlying supply and demand criteria continue to set floors and ceilings for nitrogen and other syngas derived products, political events as ever have the potential to derail all calculations. While much attention has focused on the US election, the escalating crisis in the Middle East continues to have the potential to threaten fertilizer trade in multiple ways. As this issue was going to press, Israel had just launched its retaliatory missile strike on Tehran, on October 26th, the latest in a series of tit for tat attacks between Israel and Iran, in particular an Iranian missile strike on Israel on October 1st. The Iranian government appeared to be downplaying the results as “limited”, but said that it considered itself “entitled and obligated to defend itself”.

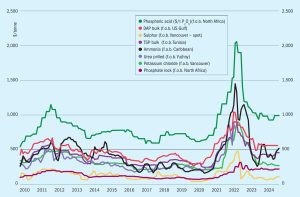

Short term supply constraints are dominating acid markets at present, but increasing smelter production across Asia may lead to oversupply in the longer term.

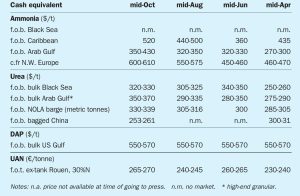

In October, ammonia benchmarks were more or less stable across the board. West of Suez, supply from Algeria was constrained by an ongoing turnaround at one of domestic player Sorfert’s production units. Still, demand from NW Europe remained quiet, although CF was set to receive a 15,000 tonne spot cargo from Hexagon some time in November, reportedly sourced somewhere in the region of $530/t f.o.b. Turkey. While regional supply appeared tight, steadily improving output from Trinidad and the US Gulf could alleviate recent pressures, with many players of the opinion that Yara and Mosaic could agree a $560/t c.fr rollover for November at Tampa as a result.

Global sulphur prices are expected to continue rising in certain regions but at a reduced rate of increase. Recent higher spot prices in the Middle East are likely to carry over to other markets. Sulphur affordability in key markets such as China remains good, reinforced by recent increases in phosphate prices.

An ammonium nitrate industry geared around producing explosives for the mining sector is now being joined by a major urea project and a number of renewables-based products for export of green ammonia.

Beyond its use in the manufacture of sulphuric acid, sulphur dioxide also has many industrial uses, especially in the food, paper, pharmaceutical and refining industries.

Ammonia prices could remain stable for the duration of October, with any further increases likely to be capped by a lack of demand. The outlook for November is more positive for buyers, with prices set to ease off once turnarounds at key export hubs are concluded.

Market snapshot, 17th October 2024 Urea : Prices firmed in a thin market in mid-October. Middle East values shot up $20/t on expectations that Indian Potash Limited (IPL) would announce another tender to secure tonnes for India in December. If correct, this will follow hot on the heels of the latest Rashtriya Chemicals and Fertilizers (RCF) purchase tender for 0.56 million tonnes of urea. Sohar International Urea & Chemical Industries (SIUCI) sold a November cargo at $390/t f.o.b. with further trader interest reported at $385/t f.o.b. This demand was probably generated by traders positioning themselves for IPL’s expected tender, given that other markets generally remained quiet.