Nitrogen+Syngas 400 Mar-Apr 2026

17 March 2026

Chemical demand for methanol

METHANOL

Chemical demand for methanol

Methanol’s phenomenal growth in the early years of the century was based on its uptake into fuel uses and its ability to bridge coal reserves with plastics production in China. However, with these sectors maturing, traditional chemical end uses are becoming the main growth sector once again.

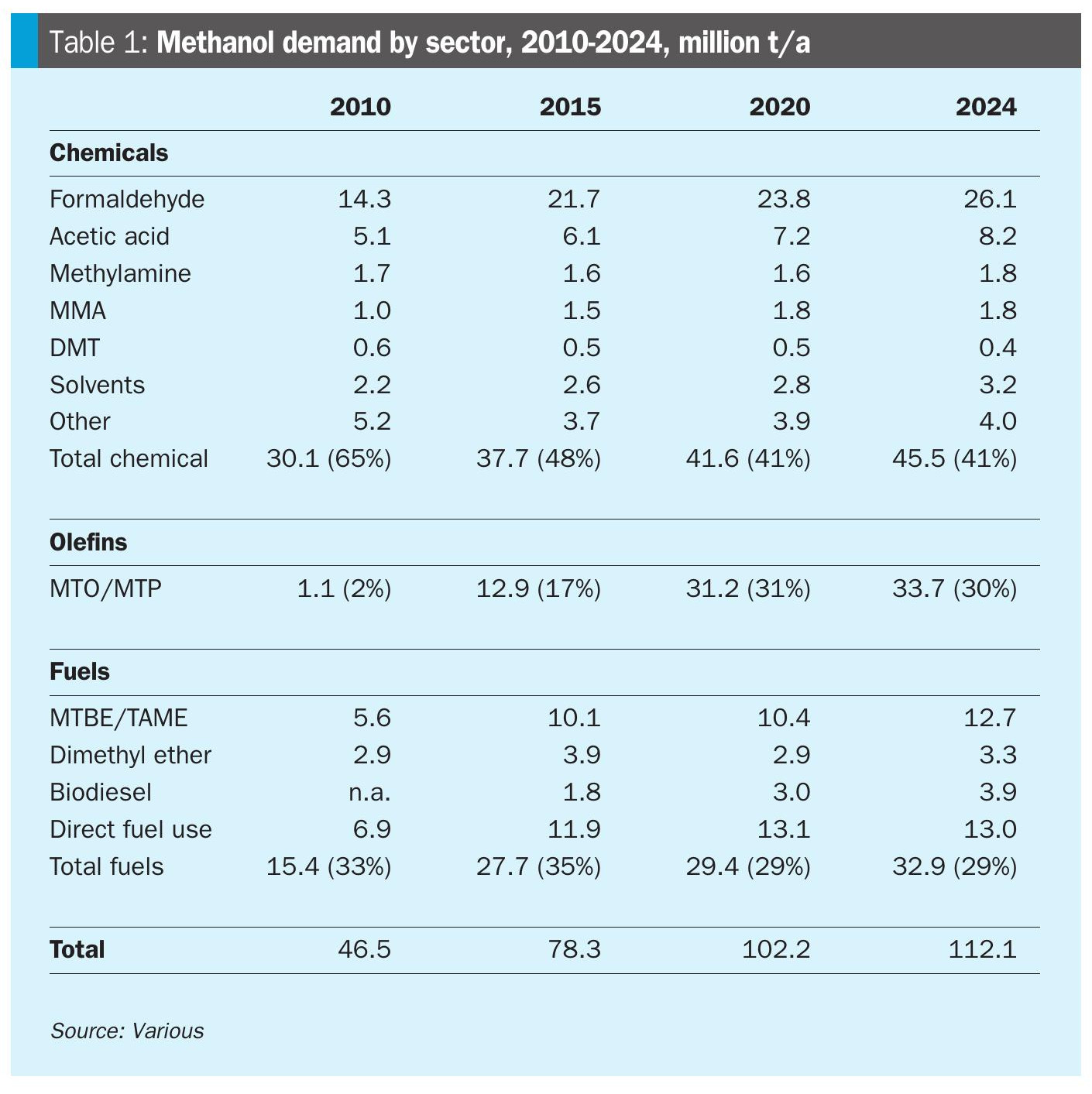

The world market for methanol was around 115 million t/a in 2025, or just over half the size of the market for ammonia, making it the second most important syngas derivative. Demand is split into three major categories. The first is traditional chemical uses, mostly formaldehyde and acetic acid, as well as methyl methacrylate (MMA), methyl chlorides and similar solvents – all told, about 40% of all methanol demand is accounted for by these uses. The second is fuel and energy uses, either as a blendstock into gasoline, as a marine fuel, or via derivatives such as methyl t-butyl ether (MTBE) or TAME as oxygenate additives into gasoline, as well as dimethyl ether for LPG blending, and methanol is also used in esterification of organic oils to form biodiesel. These collectively represent around 30% of all methanol demand. The final 30% is accounted for by conversion into olefins – propylene or ethylene, and via them into longer chain molecules as part of the plastics industry.

Since the first decade or so of the 21st century, the methanol market has effectively devolved into two separate markets; China and the rest of the world. China has been where almost all incremental demand growth has occurred, as methanol based on coal gasification provided China with a way of turning its extensive coal reserves into badly needed chemicals, fuels and plastics, reducing the need for imports from overseas. In this way, China has come to represent more than half of all methanol demand, and it accounts for all methanol to olefins (MTO) demand and most fuel use demand. China actually has about 60% of global methanol capacity, though operating rates can vary.

MTO demand

As Table 1 shows, Chinese MTO demand is around 30-33 million t/a. However, the operating rate of MTO plants is very much determined by the economics of production as compared to the rival naphtha cracking route, and this in turn depends on the relative costs of coal and crude oil. The balance between naphtha and coal-based olefins production can be a fine one. In general over the past few years, coal-based methanol costs have run slightly above naphtha route economics, but Chinse coal prices have come down from a high point around 2022-23, and while oil prices had also been sluggish due to oversupply in the global oil market, the current tensions in the Middle East have seen prices rise again to favour methanol routes to olefins. There is still new MTO plant construction in China – Guangxi Huayi Energy Chemical is building a 1 million t/a plant – but the era of very rapid production growth seen in the 2010s appears to be decisively over.

Outside of China, there has been occasional interest in MTO production, but no major projects have reached completion as yet. The most advanced is Uzbekistan’s Gas Chemical Complex, which aims to produce 1.1 million t/a of polymers. A 200,000 t/a MTO plant was also recently announced for Rotterdam by Blue Circle Olefins, though the project remains at an early stage.

Fuels demand

It is a similar story for fuel uses for methanol. China began blending methanol into gasoline in some of the major methanol producing regions in the 1990s, and also rapidly expanded DME capacity to blend into LPG. Methanol penetration of the gasoline market reached around 10%, but this is about as much as can be blended before specialised engines are required, and hence the fuel blending market has become essentially saturated and there has been no growth over the past few years. Israel and some other countries have also experimented with methanol fuel blending, but nowhere has come close to the level of demand achieved by China.

As far as energy uses by methanol derivatives go, biodiesel became popular in Europe, but EU regulations on where the organic oil was being sourced from have served to slow the development of that market, and biofuel uptake in countries such as the US and Brazil have focused on ethanol from plant sources instead. Even so, biodiesel demand is estimated to have risen from 45 billion litres in 2020 to 50 billion litres in 2025, according to the IEA. Use of esters as fuel oxygenates to burn more cleanly such as MTBE and FAME, continues to increase, particularly in China and India.

The largest potential growth area for methanol as a fuel is as an alternative to fuel oil in the marine sector. However, this is predicated on the methanol coming from low carbon sources, as discussed later.

Chemical demand

Table 1 shows that of around 10 million t/a of incremental methanol demand increase form 2020-2024, about 2.5 million t/a came from MTO, 3.5 million t/a from fuel uses, and 4 million t/a from chemicals uses, mostly formaldehyde and acetic acid. These have traditionally been the major uses for methanol, with formaldehyde going into resin production for, e.g. fibreboard manufacture, and acetic acid being used to make vinyl acetate monomer (VAM) as an intermediate for coatings, adhesives, and construction uses. Methyl methacrylate (MMA) is mainly in the construction (building panels), automotive (lightweighting), and electronics (display panels) sectors. All of these uses are thus effectively contingent on new construction, particularly of housing and vehicles, and so demand growth tends to be closely tied to GDP growth. This led to chemicals uses lagging the rapid growth in fuels and MTO use for methanol during the 2000s-2010s, but as those uses mature, so chemical demand is beginning to take the lead again.

Methanol as a bunker fuel

The IMO has set a target of the shipping sector reaching ‘net zero’ carbon emissions by 2050, and a 20-30% reduction in carbon emissions in 2030 compared to a 2008 baseline. Shipping companies have been racing to find alternatives to traditional heavy fuel oil as a marine fuel as a result. Low carbon methanol is one of the leading candidates, alongside LNG, low carbon ammonia, biodiesel, hydrogen, and electricity as power sources. LNG has been the preferred candidate in the short term, and now powers around 7% of the world’s merchant fleet. However, while considerably lower carbon than fuel oil, it is nevertheless a fossil fuel, and production of biomethane or low carbon synthetic methane tend to be smaller scale and expensive. Ammonia is developing rapidly as a proof of concept, but methanol engines for ships are already a proven technology, and the main barrier to methanol’s wider adoption as a marine fuel is production of sufficient low carbon methanol. There are 60 methanol powered (or potentially methanol powered – many are ‘dual fuel’ engined vessels) ships in service and another 300 under construction.

Blue and green methanol

Supply is the main issue now for methanol as a shipping fuel. Most methanol (ca 60%) is produced using natural gas, and around 40%, mainly in China, is based on coal as a feedstock. Low carbon methanol only represents about 1% of production at present. While there has been considerable interest in low carbon methanol production, many projects have been only at pilot scale, and final investment decisions hard to come by. In August 2024 Orsted scrapped development of its 55,000 t/a FlagshipONE green methanol project in Sweden, citing slower than expected development of the market for low carbon methanol and lack of an offtake agreement. OCI sold its blue ammonia development to Woodside and two idled biomethanol plants to Methanex.

The Methanol Institute currently calculates that there is 56 million t/a of low carbon methanol capacity under development, split between biomethanol (23 million t/a) – mostly in China and Europe – green or ‘e-methanol’ (22 million t/a), mostly in Europe, and blue methanol projects (11 million t/a), mostly in North America. Chinese biomethanol capacity seems to have the most projects actually under construction, with CIMC Green Energy Low Carbon Technology Co completing its 50,000 t/a plant at Zhanjiang in Guangdong in December 2025. Goldwind is building two 250,000 t/a plants, both using biomass gasification, like the CIMC plant. All of the low carbon methanol is being targeted at marine fuel use.

In the US, Lake Charles Methanol II, with 1.2 million t/a of capacity, is at the front end engineering design phase, while further southwest, Mexico’s Pacifico Mexinol is still on course to become the largest blue methanol plant in production, with the aim of generating 350,000 t/a of green methanol and 1.8 million t/a of blue methanol from 2028, with construction reported to be due to start in the next few months.

While some of the optimism that was attached to low carbon methanol as a bunker fuel has dissipated, it does appear that the first concrete steps are now being taken, and while chemical uses may dominate growth in the methanol market in the next couple of years, by the end of the century fuel uses may be swinging back towards prominence again.