Industrial demand for sulphur dioxide

Beyond its use in the manufacture of sulphuric acid, sulphur dioxide also has many industrial uses, especially in the food, paper, pharmaceutical and refining industries.

Beyond its use in the manufacture of sulphuric acid, sulphur dioxide also has many industrial uses, especially in the food, paper, pharmaceutical and refining industries.

A report on CRU’s annual Sulphur+Sulphuric Acid Conference, held in Barcelona, in early November.

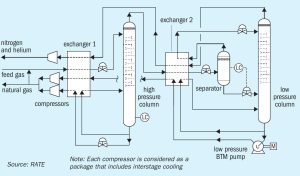

As the oil and gas industry focus on new requirements for CO2 recovery, cryogenic processes come under the spotlight. Mahin Rameshni and Stephen Santo of RATE USA discuss the importance of cryogenic processes in acid gas sweetening. Liquefied H2 S and CO2 reinjection is proposed as a cost effective alternative to large sulphur plants.

For six decades, Chemetics has been a pioneering force in the sulphuric acid design and equipment industry, consistently introducing groundbreaking technologies that have revolutionised the field by optimising the methodology in which chemicals are produced. This year, Chemetics celebrates its 60-year anniversary as one of the leading designers, direct equipment suppliers and fabricators that has modernised the sulphuric acid industry of today. This article dives into Chemetics’ rich history and key innovations that have shaped and moulded the industry.

In this revamp case study Scott Kafesjian and Quinn Kotter of Wood demonstrate how Wood sulphur technology was implemented at a 46-year old refinery SRU to improve reliability, operability and performance to meet new requirements for increased flexibility and higher availability.

OCP’s recent award of a contract to Worley Chemetics for three new greenfield sulphuric acid plants has confirmed the phosphate giant’s plans for its new Mzinda Phosphate Hub in Morocco, one of the largest investments in new phosphate capacity anywhere in the world over the next few years. It is part of a number of new investments under way in Morocco as OCP continues to expand its already considerable phosphate facilities. Three new fertilizer lines came onstream at Jorf Lasfar in 2023 and 2024, each with a capacity of 1 million t/a of diammonium phosphate (DAP). The Mzinda mega-project will add another 4 million t/a of triple superphosphate (TSP) capacity by around 2028-29, and will relieve some of the issues that OCP has in importing ammonia for DAP production, as TSP only requires phosphate rock and phosphoric acid. There is also an additional 1 million t/a of TSP capacity under construction at Jorf Lasfar, which is expected to be completed next year, and OCP also announced last year that it would build an integrated purified phosphoric acid (PPA) plant at Jorf Lasfar. The first phase of the project consists of 200,000 t/a of P2 O5 pretreated phosphoric acid capacity, 100,000 t/a (P2 O5 ) of PPA capacity, and 100,000 t/a of technical MAP (tMAP) capacity. The site will also be home to downstream production of phosphate salts and lithium iron phosphate (LFP) capacities. The initial plants will be delivered starting in mid-2026, carrying through into 2029, constructed in conjunction with JESA, a joint venture between OCP and Worley.

OCP Group has launched what it calls the Mzinda-Meskala Strategic Programme, aimed at significantly expanding fertilizer production in the country. Initially announced in December 2022, the program is set to enhance production capacity in two key regions: the Mzinda-Safi Corridor and the Meskala-Essaouira Corridor. This initiative is part of OCP’s broader strategy to meet growing global demand for fertilizers while committing to long-term sustainability goals, including achieving carbon neutrality by 2040.

This year will be the 40th Sulphur – now Sulphur + Sulphuric Acid – Conference to be held. From its beginnings in Canada to this year’s meeting at the Hyatt Regency hotel in Barcelona, much has changed, but its mission – to be an essential annual forum for the global sulphur and acid community – remains the same.

Shell Deutschland has taken a final investment decision (FID) to progress REFHYNE II, a 100 MW renewable proton-exchange membrane (PEM) hydrogen electrolyser at the Shell Energy and Chemicals Park Rheinland in Germany. Using renewable electricity, REFHYNE II is expected to produce up to 44 t/d of renewable hydrogen to partially decarbonise site operations. The electrolyser is scheduled to begin operating in 2027. Renewable hydrogen from REFHYNE II will be used at the Shell Energy and Chemicals Park to produce energy products such as transport fuels with a lower carbon intensity. Using renewable hydrogen at Shell Rheinland will help to further reduce Scope 1 and 2 emissions at the facility. In the longer term, renewable hydrogen from REFHYNE II could be directly supplied to help lower industrial emissions in the region as customer demand evolves.

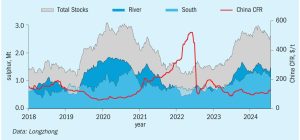

In the last two years there have been significant changes to the level and location of sulphur inventory, which has caused swings in short-term supply availability. Inventory plays a necessary role in balancing the sulphur market but exactly when, where, how, and why inventory enters the market can trigger a diverse range of price responses. In this insight article, CRU’s Peter Harrisson looks at how inventory change influences sulphur availability and pricing.